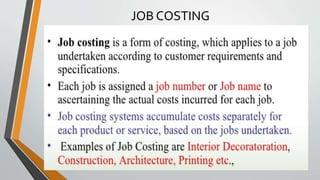

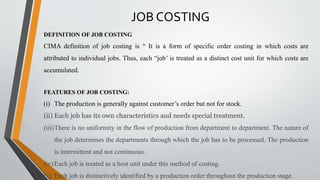

This document discusses different types of cost accounting methods including job costing, batch costing, and contract costing. Job costing tracks costs for individual jobs or orders, with each one treated as a separate cost unit. Batch costing is used when items are produced in batches, with costs collected against each batch. Contract costing is a specialized type of job costing used for long-term contracts like construction projects that span multiple accounting periods. It aims to determine the profit or loss on each contract over its duration and at completion.