Introduction

• Financial institutionsin India are of two major kinds- banking and non-

banking

• Nonbanking financial institutions (NBFI) provide wide range of

financial services and provide enhanced equity and risk-based

products

• NBFI include non-banking financial companies (NBFC), Developmental

Financial Institutions (DFI) etc.

• NBFCs are subject less stringent regulation compared to banks and

therefore have greater flexibility in terms of lending

• NBFCs provide wide range of financial services

• NBFC vs Bank

• NBFCs cannot accept demand deposits

• NBFCs do not form part of payment and settlement systems and therefore

cannot issue and encash cheques

• NBFCs cannot issue Demand Drafts like Banks

3.

Definition of NBFC

•Section 45 I (f)- NBFC means

• (i) a financial institution which is a company;

• (ii) a non banking institution which is a company and which has as its

principal business the receiving of deposits, under any scheme or

arrangement or in any other manner, or lending in any manner;

• (iii) such other non-banking institution or class of such institutions, as the

bank may, with the previous approval of the Central Government and by

notification in the Official Gazette, specify.

• Section 45 I (c)- Financial Institution means any non-banking

institution which carries on as its business or part of its business

any of the following activities, namely :-

• the financing, whether by way of making loans or advances or otherwise, of

any activity other than its own;

• the acquisition of shares, stock, bonds, debentures or securities issued by a

government or local authority or other marketable securities of a like

nature;

4.

Definition of NBFC

•letting or delivering of any goods to a hirer under a hire-purchase agreement as

defined in clause (c) of section 2 of the Hire-Purchase Act, 1972 (26 of 1972);

• the carrying on of any class of insurance business;

• collecting, for any purpose or under any scheme or arrangement by whatever

name called monies in lump sum or otherwise, by way of subscriptions or by

sale of units, or other instruments or in any other manner and awarding prizes

or gifts, whether in cash or kind, or disbursing monies in any other way, to

persons from whom monies are collected or to any other person;

• but does not include any institution, which carries on as its principal

business-

• agricultural operations; or

• industrial activity; or;

• the purchase or sale of any goods (other than securities) or the providing of

any services; or

• the purchase, construction or sale of immovable property, so, however, that no

portion of the income of the institution is derived from the financing of

purchases, constructions or sales of immovable property by other persons;

5.

Definition of NBFC

•A Non-Banking Financial Company (NBFC) is a company registered

under the Companies Act, 1956 engaged in the business of:

• loans and advances,

• acquisition of shares/stocks/bonds/debentures/securities issued by

Government or other marketable securities of a like nature,

• leasing,

• hire-purchase,

• insurance business,

• chit fund business

• But does not include any institution whose principal business is:

• agriculture activity,

• industrial activity,

• purchase or sale of any goods (other than securities) or

• providing any services and sale/purchase/construction of immovable

property.

6.

Registration of NBFCs

•Section 45 IA of RBI Act- No NBFC can commence or carry on

business of a non-banking financial institution without obtaining a

certificate of registration from the RBI and without having a Net

Owned Funds of Rs. 2 crore - Notification No. 132/ CGM (VSNM) -99

dated April 20, 1999

• However, vide Notification No.DNBR.007/ CGM (CDS) -2015 dated

March 27, 2015 RBI stated that NBFC having a certificate of

registration from RBI and having a NOF of less that Rs. 2 crore can

continue business if they achieve Rs. 1 crore NOF by April 1, 2016 and

Rs. 2 crore NOF by April 1, 2017

• Principal business test: RBI Press release dt. April 8, 1999

• company’s financial assets constitute more than 50% of the total assets

AND

• income from financial assets constitute more than 50% of the gross

income.

7.

Registration of NBFC

•The Bank has issued notifications from time to time exempting some

entities from the requirements of Chapter III B of the RBI Act, 1934 or

part thereof.- Master Circular- Exemptions from Provisions of RBI Act,

1934

• Housing finance company under National Housing Bank Act, 1987

• Merchant Banking Company regulated by SEBI

• Micro finance company- A company registered under Sec. 25 of the

Companies Act, 1956 and engaged in micro financing activities, providing

credit not exceeding Rs. 50,000 for a business enterprise and Rs. 1,25,000 for

meeting the cost of a dwelling unit to any poor person for enabling him to

raise his level of income and standard of living

• Venture Capital Funds regulated by SEBI

• Stock Exchange/Stock Broker/Sub-Broker regulated by SEBI

• Insurance companies regulated by IRDA

• Chit fund companies regulated under Chit Funds Act, 1982

• Nidhi Company notified under Sec. 620 A of the Companies Act, 1956

• Prepaid payment instruments issued by NBFC

8.

Classification of NBFCs

•Classification of NBFCs in terms of liabilities

• Deposit Accepting – NBFCs which accepts/holds public deposits.

Definition of “public deposit” – Sec. 45 I (bb) read with Reg 2(xii)

of the MC for NBFC Acceptance of Public Deposit Directions

• Non-deposit Accepting – Non-banking financial companies which

do not accept public deposits- these are further classified in

terms of their size into Systematically Important (NBFC-NDSI) and

other non-deposit holding companies (NBFC-ND). NBFCs whose

asset size is of Rs.500 cr or more as per last audited balance sheet

are considered as systemically important NBFCs

9.

Classification of NBFCs

•Asset Finance Company (AFC)- a company whose principal business is

financing physical assets supporting productive/economic activity. E.g

automobiles, tractors, generator sets, etc. and general purpose

industrial machines. Principal business for AFC is defined as aggregate

of financing physical assets supporting economic activity and income

arising therefrom is not less than 60% of its total assets and total

income respectively.

