Download as PDF, PPTX

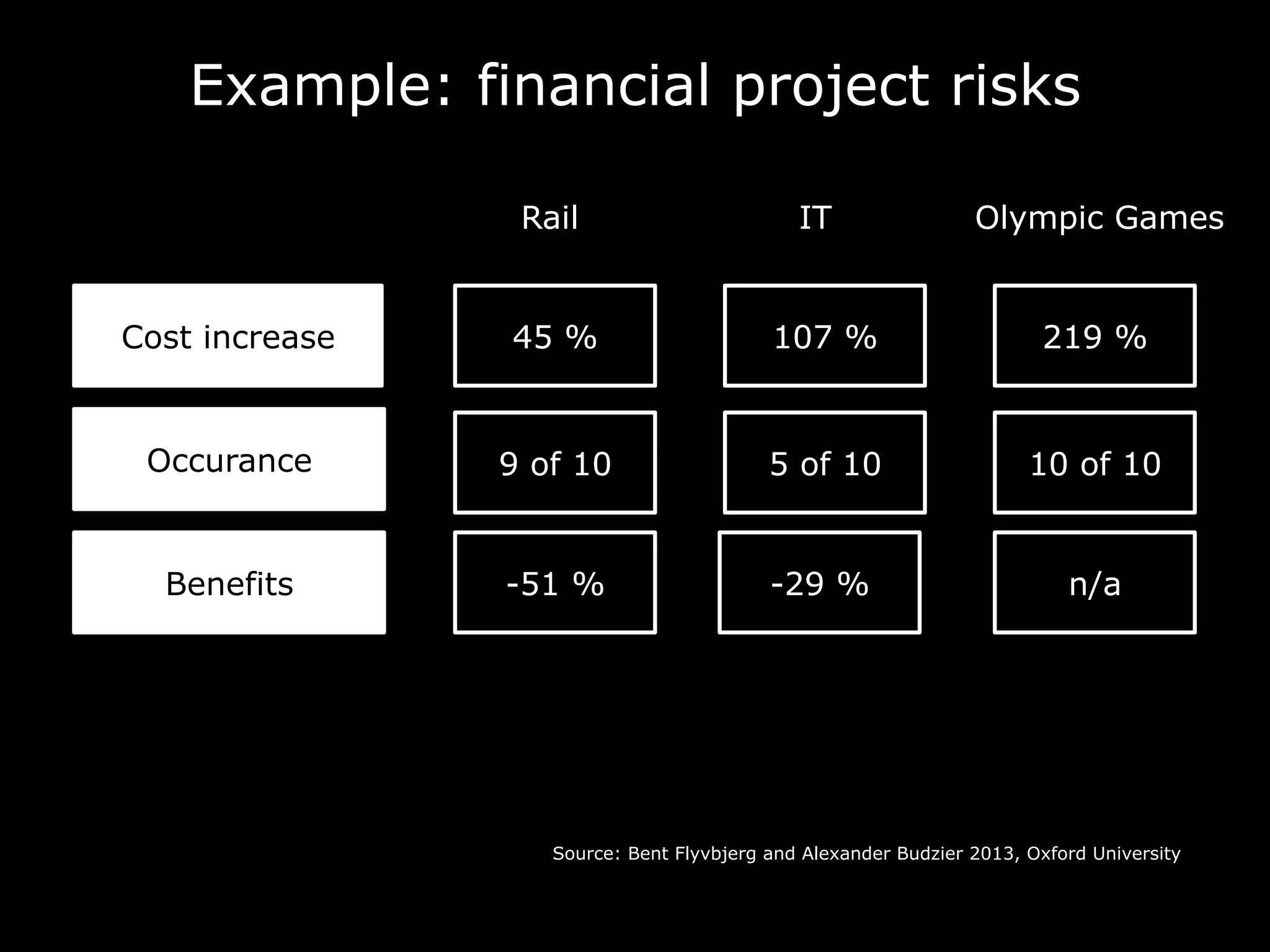

