Maksym Vyshnivetskyi: Управління вартістю (Cost) (UA)

2.

Favorite pet

Ozzy Osbourne.Not that one, but this one

with big ears

The quote I like

«A journey of a thousand miles begins with a single step»

Master degree in economical geography

• Delivery Quality Monitoring and Support

dept. (it’s not about testing ), Director

• PM Chapter co-lead

Endless talks about

• Why Agile will not help us to survive

• And a bit about project

management, quality assurance and

Kanban Method

Experience

• 10 year of project management in public sector

and outsourcing

• 10 year in process management and quality

assurance

Hello, world ☺

3.

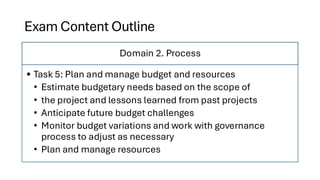

Exam Content Outline

Domain2. Process

• Task 5: Plan and manage budget and resources

• Estimate budgetary needs based on the scope of

• the project and lessons learned from past projects

• Anticipate future budget challenges

• Monitor budget variations and work with governance

process to adjust as necessary

• Plan and manage resources

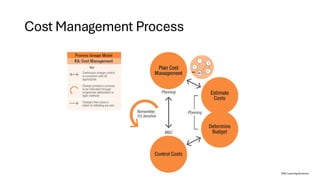

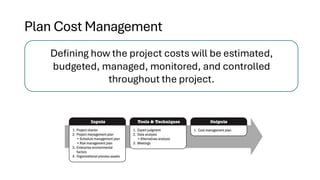

Plan Cost Management

Defininghow the project costs will be estimated,

budgeted, managed, monitored, and controlled

throughout the project.

6.

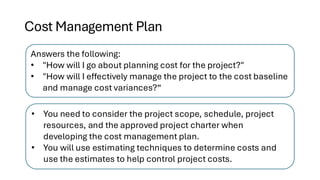

Cost Management Plan

Answersthe following:

• "How will I go about planning cost for the project?"

• "How will I effectively manage the project to the cost baseline

and manage cost variances?“

• You need to consider the project scope, schedule, project

resources, and the approved project charter when

developing the cost management plan.

• You will use estimating techniques to determine costs and

use the estimates to help control project costs.

7.

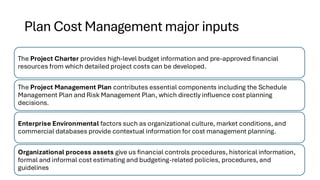

Plan Cost Managementmajor inputs

The Project Charter provides high-level budget information and pre-approved financial

resources from which detailed project costs can be developed.

The Project Management Plan contributes essential components including the Schedule

Management Plan and Risk Management Plan, which directly influence cost planning

decisions.

Enterprise Environmental factors such as organizational culture, market conditions, and

commercial databases provide contextual information for cost management planning.

Organizational process assets give us financial controls procedures, historical information,

formal and informal cost estimating and budgeting-related policies, procedures, and

guidelines

8.

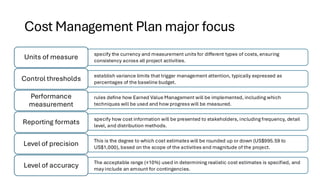

Cost Management Planmajor focus

specify the currency and measurement units for different types of costs, ensuring

consistency across all project activities.

Units of measure

establish variance limits that trigger management attention, typically expressed as

percentages of the baseline budget.

Control thresholds

rules define how Earned Value Management will be implemented, including which

techniques will be used and how progress will be measured.

Performance

measurement

specify how cost information will be presented to stakeholders, including frequency, detail

level, and distribution methods.

Reporting formats

This is the degree to which cost estimates will be rounded up or down (US$995.59 to

US$1,000), based on the scope of the activities and magnitude of the project.

Level of precision

The acceptable range (±10%) used in determining realistic cost estimates is specified, and

may include an amount for contingencies.

Level of accuracy

9.

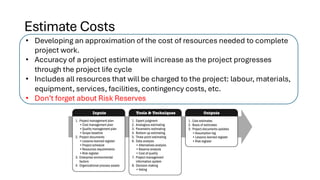

Estimate Costs

• Developingan approximation of the cost of resources needed to complete

project work.

