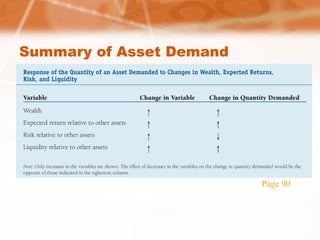

This document provides an overview of demand for financial assets. It discusses key concepts such as:

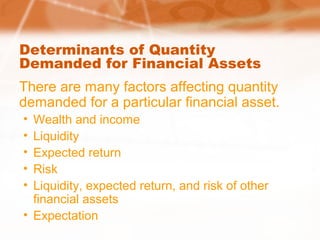

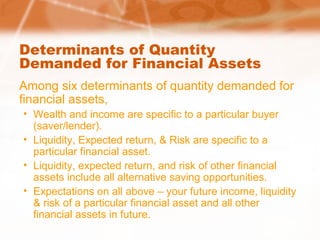

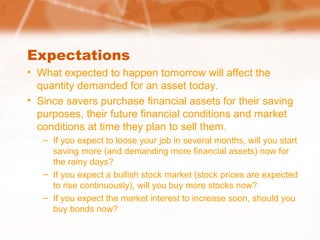

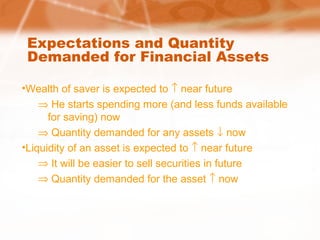

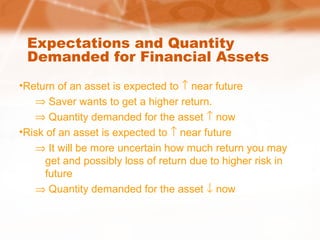

- The determinants of demand for financial assets, including wealth, income, liquidity, expected return, risk, and expectations.

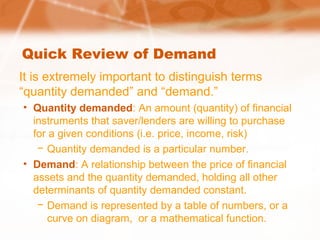

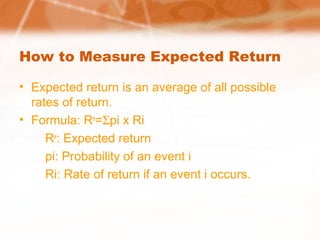

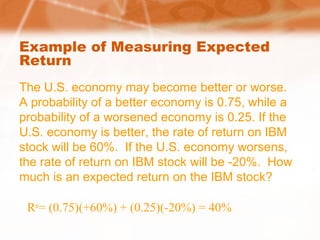

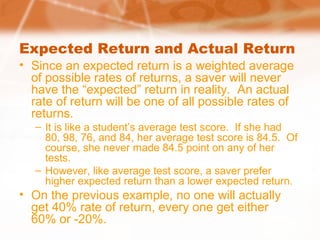

- How expected return is calculated using probabilities of different possible returns.

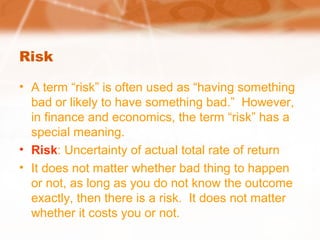

- The different types of risk associated with financial assets like default risk, purchasing power risk, and interest rate risk.

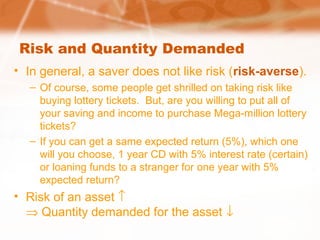

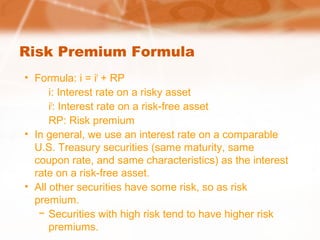

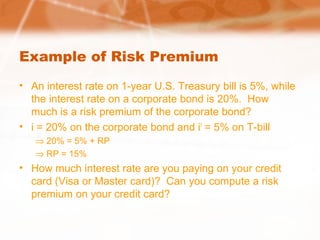

- The relationship between risk and return, known as the risk-return tradeoff, and how risk premium compensates for higher risk.

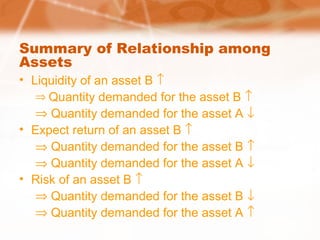

- How demanders evaluate and compare characteristics of different assets to determine which ones they demand more of.