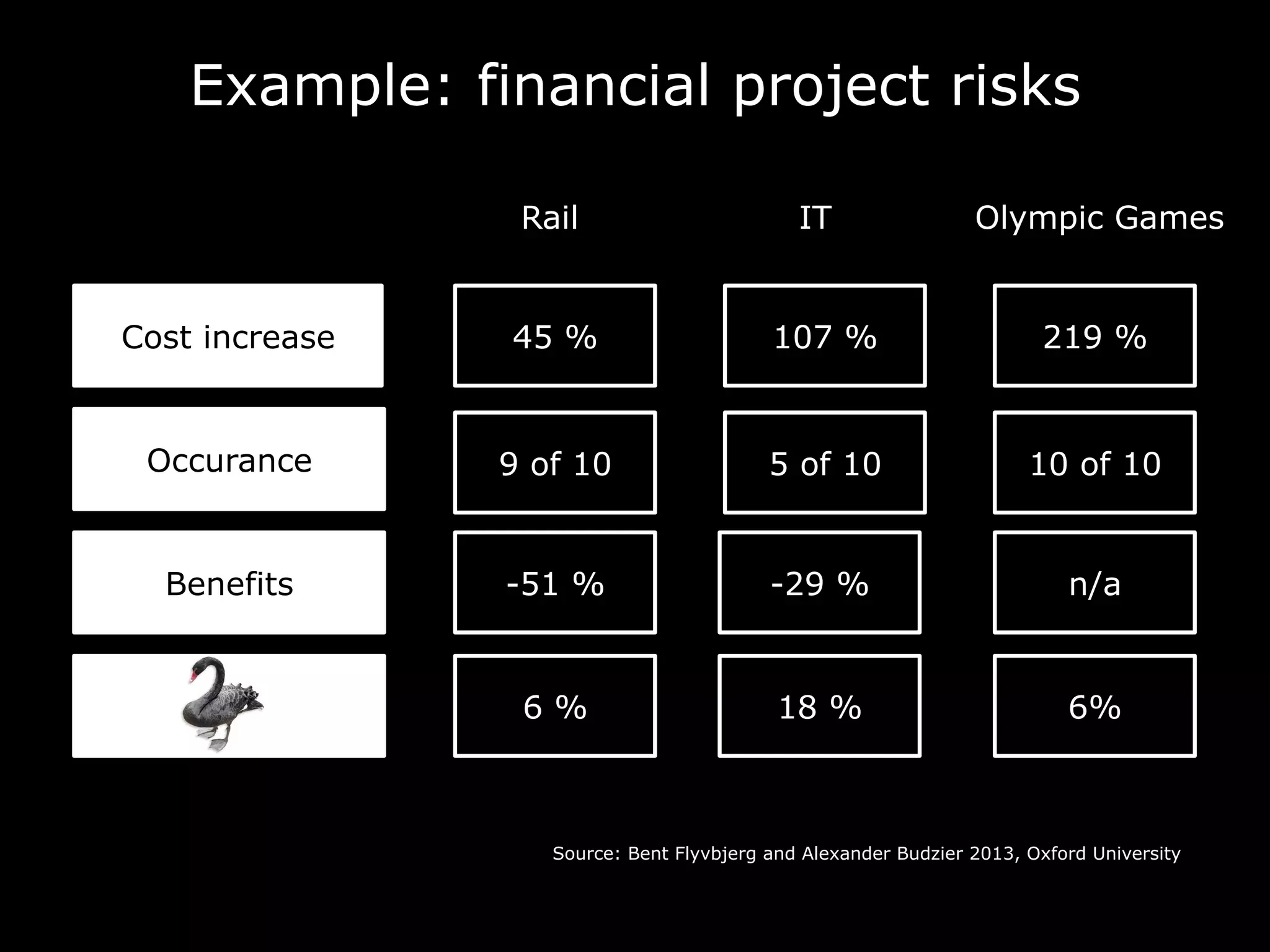