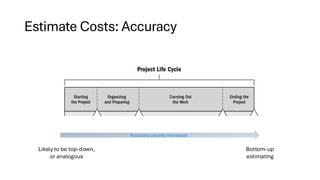

• Accuracy of a project estimate will increase as the project progresses

through the project life cycle

• Includes all resources that will be charged to the project: labour, materials,

equipment, services, facilities, contingency costs, etc.

• Don’t forget about Risk Reserves

Estimate Costs: Accuracy

AdvantagesDisadvatages

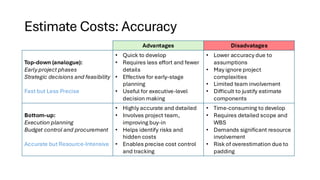

Top-down (analogue):

Early project phases

Strategic decisions and feasibility

Fast but Less Precise

• Quick to develop

• Requires less effort and fewer

details

• Effective for early-stage

planning

• Useful for executive-level

decision making

• Lower accuracy due to

assumptions

• May ignore project

complexities

• Limited team involvement

• Difficult to justify estimate

components

Bottom-up:

Execution planning

Budget control and procurement

Accurate but Resource-Intensive

• Highly accurate and detailed

• Involves project team,

improving buy-in

• Helps identify risks and

hidden costs

• Enables precise cost control

and tracking

• Time-consuming to develop

• Requires detailed scope and

WBS

• Demands significant resource

involvement

• Risk of overestimation due to

padding

12.

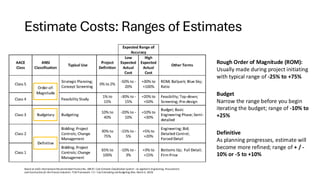

Estimate Costs: Rangesof Estimates

Rough Order of Magnitude (ROM):

Usually made during project initiating

with typical range of -25% to +75%

Budget

Narrow the range before you begin

iterating the budget; range of -10% to

+25%

Definitive

As planning progresses, estimate will

become more refined; range of + / -

10% or -5 to +10%

Based on AACE International Recommended PracticeNo. 18R-97: Cost Estimate Classification System – As Applied in Engineering, Procurement,

and Construction for the Process Industries. TCMFramework: 7.3 – CostEstimating and Budgeting (Rev. March 6, 2019)

13.

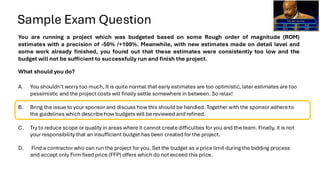

Sample Exam Question

Youare running a project which was budgeted based on some Rough order of magnitude (ROM)

estimates with a precision of -50% /+100%. Meanwhile, with new estimates made on detail level and

some work already finished, you found out that these estimates were consistently too low and the

budget will not be sufficient to successfully run and finish the project.

What should you do?

A. You shouldn’t worry too much, It is quite normal that early estimates are too optimistic, later estimates are too

pessimistic and the project costs will finally settle somewhere in between. So relax!

B. Bring the issue to your sponsor and discuss how this should be handled. Together with the sponsor adhere to

the guidelines which describe how budgets will be reviewed and refined.

C. Try to reduce scope or quality in areas where it cannot create difficulties for you and the team. Finally, it is not

your responsibility that an insufficient budget has been created for the project.

D. Find a contractor who can run the project for you. Set the budget as a price limit during the bidding process

and accept only Firm fixed price (FFP) offers which do not exceed this price.

14.

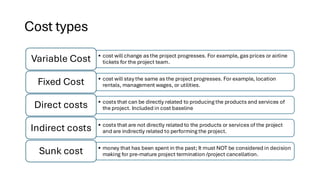

Cost types

• costwill change as the project progresses. For example, gas prices or airline

tickets for the project team.

Variable Cost

• cost will stay the same as the project progresses. For example, location

rentals, management wages, or utilities.

Fixed Cost

• costs that can be directly related to producing the products and services of

the project. Included in cost baseline

Direct costs

• costs that are not directly related to the products or services of the project

and are indirectly related to performing the project.

