Governments can influence exchange rates through direct and indirect intervention in foreign exchange markets. Direct intervention involves central banks exchanging currency reserves to influence exchange rates. Indirect intervention uses interest rates and capital controls. Exchange rate systems range from fixed rates determined by governments to freely floating rates set by markets. Governments establish currency boards and peg currencies to stabilize exchange rates. A single European currency, the euro, aims to facilitate European trade and monetary policy but also poses challenges.

Currency is any form of money in general circulation in a country. Foreign exchange is money denominated in the currency of another country or a group of countries. Simply, an exchange rate is defined as the rate at which the market converts one currency into another. Copy the link given below and paste it in new browser window to get more information on Fixed Exchange Rate:-

http://www.transtutors.com/homework-help/international-economics/economic-policy-in-open-economy/fixed-exchange-rate/

Currency is any form of money in general circulation in a country. Foreign exchange is money denominated in the currency of another country or a group of countries. Simply, an exchange rate is defined as the rate at which the market converts one currency into another. Copy the link given below and paste it in new browser window to get more information on Fixed Exchange Rate:-

http://www.transtutors.com/homework-help/international-economics/economic-policy-in-open-economy/fixed-exchange-rate/

describing the exchange rate systems, explaining how government uses direct and indirect intervention to influence exchange rates, and how government intervention in the forex markets.

The interaction between international trade.WajidMoon

International finance encompasses the study and practice of financial management in a global context, focusing on the flow of capital across borders, currency exchange rates, international investment, and international trade. Here's a concise description:

describing the exchange rate systems, explaining how government uses direct and indirect intervention to influence exchange rates, and how government intervention in the forex markets.

The interaction between international trade.WajidMoon

International finance encompasses the study and practice of financial management in a global context, focusing on the flow of capital across borders, currency exchange rates, international investment, and international trade. Here's a concise description:

[Note: This is a partial preview. To download this presentation, visit:

https://www.oeconsulting.com.sg/training-presentations]

Sustainability has become an increasingly critical topic as the world recognizes the need to protect our planet and its resources for future generations. Sustainability means meeting our current needs without compromising the ability of future generations to meet theirs. It involves long-term planning and consideration of the consequences of our actions. The goal is to create strategies that ensure the long-term viability of People, Planet, and Profit.

Leading companies such as Nike, Toyota, and Siemens are prioritizing sustainable innovation in their business models, setting an example for others to follow. In this Sustainability training presentation, you will learn key concepts, principles, and practices of sustainability applicable across industries. This training aims to create awareness and educate employees, senior executives, consultants, and other key stakeholders, including investors, policymakers, and supply chain partners, on the importance and implementation of sustainability.

LEARNING OBJECTIVES

1. Develop a comprehensive understanding of the fundamental principles and concepts that form the foundation of sustainability within corporate environments.

2. Explore the sustainability implementation model, focusing on effective measures and reporting strategies to track and communicate sustainability efforts.

3. Identify and define best practices and critical success factors essential for achieving sustainability goals within organizations.

CONTENTS

1. Introduction and Key Concepts of Sustainability

2. Principles and Practices of Sustainability

3. Measures and Reporting in Sustainability

4. Sustainability Implementation & Best Practices

To download the complete presentation, visit: https://www.oeconsulting.com.sg/training-presentations

What is the TDS Return Filing Due Date for FY 2024-25.pdfseoforlegalpillers

It is crucial for the taxpayers to understand about the TDS Return Filing Due Date, so that they can fulfill your TDS obligations efficiently. Taxpayers can avoid penalties by sticking to the deadlines and by accurate filing of TDS. Timely filing of TDS will make sure about the availability of tax credits. You can also seek the professional guidance of experts like Legal Pillers for timely filing of the TDS Return.