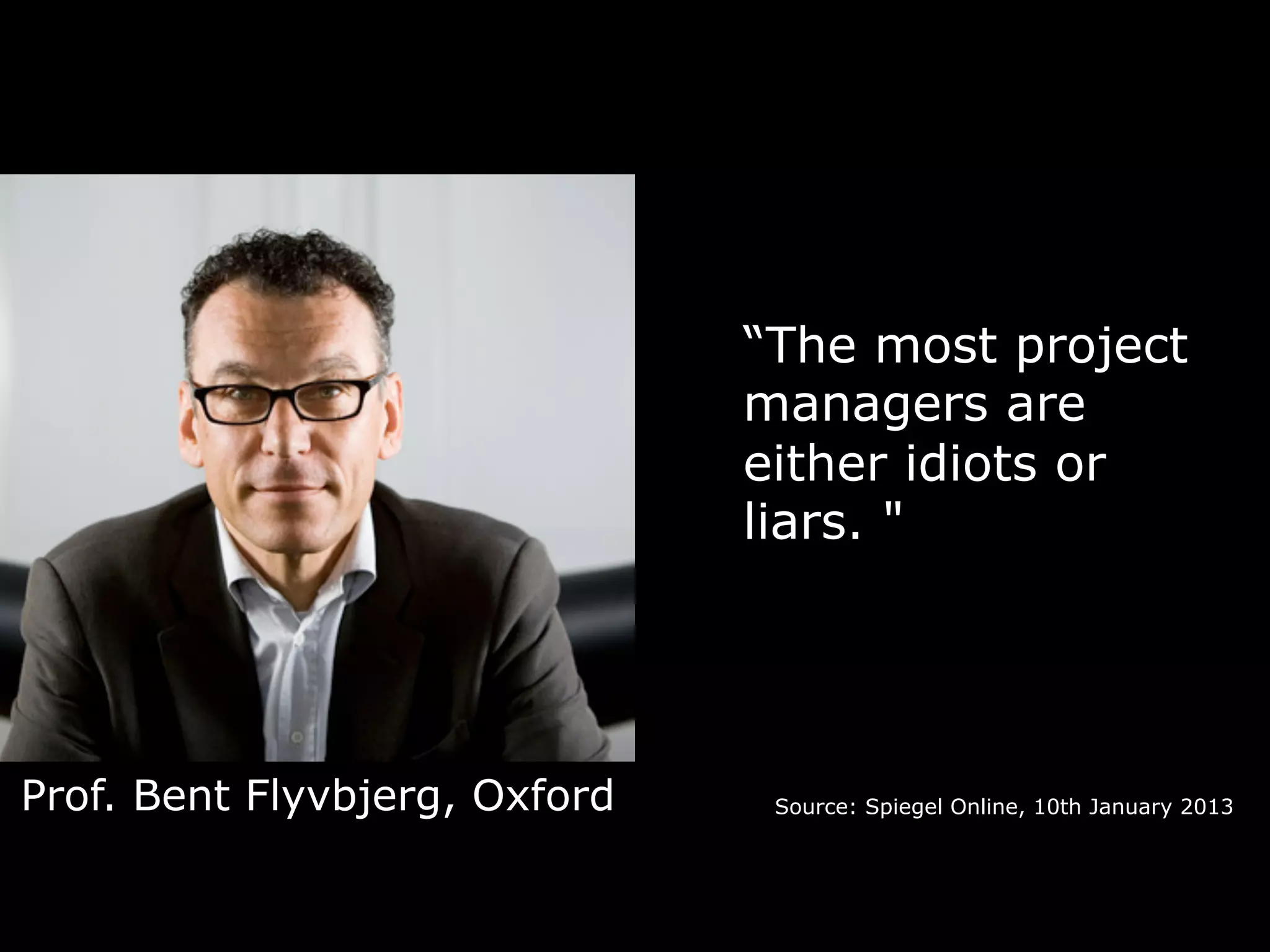