Indirect costs

• money that has been spent in the past; It must NOT be considered in decision

making for pre-mature project termination /project cancellation.

Sunk cost

15.

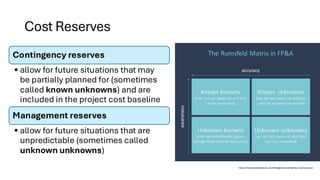

Cost Reserves

Contingency reserves

•allow for future situations that may

be partially planned for (sometimes

called known unknowns) and are

included in the project cost baseline

Management reserves

• allow for future situations that are

unpredictable (sometimes called

unknown unknowns)

https://www.fpandaclub.com/insights/uncertainty-is-all-around

16.

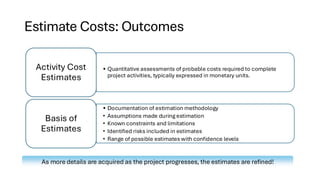

Estimate Costs: Outcomes

•Quantitative assessments of probable costs required to complete

project activities, typically expressed in monetary units.

Activity Cost

Estimates

• Documentation of estimation methodology

• Assumptions made during estimation

• Known constraints and limitations

• Identified risks included in estimates

• Range of possible estimates with confidence levels

Basis of

Estimates

As more details are acquired as the project progresses, the estimates are refined!

17.

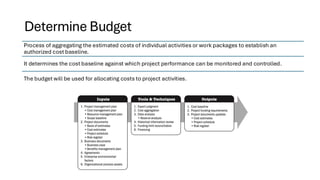

Determine Budget

Process ofaggregating the estimated costs of individual activities or work packages to establish an

authorized cost baseline.

It determines the cost baseline against which project performance can be monitored and controlled.

The budget will be used for allocating costs to project activities.

18.

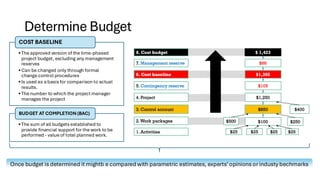

Determine Budget

•The approvedversion of the time-phased

project budget, excluding any management

reserves

•Can be changed only through formal

change control procedures

•Is used as a basis for comparison to actual

results.

•The number to which the project manager

manages the project

COST BASELINE

•The sum of all budgets established to

provide financial support for the work to be

performed - value of total planned work.

BUDGET AT COMPLETION (BAC)

Once budget is determined it mightb e compared with parametric estimates, experts’opinions or industy bechmarks

19.

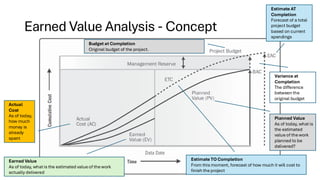

Budget at Completion(BAC)

Determined at project start based on work planned

Used with Planned Value (PV) to determine budget’s status against

planned

Compared to Estimate at Completion (EAC) at point of analysis

based on expected future work

Expressed in cost units (any currency)

20.

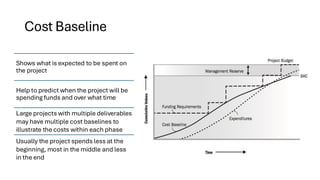

Cost Baseline

Shows whatis expected to be spent on

the project

Help to predict when the project will be

spending funds and over what time

Large projects with multiple deliverables

may have multiple cost baselines to

illustrate the costs within each phase

Usually the project spends less at the

beginning, most in the middle and less

in the end

21.

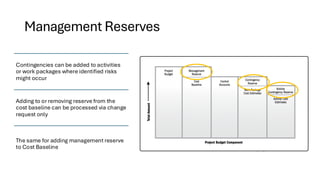

Management Reserves

Contingencies canbe added to activities

or work packages where identified risks

might occur

Adding to or removing reserve from the

cost baseline can be processed via change

request only

The same for adding management reserve

to Cost Baseline

22.

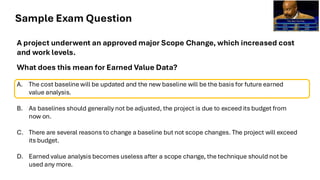

Sample Exam Question

Aproject underwent an approved major Scope Change, which increased cost

and work levels.

