Download to read offline

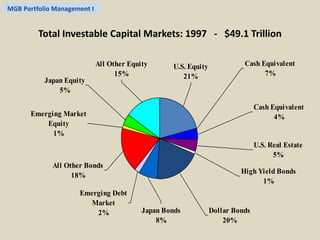

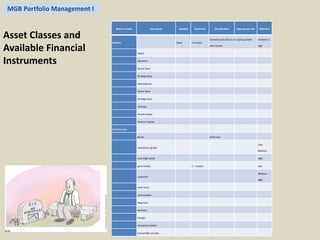

- The document discusses the case for global investing and diversifying investment portfolios internationally. It notes the growth of markets outside the US and developed world as reasons for global investing. - It also discusses some of the challenges of international investing like currency risk and political uncertainty. However, fund managers still see benefits from diversifying beyond domestic markets given global economic trends. - The document provides examples of asset classes and financial instruments available for global investing including stocks, bonds, investment companies and real estate investment trusts.

![[EN] Strategy Brief / Global Convertible Opportunities / December 2015](https://cdn.slidesharecdn.com/ss_thumbnails/strategybriefglobalconvertibleopportunitiesv9-151224093002-thumbnail.jpg?width=640&height=640&fit=bounds)