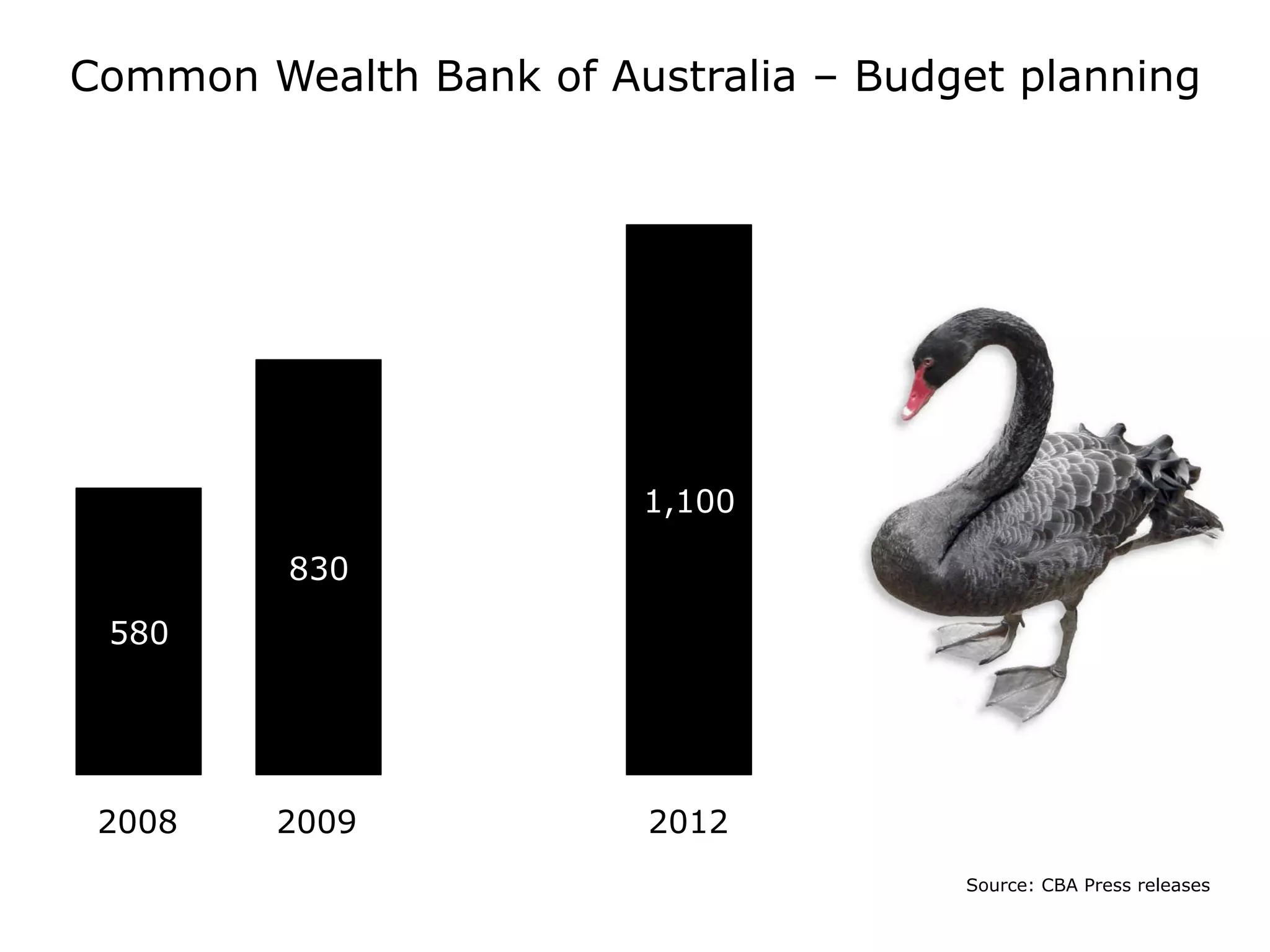