What does this mean for Earned Value Data?

A. The cost baseline will be updated and the new baseline will be the basis for future earned

value analysis.

B. As baselines should generally not be adjusted, the project is due to exceed its budget from

now on.

C. There are several reasons to change a baseline but not scope changes. The project will exceed

its budget.

D. Earned value analysis becomes useless after a scope change, the technique should not be

used any more.

23.

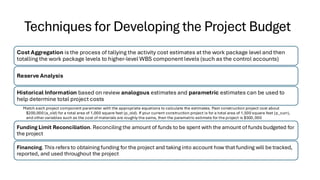

Techniques for Developingthe Project Budget

Cost Aggregation is the process of tallying the activity cost estimates at the work package level and then

totalling the work package levels to higher-level WBS component levels (such as the control accounts)

Reserve Analysis

Historical Information based on review analogous estimates and parametric estimates can be used to

help determine total project costs

Match each project component parameter with the appropriate equations to calculate the estimates. Past construction project cost about

$200,000 (a_old) for a total area of 1,000 square feet (p_old). If your current construction project is for a total area of 1,500 square feet (p_curr),

and other variables such as the cost of materials are roughly the same, then the parametric estimate for the project is $300,000

Funding Limit Reconciliation. Reconciling the amount of funds to be spent with the amount of funds budgeted for

the project

Financing. This refers to obtaining funding for the project and taking into account how that funding will be tracked,

reported, and used throughout the project

24.

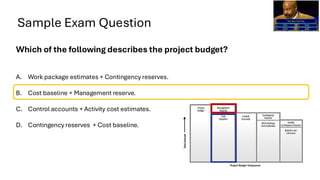

Sample Exam Question

Whichof the following describes the project budget?

A. Work package estimates + Contingency reserves.

B. Cost baseline + Management reserve.

C. Control accounts + Activity cost estimates.

D. Contingency reserves + Cost baseline.

25.

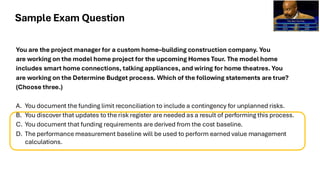

You are theproject manager for a custom home–building construction company. You

are working on the model home project for the upcoming Homes Tour. The model home

includes smart home connections, talking appliances, and wiring for home theatres. You

are working on the Determine Budget process. Which of the following statements are true?

(Choose three.)

A. You document the funding limit reconciliation to include a contingency for unplanned risks.

B. You discover that updates to the risk register are needed as a result of performing this process.

C. You document that funding requirements are derived from the cost baseline.

D. The performance measurement baseline will be used to perform earned value management

calculations.

Sample Exam Question

26.

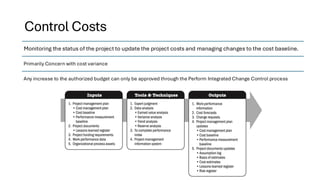

Control Costs

Monitoring thestatus of the project to update the project costs and managing changes to the cost baseline.

Primarily Concern with cost variance

Any increase to the authorized budget can only be approved through the Perform Integrated Change Control process

27.

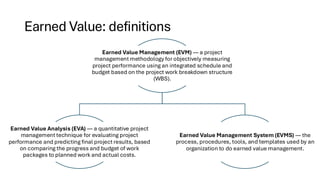

Earned Value: definitions

EarnedValue Management (EVM) — a project

management methodology for objectively measuring

project performance using an integrated schedule and

budget based on the project work breakdown structure

(WBS).

Earned Value Analysis (EVA) — a quantitative project

management technique for evaluating project

performance and predicting final project results, based

on comparing the progress and budget of work

packages to planned work and actual costs.

Earned Value Management System (EVMS) — the

process, procedures, tools, and templates used by an

organization to do earned value management.

28.

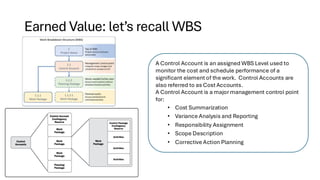

Earned Value: let’srecall WBS

A Control Account is an assigned WBS Level used to

monitor the cost and schedule performance of a

significant element of the work. Control Accounts are

also referred to as Cost Accounts.

