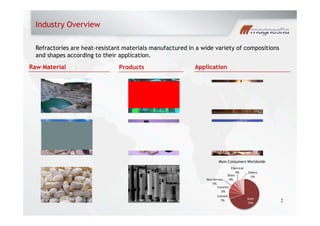

Magnesita is a global refractory company with the largest magnesite reserves in the world. It presented to investors in the second quarter of 2010. Key points included:

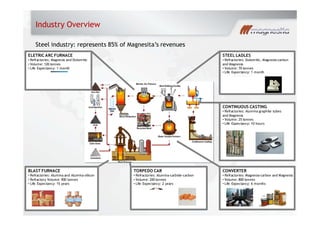

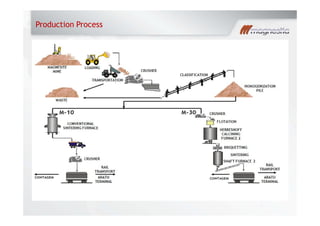

- The steel industry represents 85% of Magnesita's revenues, with refractories used across various steel production processes.

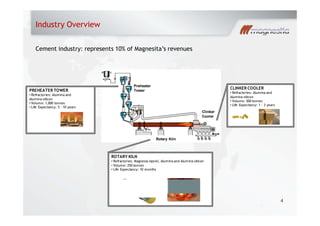

- Cement represents 10% of revenues, with refractories used in rotary kilns, preheaters, and clinker coolers.

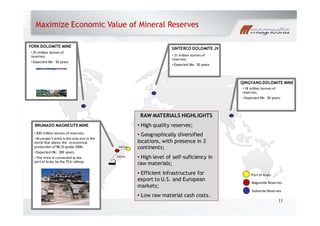

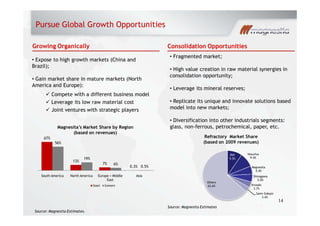

- Magnesita has a global presence with 28 plants across four continents and a focus on high-growth markets like China and Latin America.

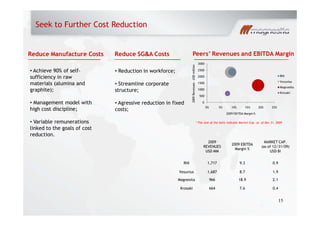

- The company aims to leverage its mineral reserves, pursue global growth opportunities, and further reduce costs.