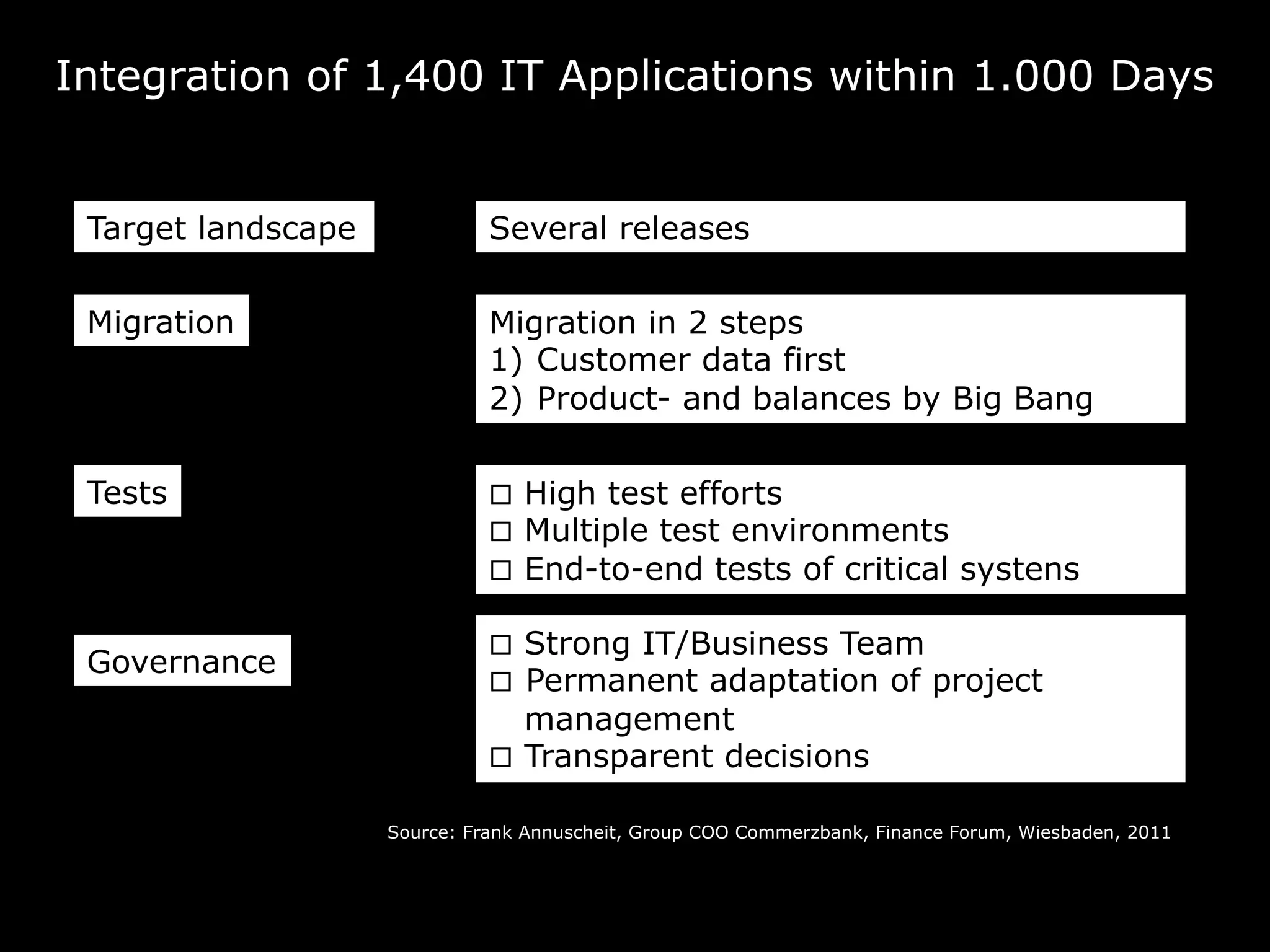

