Downloaded 47 times

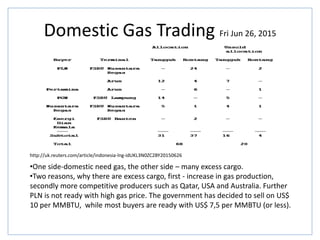

The document discusses Indonesia's natural gas market and LNG trade. It notes that while Indonesia has long exported LNG, domestic gas demand is rising significantly as oil-fired power plants are converted to run on gas. This is creating gas supply shortages within Indonesia. The government is working to address this issue through various strategies like developing new gas infrastructure including pipelines, LNG import terminals, and regulating domestic gas allocation. Japanese companies have traditionally played a major role in Indonesia's LNG industry through investment, technology, and offtake agreements. However, as domestic gas needs grow, Indonesia's gas market is undergoing a transition from primarily export-focused to aiming to also meet strong rising domestic demand.