A Control Account is a major management control point

for:

• Cost Summarization

• Variance Analysis and Reporting

• Responsibility Assignment

• Scope Description

• Corrective Action Planning

29.

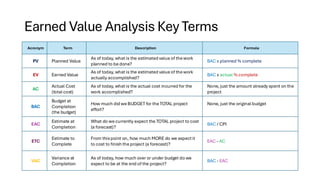

Earned Value AnalysisKey Terms

Acronym Term Description Formula

PV Planned Value

As of today, whatis the estimated value of the work

planned to be done?

BAC x planned % complete

EV Earned Value

As of today, whatis the estimated value of the work

actually accomplished?

BAC x actual % complete

AC

Actual Cost

(total cost)

As of today, whatis the actual cost incurred for the

work accomplished?

None, just the amount already spent on the

project

BAC

Budget at

Completion

(the budget)

How much did we BUDGET for the TOTAL project

effort?

None, just the original budget

EAC

Estimate at

Completion

What do we currently expect the TOTAL project to cost

(a forecast)?

BAC / CPI

ETC

Estimate to

Complete

From thispoint on, how much MORE do we expectit

to cost to finish the project (a forecast)?

EAC - AC

VAC

Variance at

Completion

As of today, how much over or under budget do we

expect to be at the end of the project?

BAC - EAC

30.

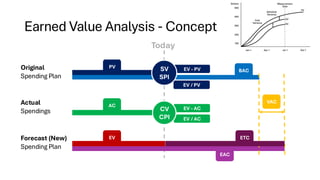

Earned Value Analysis- Concept

Original

Spending Plan

Actual

Spendings

Forecast (New)

Spending Plan

Today

PV

AC

BAC

ETC

EV

EAC

VAC

EV - PV

EV / PV

EV - AC

EV / AC

CV

CPI

SV

SPI

31.

Earned Value Analysis- Concept

Earned Value

As of today, whatis the estimated value of the work

actually delivered

Estimate TO Completion

From thismoment, forecast of how much it will cost to

finish the project

Estimate AT

Completion

Forecast of a total

project budget

based on current

spendings

Variance at

Completion

The difference

between the

original budget

Budget at Completion

Original budget of the project.

Planned Value

As of today, whatis

the estimated

value of the work

planned to be

delivered?

Actual

Cost

As of today,

how much

money is

already

spent

32.

Earned Value: Varianceand Performance Analysis

Acronym Term Description Formula

CV Cost variance The difference between earned value and actual cost. Negative isover budget EV-AC

SV

Schedule

Variance

The difference between earned value and planned value. Negative isbehind

schedule

EV - PV

CPI

Cost

Performance

Index

How efficient is my project?

• Is a measure of the cost efficiency of budgeted resources, expressed as a

ratio of earned value to actual cost.

• CPI shows how well the project is sticking to the budget

• “Every dollar the project spends, we do $X (below or above 1) worth of work

on this project”

• “We are X% under or over budgetat this point in the project”

EV/AC

SPI

Schedule

Performance

Index

The baseline schedule efficiency factor representing the relationship between

the earned value achieved versusplanned value. >1 is good

EV/PV

TCPI

To Complete

Performance

Index

The result of dividing the remaining budget according to the plan by the actually

available budget (consideringexistingcost variances).

From now on, how well do we need to perform to meet our goal

(BAC – EV) / (BAC – AC)

remaining work /

remaining funds

33.

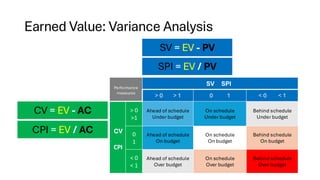

CPI = EV/ AC

SPI = EV / PV

CV = EV - AC

SV = EV - PV

Performance

measures

SV SPI

> 0 > 1 0 1 < 0 < 1

CV

CPI

> 0

>1

Ahead of schedule

Under budget

On schedule

Under budget

Behind schedule

Under budget

0

1

Ahead of schedule

On budget

On schedule

On budget

Behind schedule

On budget

< 0

< 1

Ahead of schedule

Over budget

On schedule

Over budget

Behind schedule

Over budget

Earned Value: Variance Analysis

Forecasting: EAC

EAC isa way to project/estimate the planned cost at project finish based on the currently available data