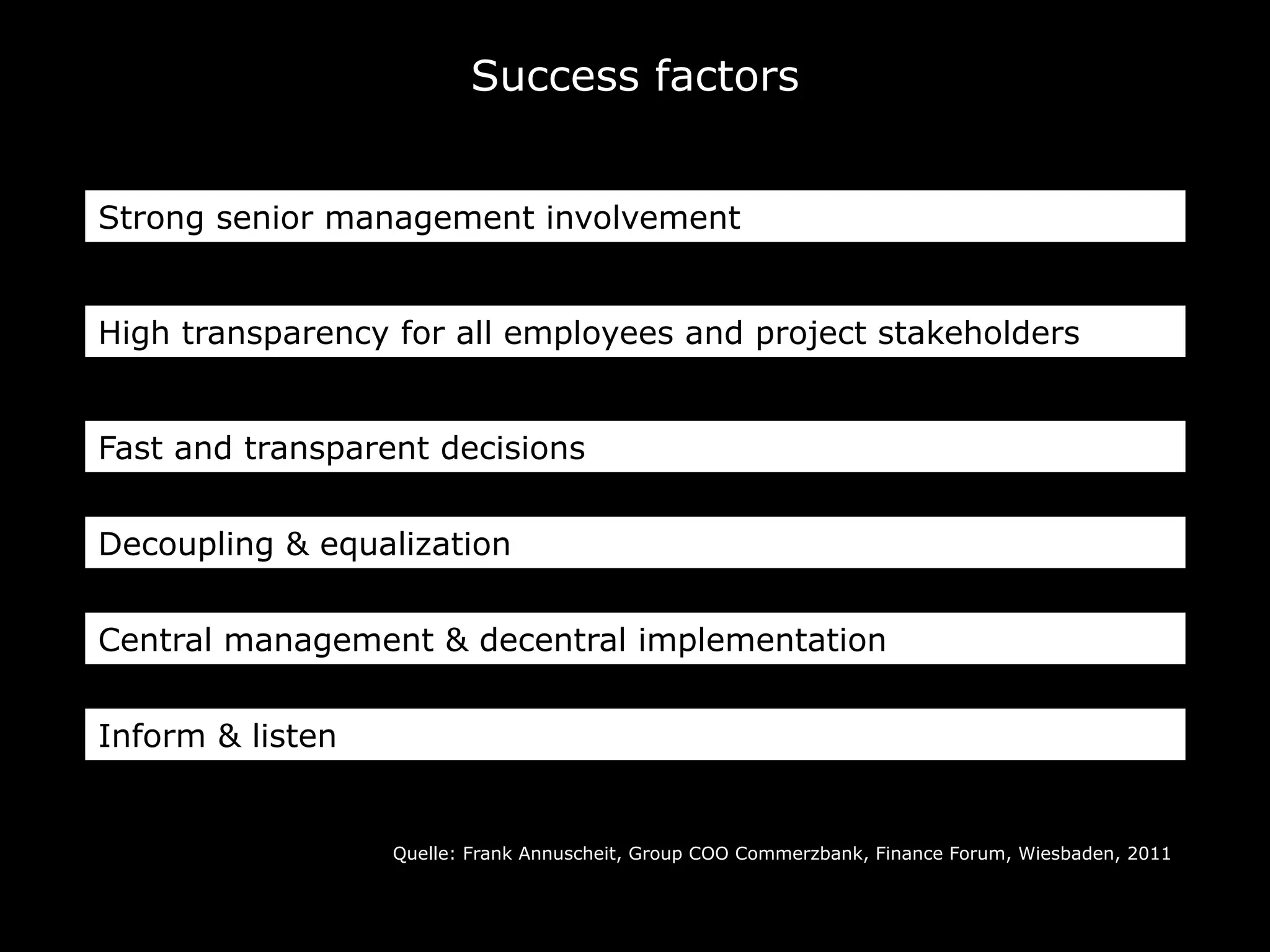

