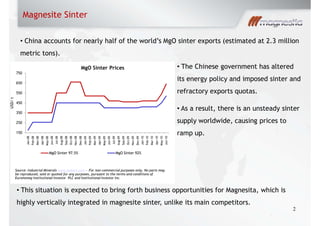

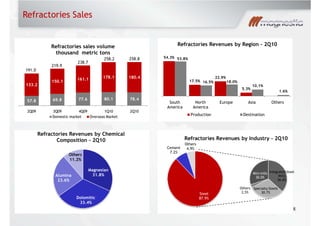

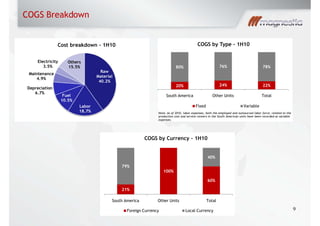

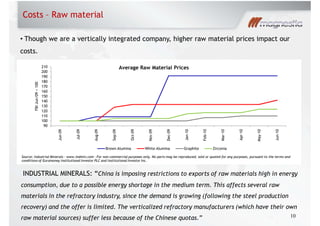

China has imposed export quotas on magnesite sinter and refractory materials due to energy policy changes and potential shortages. This has led to an unstable global supply and higher prices. Magnesita is well positioned as it is highly vertically integrated in magnesite sinter production, unlike its main competitors. Magnesita has also seen increased revenues from new contracts using its CPP business model and its financial results have been strong, with adjusted EBITDA growth of 21.7% in 2Q10. However, higher raw material prices impact costs due to supply restrictions from China and increased freight and input costs.