EAC = BAC/CPI

If we believe the project will continue to spend at the same rate up to now => Normal variant to use

•The delay is caused byreasons which is likelyto continue (e.g. labour with less skilled than expected)

•example: theEAC for the housing project = US$10000 / 0.75= US$13333

EAC = AC + (BAC-EV)

If we believe that future expenditures will occur at the original forecasted amount (no more delays ofthe same kind in future) =>

Ignores a 1-off cost hit, so uses the actuals plus remaining work

•The delay might be caused bysome unforeseen reasons (e.g. typhoon) which is not likely to happen again

•example: theEAC for the housing project = US$4000 + (US$10000 – $3000) = US$11000

EAC = AC + [(BAC-EV)/(SPI*CPI)]

If we believe that both current cost and current schedule performance will impact future cost performance => Project end date must be met

•The performance of the project willcontinue with sub-prime standards (overbudget and behind schedule)

•example: theEAC for the housing project = US$4000 + [(US$10000 – $3000)/(0.75*0.75)] = US$16444

EAC = AC + New Estimate

If we believe the original conditions and assumptions are wrong => When the project is“broken” the baseline is untenable

36.

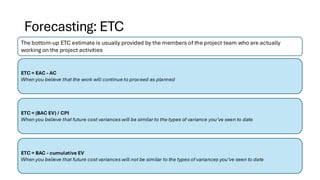

Forecasting: ETC

The bottom-upETC estimate is usually provided by the members of the project team who are actually

working on the project activities

ETC = EAC - AC

When you believe that the work will continue to proceed as planned

ETC = (BAC EV) / CPI

When you believe that future cost variances will be similar to the types of variance you’ve seen to date

ETC = BAC - cumulative EV

When you believe that future cost variances will not be similar to the types of variances you’ve seen to date

37.

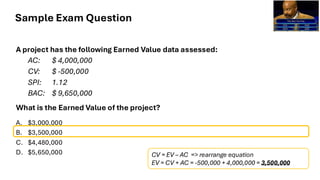

Sample Exam Question

Aproject has the following Earned Value data assessed:

AC: $ 4,000,000

CV: $ -500,000

SPI: 1.12

BAC: $ 9,650,000

What is the Earned Value of the project?

A. $3,000,000

B. $3,500,000

C. $4,480,000

D. $5,650,000 CV = EV – AC => rearrange equation

EV = CV + AC = -500,000 + 4,000,000 = 3,500,000

38.

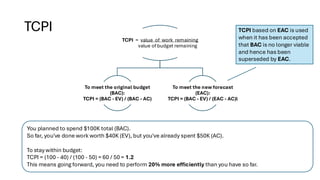

TCPI

TCPI = valueof work remaining

value of budget remaining

To meet the original budget

(BAC):

TCPI = (BAC - EV) / (BAC - AC)

To meet the new forecast

(EAC):

TCPI = (BAC - EV) / (EAC - AC)l

You planned to spend $100K total (BAC).

So far, you've done work worth $40K (EV), but you've already spent $50K (AC).

To stay within budget:

TCPI = (100 - 40) / (100 - 50) = 60 / 50 = 1.2

This means going forward, you need to perform 20% more efficiently than you have so far.

TCPI based on EAC is used

when it has been accepted

that BAC is no longer viable

and hence has been

superseded by EAC.

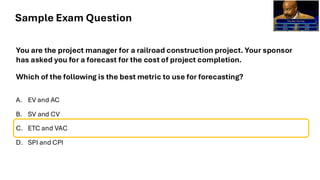

Sample Exam Question

Youare the project manager for a railroad construction project. Your sponsor

has asked you for a forecast for the cost of project completion.

Which of the following is the best metric to use for forecasting?

A. EV and AC

B. SV and CV

C. ETC and VAC

D. SPI and CPI

41.

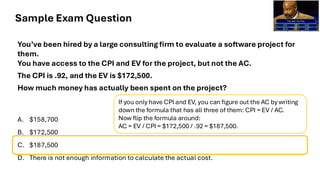

Sample Exam Question

You’vebeen hired by a large consulting firm to evaluate a software project for

them.