As a business owner in Delaware, staying on top of your tax obligations is paramount, especially with the annual deadline for Delaware Franchise Tax looming on March 1. One such obligation is the annual Delaware Franchise Tax, which serves as a crucial requirement for maintaining your company’s legal standing within the state. While the prospect of handling tax matters may seem daunting, rest assured that the process can be straightforward with the right guidance. In this comprehensive guide, we’ll walk you through the steps of filing your Delaware Franchise Tax and provide insights to help you navigate the process effectively.

Accpac to QuickBooks Conversion Navigating the Transition with Online Account...PaulBryant58

This article provides a comprehensive guide on how to

effectively manage the convert Accpac to QuickBooks , with a particular focus on utilizing online accounting services to streamline the process.

Skye Residences | Extended Stay Residences Near Toronto Airportmarketingjdass

Experience unparalleled EXTENDED STAY and comfort at Skye Residences located just minutes from Toronto Airport. Discover sophisticated accommodations tailored for discerning travelers.

Website Link :

https://skyeresidences.com/

https://skyeresidences.com/about-us/

https://skyeresidences.com/gallery/

https://skyeresidences.com/rooms/

https://skyeresidences.com/near-by-attractions/

https://skyeresidences.com/commute/

https://skyeresidences.com/contact/

https://skyeresidences.com/queen-suite-with-sofa-bed/

https://skyeresidences.com/queen-suite-with-sofa-bed-and-balcony/

https://skyeresidences.com/queen-suite-with-sofa-bed-accessible/

https://skyeresidences.com/2-bedroom-deluxe-queen-suite-with-sofa-bed/

https://skyeresidences.com/2-bedroom-deluxe-king-queen-suite-with-sofa-bed/

https://skyeresidences.com/2-bedroom-deluxe-queen-suite-with-sofa-bed-accessible/

#Skye Residences Etobicoke, #Skye Residences Near Toronto Airport, #Skye Residences Toronto, #Skye Hotel Toronto, #Skye Hotel Near Toronto Airport, #Hotel Near Toronto Airport, #Near Toronto Airport Accommodation, #Suites Near Toronto Airport, #Etobicoke Suites Near Airport, #Hotel Near Toronto Pearson International Airport, #Toronto Airport Suite Rentals, #Pearson Airport Hotel Suites

"𝑩𝑬𝑮𝑼𝑵 𝑾𝑰𝑻𝑯 𝑻𝑱 𝑰𝑺 𝑯𝑨𝑳𝑭 𝑫𝑶𝑵𝑬"

𝐓𝐉 𝐂𝐨𝐦𝐬 (𝐓𝐉 𝐂𝐨𝐦𝐦𝐮𝐧𝐢𝐜𝐚𝐭𝐢𝐨𝐧𝐬) is a professional event agency that includes experts in the event-organizing market in Vietnam, Korea, and ASEAN countries. We provide unlimited types of events from Music concerts, Fan meetings, and Culture festivals to Corporate events, Internal company events, Golf tournaments, MICE events, and Exhibitions.

𝐓𝐉 𝐂𝐨𝐦𝐬 provides unlimited package services including such as Event organizing, Event planning, Event production, Manpower, PR marketing, Design 2D/3D, VIP protocols, Interpreter agency, etc.

Sports events - Golf competitions/billiards competitions/company sports events: dynamic and challenging

⭐ 𝐅𝐞𝐚𝐭𝐮𝐫𝐞𝐝 𝐩𝐫𝐨𝐣𝐞𝐜𝐭𝐬:

➢ 2024 BAEKHYUN [Lonsdaleite] IN HO CHI MINH

➢ SUPER JUNIOR-L.S.S. THE SHOW : Th3ee Guys in HO CHI MINH

➢FreenBecky 1st Fan Meeting in Vietnam

➢CHILDREN ART EXHIBITION 2024: BEYOND BARRIERS

➢ WOW K-Music Festival 2023

➢ Winner [CROSS] Tour in HCM

➢ Super Show 9 in HCM with Super Junior

➢ HCMC - Gyeongsangbuk-do Culture and Tourism Festival

➢ Korean Vietnam Partnership - Fair with LG

➢ Korean President visits Samsung Electronics R&D Center

➢ Vietnam Food Expo with Lotte Wellfood

"𝐄𝐯𝐞𝐫𝐲 𝐞𝐯𝐞𝐧𝐭 𝐢𝐬 𝐚 𝐬𝐭𝐨𝐫𝐲, 𝐚 𝐬𝐩𝐞𝐜𝐢𝐚𝐥 𝐣𝐨𝐮𝐫𝐧𝐞𝐲. 𝐖𝐞 𝐚𝐥𝐰𝐚𝐲𝐬 𝐛𝐞𝐥𝐢𝐞𝐯𝐞 𝐭𝐡𝐚𝐭 𝐬𝐡𝐨𝐫𝐭𝐥𝐲 𝐲𝐨𝐮 𝐰𝐢𝐥𝐥 𝐛𝐞 𝐚 𝐩𝐚𝐫𝐭 𝐨𝐟 𝐨𝐮𝐫 𝐬𝐭𝐨𝐫𝐢𝐞𝐬."

RMD24 | Debunking the non-endemic revenue myth Marvin Vacquier Droop | First ...BBPMedia1

Marvin neemt je in deze presentatie mee in de voordelen van non-endemic advertising op retail media netwerken. Hij brengt ook de uitdagingen in beeld die de markt op dit moment heeft op het gebied van retail media voor niet-leveranciers.

Retail media wordt gezien als het nieuwe advertising-medium en ook mediabureaus richten massaal retail media-afdelingen op. Merken die niet in de betreffende winkel liggen staan ook nog niet in de rij om op de retail media netwerken te adverteren. Marvin belicht de uitdagingen die er zijn om echt aansluiting te vinden op die markt van non-endemic advertising.

India Orthopedic Devices Market: Unlocking Growth Secrets, Trends and Develop...Kumar Satyam

According to TechSci Research report, “India Orthopedic Devices Market -Industry Size, Share, Trends, Competition Forecast & Opportunities, 2030”, the India Orthopedic Devices Market stood at USD 1,280.54 Million in 2024 and is anticipated to grow with a CAGR of 7.84% in the forecast period, 2026-2030F. The India Orthopedic Devices Market is being driven by several factors. The most prominent ones include an increase in the elderly population, who are more prone to orthopedic conditions such as osteoporosis and arthritis. Moreover, the rise in sports injuries and road accidents are also contributing to the demand for orthopedic devices. Advances in technology and the introduction of innovative implants and prosthetics have further propelled the market growth. Additionally, government initiatives aimed at improving healthcare infrastructure and the increasing prevalence of lifestyle diseases have led to an upward trend in orthopedic surgeries, thereby fueling the market demand for these devices.

Memorandum Of Association Constitution of Company.pptseri bangash

www.seribangash.com

A Memorandum of Association (MOA) is a legal document that outlines the fundamental principles and objectives upon which a company operates. It serves as the company's charter or constitution and defines the scope of its activities. Here's a detailed note on the MOA:

Contents of Memorandum of Association:

Name Clause: This clause states the name of the company, which should end with words like "Limited" or "Ltd." for a public limited company and "Private Limited" or "Pvt. Ltd." for a private limited company.

https://seribangash.com/article-of-association-is-legal-doc-of-company/

Registered Office Clause: It specifies the location where the company's registered office is situated. This office is where all official communications and notices are sent.

Objective Clause: This clause delineates the main objectives for which the company is formed. It's important to define these objectives clearly, as the company cannot undertake activities beyond those mentioned in this clause.

www.seribangash.com

Liability Clause: It outlines the extent of liability of the company's members. In the case of companies limited by shares, the liability of members is limited to the amount unpaid on their shares. For companies limited by guarantee, members' liability is limited to the amount they undertake to contribute if the company is wound up.

https://seribangash.com/promotors-is-person-conceived-formation-company/

Capital Clause: This clause specifies the authorized capital of the company, i.e., the maximum amount of share capital the company is authorized to issue. It also mentions the division of this capital into shares and their respective nominal value.

