Downloaded 12 times

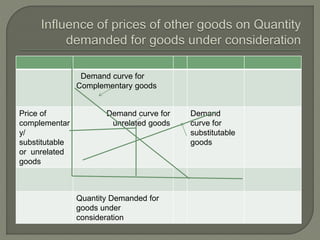

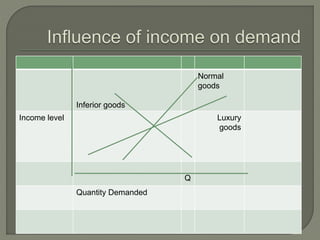

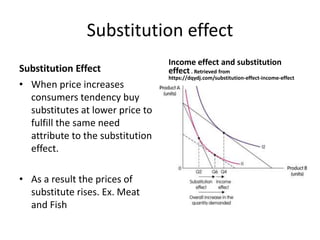

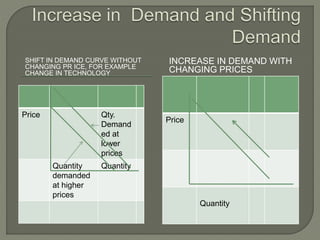

This document provides an overview of key economic concepts covered in introductory economics including: - Definitions of economic and non-economic goods and the production process. The four factors of production: land, labor, capital, and entrepreneurship. - The concept of scarcity and how it leads to trade-offs requiring rational choice between alternative uses of limited resources. Opportunity cost is explored through examples. - Demand analysis including the difference between demand and effective demand. The law of demand and factors that influence demand like price, income, tastes. - Supply analysis including the law of supply and factors that influence supply like price, costs of production, and technology. - Equilibrium concepts where

![Microeconomic_Basic_Concepts_&_Principals[1] - Read-Only](https://cdn.slidesharecdn.com/ss_thumbnails/microeconomicbasicconceptsprincipals1-read-only-240514160329-bf7b4dd3-thumbnail.jpg?width=640&height=640&fit=bounds)

![Awareness of digital currency[1] (1).pptx](https://cdn.slidesharecdn.com/ss_thumbnails/awarenessofdigitalcurrency11-260125155504-b1badee4-thumbnail.jpg?width=640&height=640&fit=bounds)