Downloaded 21 times

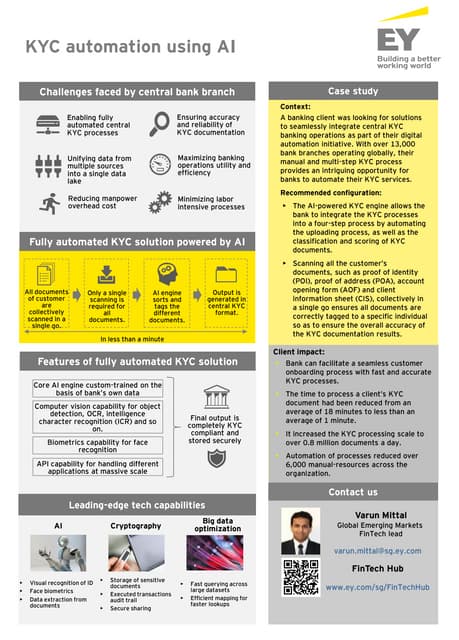

A banking client implemented an AI-powered KYC automation solution to streamline their manual KYC processes across 13,000 global branches, drastically reducing document processing time from 18 minutes to under 1 minute. The AI engine automates document uploading, classification, and scoring, allowing the bank to handle over 0.8 million KYC documents daily while reducing manual resources by over 6,000. Key features include visual recognition, biometrics, and a secure data management system, ensuring compliance and efficient operations.