Association Clause: It simply states that the subscribers wish to form a company and agree to become members of it, in accordance with the terms of the MOA.

Importance of Memorandum of Association:

Legal Requirement: The MOA is a legal requirement for the formation of a company. It must be filed with the Registrar of Companies during the incorporation process.

Constitutional Document: It serves as the company's constitutional document, defining its scope, powers, and limitations.

Protection of Members: It protects the interests of the company's members by clearly defining the objectives and limiting their liability.

External Communication: It provides clarity to external parties, such as investors, creditors, and regulatory authorities, regarding the company's objectives and powers.

https://seribangash.com/difference-public-and-private-company-law/

Binding Authority: The company and its members are bound by the provisions of the MOA. Any action taken beyond its scope may be considered ultra vires (beyond the powers) of the company and therefore void.

Amendment of MOA:

While the MOA lays down the company's fundamental principles, it is not entirely immutable. It can be amended, but only under specific circumstances and in compliance with legal procedures. Amendments typically require shareholder

Business Valuation Principles for EntrepreneursBen Wann

This insightful presentation is designed to equip entrepreneurs with the essential knowledge and tools needed to accurately value their businesses. Understanding business valuation is crucial for making informed decisions, whether you're seeking investment, planning to sell, or simply want to gauge your company's worth.

Unveiling the Secrets How Does Generative AI Work.pdfSam H

At its core, generative artificial intelligence relies on the concept of generative models, which serve as engines that churn out entirely new data resembling their training data. It is like a sculptor who has studied so many forms found in nature and then uses this knowledge to create sculptures from his imagination that have never been seen before anywhere else. If taken to cyberspace, gans work almost the same way.

Enterprise Excellence is Inclusive Excellence.pdfKaiNexus

Enterprise excellence and inclusive excellence are closely linked, and real-world challenges have shown that both are essential to the success of any organization. To achieve enterprise excellence, organizations must focus on improving their operations and processes while creating an inclusive environment that engages everyone. In this interactive session, the facilitator will highlight commonly established business practices and how they limit our ability to engage everyone every day. More importantly, though, participants will likely gain increased awareness of what we can do differently to maximize enterprise excellence through deliberate inclusion.

What is Enterprise Excellence?

Enterprise Excellence is a holistic approach that's aimed at achieving world-class performance across all aspects of the organization.

What might I learn?

A way to engage all in creating Inclusive Excellence. Lessons from the US military and their parallels to the story of Harry Potter. How belt systems and CI teams can destroy inclusive practices. How leadership language invites people to the party. There are three things leaders can do to engage everyone every day: maximizing psychological safety to create environments where folks learn, contribute, and challenge the status quo.

Who might benefit? Anyone and everyone leading folks from the shop floor to top floor.

Dr. William Harvey is a seasoned Operations Leader with extensive experience in chemical processing, manufacturing, and operations management. At Michelman, he currently oversees multiple sites, leading teams in strategic planning and coaching/practicing continuous improvement. William is set to start his eighth year of teaching at the University of Cincinnati where he teaches marketing, finance, and management. William holds various certifications in change management, quality, leadership, operational excellence, team building, and DiSC, among others.

Cracking the Workplace Discipline Code Main.pptxWorkforce Group

Cultivating and maintaining discipline within teams is a critical differentiator for successful organisations.

Forward-thinking leaders and business managers understand the impact that discipline has on organisational success. A disciplined workforce operates with clarity, focus, and a shared understanding of expectations, ultimately driving better results, optimising productivity, and facilitating seamless collaboration.

Although discipline is not a one-size-fits-all approach, it can help create a work environment that encourages personal growth and accountability rather than solely relying on punitive measures.

In this deck, you will learn the significance of workplace discipline for organisational success. You’ll also learn

• Four (4) workplace discipline methods you should consider

• The best and most practical approach to implementing workplace discipline.

