Download to read offline

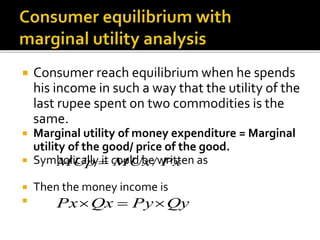

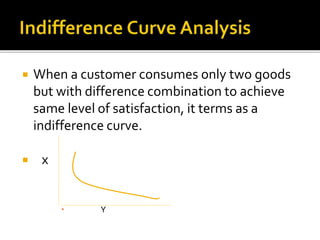

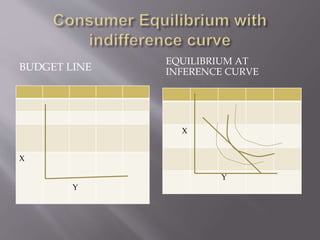

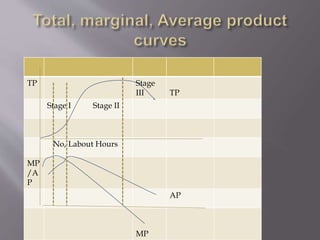

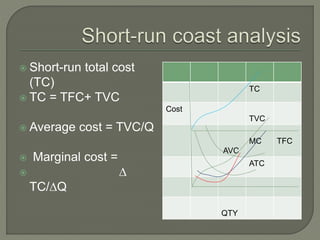

This document provides an overview of concepts related to consumer behavior and production including: - Marginal utility analysis, consumer equilibrium, and indifference curve analysis which are used to understand how consumers maximize utility given budget constraints. - Assumptions of utility analysis including that consumers attempt to maximize well-being, income constraints consumption, and marginal utility diminishes with increasing consumption. - The law of diminishing marginal utility which states that as consumption increases, marginal utility declines. - Consumer equilibrium is reached when marginal utility per rupee is equal across goods. - Indifference curves, their properties including being negatively sloped and convex, and their use in analyzing consumer choice. - Short-run production