Downloaded 33 times

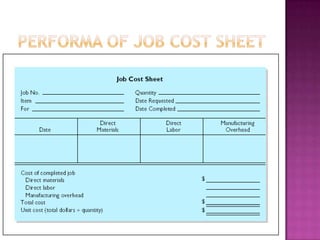

Job costing is a costing technique used when jobs are unique to customer specifications. It involves tracking direct and indirect costs for each job. Job costing is used in industries like construction, shipping, and services where each job differs, to determine the profit or loss of individual jobs and help plan future jobs by comparing actual and estimated costs.