• Three (3) key tips to maintain a disciplined workplace.

3. A6 - 3

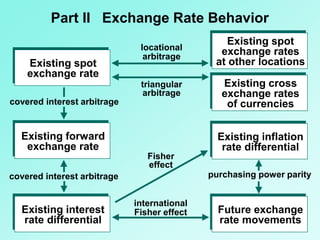

Chapter Objectives

• To describe the exchange rate

systems used by various

governments;

• To explain how governments can use

direct and indirect intervention to

influence exchange rates; and

• To explain how government intervention in

the foreign exchange market can affect

economic conditions.

4. A6 - 4

Exchange Rate Systems

• Exchange rate systems can be classified

according to the degree to which the rates

are controlled by the government.

• Exchange rate systems normally fall into

one of the following categories:

¤ fixed

¤ freely floating

¤ managed float

¤ pegged

5. A6 - 5

• In a fixed exchange rate system, exchange

rates are either held constant or allowed

to fluctuate only within very narrow bands.

• The Bretton Woods era (1944-1971) fixed

each currency’s value in terms of gold.

• The 1971 Smithsonian Agreement which

followed merely adjusted the exchange

rates and expanded the fluctuation

boundaries. The system was still fixed.

Fixed

Exchange Rate System

6. A6 - 6

• Pros: Work becomes easier for the MNCs.

• Cons: Governments may revalue their

currencies. In fact, the dollar was

devalued more than once after the U.S.

experienced balance of trade deficits.

• Cons: Each country may become more

vulnerable to the economic conditions in

other countries.

Fixed

Exchange Rate System

7. A6 - 7

• In a freely floating exchange rate system,

exchange rates are determined solely by

market forces.

• Pros: Each country may become more

insulated against the economic problems

in other countries.

• Pros: Central bank interventions that may

affect the economy unfavorably are no

longer needed.

Freely Floating

Exchange Rate System

8. A6 - 8

• Pros: Governments are not restricted by

exchange rate boundaries when setting

new policies.

• Pros: Less capital flow restrictions are

needed, thus enhancing the efficiency of

the financial market.

Freely Floating

Exchange Rate System

9. A6 - 9

• Cons: MNCs may need to devote

substantial resources to managing their

exposure to exchange rate fluctuations.

• Cons: The country that initially

experienced economic problems (such as

high inflation, increasing unemployment

rate) may have its problems compounded.

Freely Floating

Exchange Rate System

10. A6 - 10

• In a managed (or “dirty”) float exchange

rate system, exchange rates are allowed to

move freely on a daily basis and no official

boundaries exist. However, governments

may intervene to prevent the rates from

moving too much in a certain direction.

• Cons: A government may manipulate its

exchange rates such that its own country

benefits at the expense of others.

Managed Float

Exchange Rate System

11. A6 - 11

• In a pegged exchange rate system, the

home currency’s value is pegged to a

foreign currency or to some unit of

account, and moves in line with that

currency or unit against other currencies.

• The European Economic Community’s

snake arrangement (1972-1979) pegged

the currencies of member countries within

established limits of each other.

Pegged

Exchange Rate System

12. A6 - 12

• The European Monetary System which

followed in 1979 held the exchange rates

of member countries together within

specified limits and also pegged them to a

European Currency Unit (ECU) through

the exchange rate mechanism (ERM).

¤ The ERM experienced severe problems in

1992, as economic conditions and goals

varied among member countries.

Pegged

Exchange Rate System

13. A6 - 13

• In 1994, Mexico’s central bank pegged the

peso to the U.S. dollar, but allowed a band

within which the peso’s value could

fluctuate against the dollar.

¤ By the end of the year, there was

substantial downward pressure on the

peso, and the central bank allowed the

peso to float freely. The Mexican peso

crisis had just began ...

