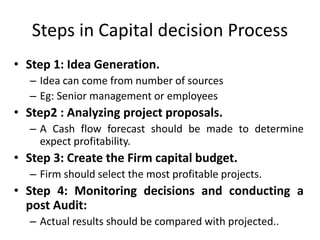

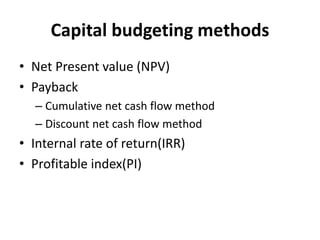

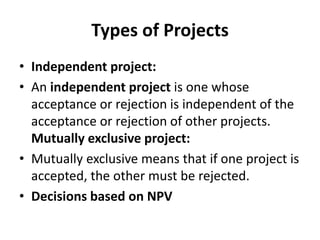

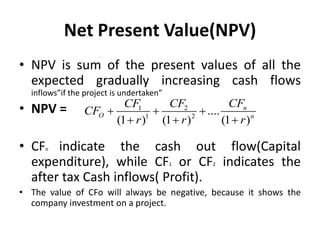

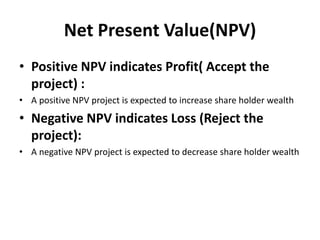

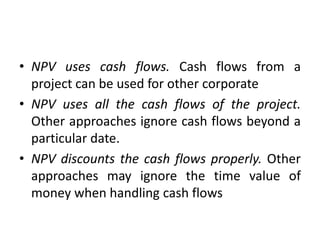

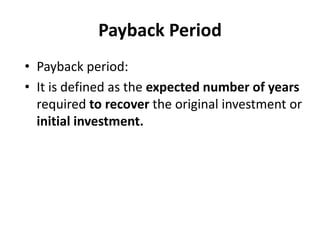

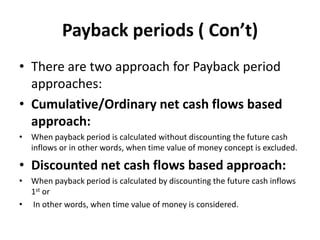

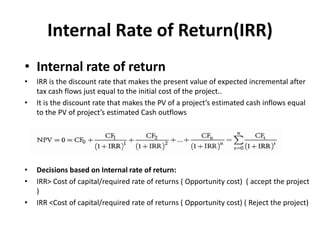

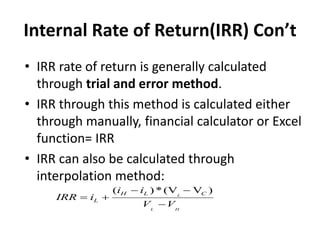

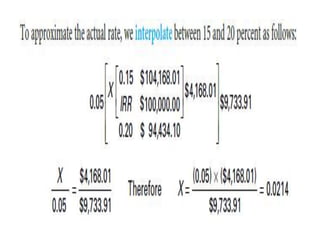

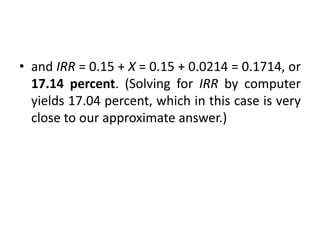

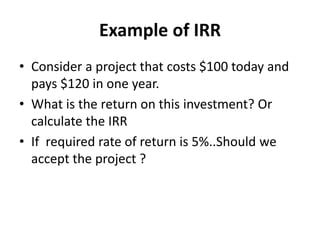

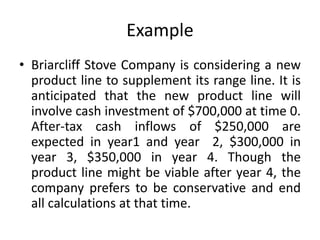

The document discusses various capital budgeting techniques used to evaluate investment projects, including net present value (NPV), payback period, internal rate of return (IRR), and profitability index (PI). It provides definitions and explanations of each method. The key steps in a typical capital budgeting process are identified as idea generation, analyzing proposals, creating a capital budget, and monitoring decisions. The importance of using good capital budgeting techniques to increase competitiveness and shareholder wealth is highlighted. Challenges with some methods and how results can differ between IRR and NPV for certain types of projects are also covered.

![5) capital_budgeting_(1)_-(2)[1].ppt.pdf](https://cdn.slidesharecdn.com/ss_thumbnails/5capitalbudgeting121-250323135834-146732f6-thumbnail.jpg?width=640&height=640&fit=bounds)