• Investment Company (IC)- Principal business is acquisition of securities

• Loan Company (LC)- principal business is providing of finance whether

by making loans or advances or otherwise for any activity other than

its own but does not include an AFC

• Infrastructure Finance Company (IFC)- is a non-deposit taking NBFC a)

which deploys at least 75 per cent of its total assets in infrastructure

loans, b) has a minimum Net Owned Funds of Rs. 300 crore, c) has a

minimum credit rating of ‘A ‘or equivalent d) and a CRAR of 15%

10.

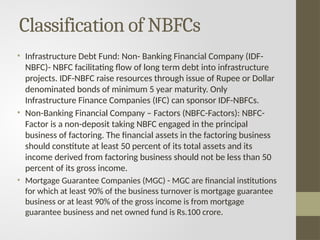

Classification of NBFCs

•Infrastructure Debt Fund: Non- Banking Financial Company (IDF-

NBFC)- NBFC facilitating flow of long term debt into infrastructure

projects. IDF-NBFC raise resources through issue of Rupee or Dollar

denominated bonds of minimum 5 year maturity. Only

Infrastructure Finance Companies (IFC) can sponsor IDF-NBFCs.

• Non-Banking Financial Company – Factors (NBFC-Factors): NBFC-

Factor is a non-deposit taking NBFC engaged in the principal

business of factoring. The financial assets in the factoring business

should constitute at least 50 percent of its total assets and its

income derived from factoring business should not be less than 50

percent of its gross income.

• Mortgage Guarantee Companies (MGC) - MGC are financial institutions

for which at least 90% of the business turnover is mortgage guarantee

business or at least 90% of the gross income is from mortgage

guarantee business and net owned fund is Rs.100 crore.

11.

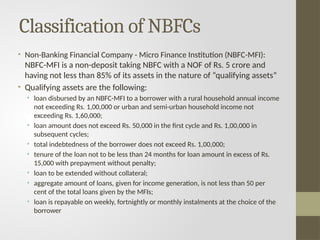

Classification of NBFCs

•Non-Banking Financial Company - Micro Finance Institution (NBFC-MFI):

NBFC-MFI is a non-deposit taking NBFC with a NOF of Rs. 5 crore and

having not less than 85% of its assets in the nature of “qualifying assets”

• Qualifying assets are the following:

• loan disbursed by an NBFC-MFI to a borrower with a rural household annual income

not exceeding Rs. 1,00,000 or urban and semi-urban household income not

exceeding Rs. 1,60,000;

• loan amount does not exceed Rs. 50,000 in the first cycle and Rs. 1,00,000 in

subsequent cycles;

• total indebtedness of the borrower does not exceed Rs. 1,00,000;

• tenure of the loan not to be less than 24 months for loan amount in excess of Rs.

15,000 with prepayment without penalty;

• loan to be extended without collateral;

• aggregate amount of loans, given for income generation, is not less than 50 per

cent of the total loans given by the MFIs;

• loan is repayable on weekly, fortnightly or monthly instalments at the choice of the

borrower

12.

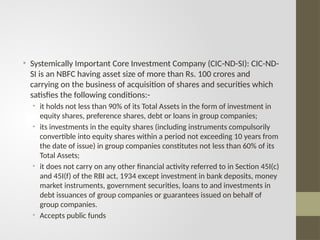

• Systemically ImportantCore Investment Company (CIC-ND-SI): CIC-ND-

SI is an NBFC having asset size of more than Rs. 100 crores and

carrying on the business of acquisition of shares and securities which

satisfies the following conditions:-

• it holds not less than 90% of its Total Assets in the form of investment in

equity shares, preference shares, debt or loans in group companies;

• its investments in the equity shares (including instruments compulsorily

convertible into equity shares within a period not exceeding 10 years from

the date of issue) in group companies constitutes not less than 60% of its

Total Assets;

• it does not carry on any other financial activity referred to in Section 45I(c)

and 45I(f) of the RBI act, 1934 except investment in bank deposits, money

market instruments, government securities, loans to and investments in

debt issuances of group companies or guarantees issued on behalf of

group companies.

• Accepts public funds

13.

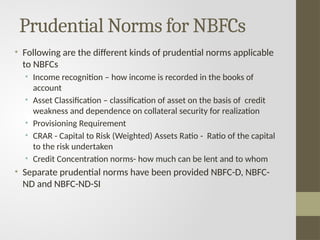

Prudential Norms forNBFCs

• Following are the different kinds of prudential norms applicable

to NBFCs

• Income recognition – how income is recorded in the books of

account

• Asset Classification – classification of asset on the basis of credit

weakness and dependence on collateral security for realization

• Provisioning Requirement

• CRAR - Capital to Risk (Weighted) Assets Ratio - Ratio of the capital

to the risk undertaken

• Credit Concentration norms- how much can be lent and to whom

• Separate prudential norms have been provided NBFC-D, NBFC-

ND and NBFC-ND-SI

14.

Corporate Governance inNBFC

• RBI issued directions for corporate governance to NBFCs

• The corporate governance norms are applicable to NBFC-ND-SI

and Deposit Taking NBFCs

• NBFCs are required to adopt the following corporate

governance norms:

• Establish a Audit Committee comprising of minimum 3 board

members. The powers and functions of Audit Committee will be

same as provided under Sec. 177 of the Companies Act, 2013

• Nomination Committee- Must ensure ‘fit and proper’ status of

proposed and existing directors

• Risk Management Committee- established to manage integrated

risk

•