Pegged

Exchange Rate System

14. A6 - 14

Currency Boards

• A currency board is a system for

maintaining the value of the local currency

with respect to some other specified

currency.

• For example, Hong Kong has tied the

value of the Hong Kong dollar to the U.S.

dollar (HK$7.8 = $1) since 1983, while

Argentina has tied the value of its peso to

the U.S. dollar (1 peso = $1) since 1991.

15. A6 - 15

Currency Boards

• For a currency board to be successful, it

must have credibility in its promise to

maintain the exchange rate.

• It has to intervene to defend its position

against the pressures exerted by

economic conditions, as well as by

speculators who are betting that the board

will not be able to support the specified

exchange rate.

16. A6 - 16

Exposure of a Pegged Currency to

Interest Rate Movements

• A country that uses a currency board does

not have complete control over its local

interest rates, as the rates must be aligned

with the interest rates of the currency to

which the local currency is tied.

• Note that the two interest rates may not be

exactly the same because of different

risks.

17. A6 - 17

• A currency that is pegged to another

currency will have to move in tandem with

that currency against all other currencies.

• So, the value of a pegged currency does

not necessarily reflect the demand and

supply conditions in the foreign exchange

market, and may result in uneven trade or

capital flows.

Exposure of a Pegged Currency to

Exchange Rate Movements

18. A6 - 18

Dollarization

• Dollarization refers to the replacement of a

local currency with U.S. dollars.

• Dollarization goes beyond a currency

board, as the country no longer has a

local currency.

• For example, Ecuador implemented

dollarization in 2000.

19. A6 - 19

€A Single European Currency

• In 1991, the Maastricht treaty called for a

single European currency. On Jan 1, 1999,

the euro was adopted by Austria, Belgium,

Finland, France, Germany, Ireland, Italy,

Luxembourg, Netherlands, Portugal, and

Spain. Greece joined the system in 2001.

• By 2002, the national currencies of the 12

participating countries will be withdrawn

and completely replaced with the euro.

20. A6 - 20

• Within the euro-zone, cross-border trade

and capital flows will occur without the

need to convert to another currency.

• European monetary policy is also

consolidated because of the single money

supply. The Frankfurt-based European

Central Bank (ECB) is responsible for

setting the common monetary policy.

€A Single European Currency

21. A6 - 21

• The ECB aims to control inflation in the

participating countries and to stabilize the

euro within reasonable boundaries.

• The common monetary policy may

eventually lead to more political harmony.

• Note that each participating country may

have to rely on its own fiscal policy (tax

and government expenditure decisions) to

help solve local economic problems.

€A Single European Currency

22. A6 - 22

• As currency movements among the

European countries will be eliminated,

there should be an increase in all types of

business arrangements, more comparable

product pricing, and more trade flows.

• It will also be easier to compare and

conduct valuations of firms across the

participating European countries.

€A Single European Currency

23. A6 - 23

• Stock and bond prices will also be more

comparable and there should be more

cross-border investing. However, non-

European investors may not achieve as

much diversification as in the past.

• Exchange rate risk and foreign exchange

transaction costs within the euro-zone will

be eliminated, while interest rates will

have to be similar.

€A Single European Currency

24. A6 - 24

• Since its introduction in 1999, the euro

has declined against many currencies.

• This weakness was partially attributed to

capital outflows from Europe, which was

in turn partially attributed to a lack of

confidence in the euro.

• Some countries had ignored restraint in

favor of resolving domestic problems,

resulting in a lack of solidarity.

€A Single European Currency

25. A6 - 25

Government Intervention

• Each country has a government agency

(called the central bank) that may

intervene in the foreign exchange market

to control the value of the country’s

currency.

• In the United States, the Federal Reserve

System (Fed) is the central bank.

26. A6 - 26

Government Intervention

• Central banks manage exchange rates

¤ to smooth exchange rate movements,

¤ to establish implicit exchange rate

boundaries, and/or

¤ to respond to temporary disturbances.