You have access to the CPI and EV for the project, but not the AC.

The CPI is .92, and the EV is $172,500.

How much money has actually been spent on the project?

A. $158,700

B. $172,500

C. $187,500

D. There is not enough information to calculate the actual cost.

If you only have CPI and EV, you can figure out the AC by writing

down the formula that has all three of them: CPI = EV / AC.

Now flip the formula around:

AC = EV / CPI = $172,500 / .92 = $187,500.

42.

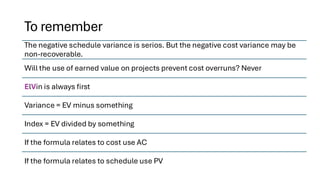

To remember

The negativeschedule variance is serios. But the negative cost variance may be

non-recoverable.

Will the use of earned value on projects prevent cost overruns? Never

ElVin is always first

Variance = EV minus something

Index = EV divided by something

If the formula relates to cost use AC

If the formula relates to schedule use PV

43.

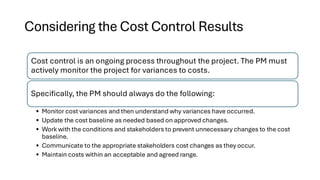

Considering the CostControl Results

Cost control is an ongoing process throughout the project. The PM must

actively monitor the project for variances to costs.

Specifically, the PM should always do the following:

• Monitor cost variances and then understand why variances have occurred.

• Update the cost baseline as needed based on approved changes.

• Work with the conditions and stakeholders to prevent unnecessary changes to the cost

baseline.

• Communicate to the appropriate stakeholders cost changes as they occur.

• Maintain costs within an acceptable and agreed range.

44.

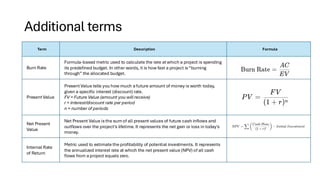

Additional terms

Term DescriptionFormula

Burn Rate

Formula-based metric used to calculate the rate atwhich a project is spending

its predefined budget. In other words, it is how fast a project is“burning

through” the allocated budget.

PresentValue

PresentValue tells you how much a future amount of money is worth today,

given a specific interest (discount) rate.

FV = Future Value (amount you will receive)

r = interest/discount rate per period

n = number of periods

Net Present

Value

Net Present Value isthe sumof all present values of future cash inflows and

outflows over the project’s lifetime. It represents the net gain or loss in today's

money.

Internal Rate

of Return

Metric used to estimate the profitability of potential investments. It represents

the annualized interest rate at which the net present value (NPV) of all cash

flows from a project equals zero.

![Forecasting: EAC

EAC is a way to project/estimate the planned cost at project finish based on the currently available data

EAC = BAC/CPI

If we believe the project will continue to spend at the same rate up to now => Normal variant to use

•The delay is caused byreasons which is likelyto continue (e.g. labour with less skilled than expected)

•example: theEAC for the housing project = US$10000 / 0.75= US$13333

EAC = AC + (BAC-EV)

If we believe that future expenditures will occur at the original forecasted amount (no more delays ofthe same kind in future) =>

Ignores a 1-off cost hit, so uses the actuals plus remaining work

•The delay might be caused bysome unforeseen reasons (e.g. typhoon) which is not likely to happen again

•example: theEAC for the housing project = US$4000 + (US$10000 – $3000) = US$11000

EAC = AC + [(BAC-EV)/(SPI*CPI)]

If we believe that both current cost and current schedule performance will impact future cost performance => Project end date must be met

•The performance of the project willcontinue with sub-prime standards (overbudget and behind schedule)

•example: theEAC for the housing project = US$4000 + [(US$10000 – $3000)/(0.75*0.75)] = US$16444

EAC = AC + New Estimate

If we believe the original conditions and assumptions are wrong => When the project is“broken” the baseline is untenable](https://image.slidesharecdn.com/lempmpcost-251007182834-04159d01/85/Maksym-Vyshnivetskyi-Cost-UA-35-320.jpg)