• Often, intervention is overwhelmed by

market forces. However, currency

movements may be even more volatile in

the absence of intervention.

27. A6 - 27

• Direct intervention refers to the exchange

of currencies that the central bank holds

as reserves for other currencies in the

foreign exchange market.

• Direct intervention is usually most

effective when there is a coordinated

effort among central banks.

Government Intervention

28. A6 - 28

• When a central bank intervenes in the

foreign exchange market without

adjusting for the change in money supply,

it is said to engaged in nonsterilized

intervention.

• In a sterilized intervention, Treasury

securities are purchased or sold at the

same time to maintain the money supply.

Government Intervention

29. A6 - 29

• Some speculators attempt to determine

when the central bank is intervening, and

the extent of the intervention, in order to

capitalize on the anticipated results of the

intervention effort.

Government Intervention

30. A6 - 30

• Central banks can also engage in indirect

intervention by influencing the factors that

determine the value of a currency.

• For example, the Fed may attempt to

increase interest rates (and hence boost

the dollar’s value) by reducing the U.S.

money supply.

¤ Note that high interest rates adversely

affects local borrowers.

Government Intervention

31. A6 - 31

• Governments may also use foreign

exchange controls (such as restrictions

on currency exchange) as a form of

indirect intervention.

Government Intervention

32. A6 - 32

Exchange Rate Target Zones

• Many economists have criticized the

present exchange rate system because of

the wide swings in the exchange rates of

major currencies.

• Some have suggested that target zones be

used, whereby an initial exchange rate will

be established with specific boundaries

(that are wider than the bands used in

fixed exchange rate systems).

33. A6 - 33

Exchange Rate Target Zones

• The ideal target zone should allow rates to

adjust to economic factors without

causing wide swings in international trade

and fear in the financial markets.

• However, the actual result may be a

system no different from what exists

today.

34. A6 - 34

Intervention as a Policy Tool

• Like tax laws and money supply, the

exchange rate is a tool which a

government can use to achieve its desired

economic objectives.

• A weak home currency can stimulate

foreign demand for products, and hence

local jobs. However, it may also lead to

higher inflation.

35. A6 - 35

Intervention as a Policy Tool

• A strong currency may cure high inflation,

since the intensified foreign competition

should cause domestic producers to

refrain from increasing prices. However, it

may also lead to higher unemployment.

36. A6 - 36

Impact of Central Bank Intervention

on an MNC’s Value

n

t

t

m

j

tjtj

k1=

1

,,

1

ERECFE

=Value

E (CFj,t ) = expected cash flows in currency j to be received

by the U.S. parent at the end of period t

E (ERj,t ) = expected exchange rate at which currency j can

be converted to dollars at the end of period t

k = weighted average cost of capital of the parent

Direct Intervention

Indirect Intervention

37. A6 - 37

• Exchange Rate Systems

¤ Fixed Exchange Rate System

¤ Freely Floating Exchange Rate System

¤ Managed Float Exchange Rate System

¤ Pegged Exchange Rate System

¤ Currency Boards

¤ Exposure of a Pegged Currency to Interest

Rate and Exchange Rate Movements

¤ Dollarization

Chapter Review

38. A6 - 38

Chapter Review

• A Single European Currency

¤ Membership

¤ Euro Transactions

¤ Impact on European Monetary Policy

¤ Impact on Business Within Europe

¤ Impact on the Valuation of Businesses in

Europe

¤ Impact on Financial Flows

¤ Impact on Exchange Rate Risk

¤ Status Report on the Euro

39. A6 - 39

Chapter Review

• Government Intervention

¤ Reasons for Government Intervention

¤ Direct Intervention

¤ Indirect Intervention

• Exchange Rate Target Zones

40. A6 - 40

Chapter Review

• Intervention as a Policy Tool

¤ Influence of a Weak Home Currency on the

Economy

¤ Influence of a Strong Home Currency on

the Economy

• How Central Bank Intervention Can Affect

an MNC’s Value