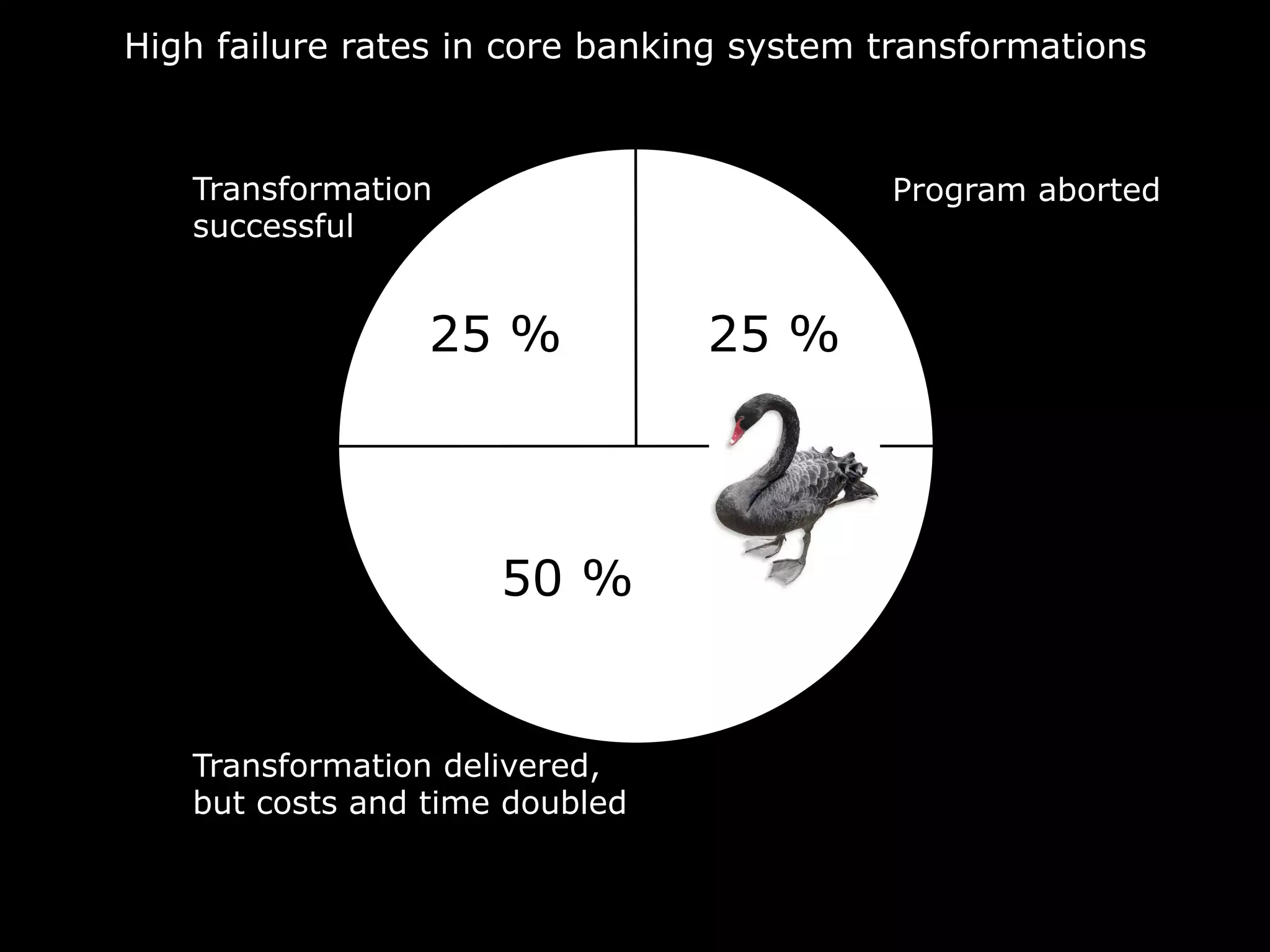

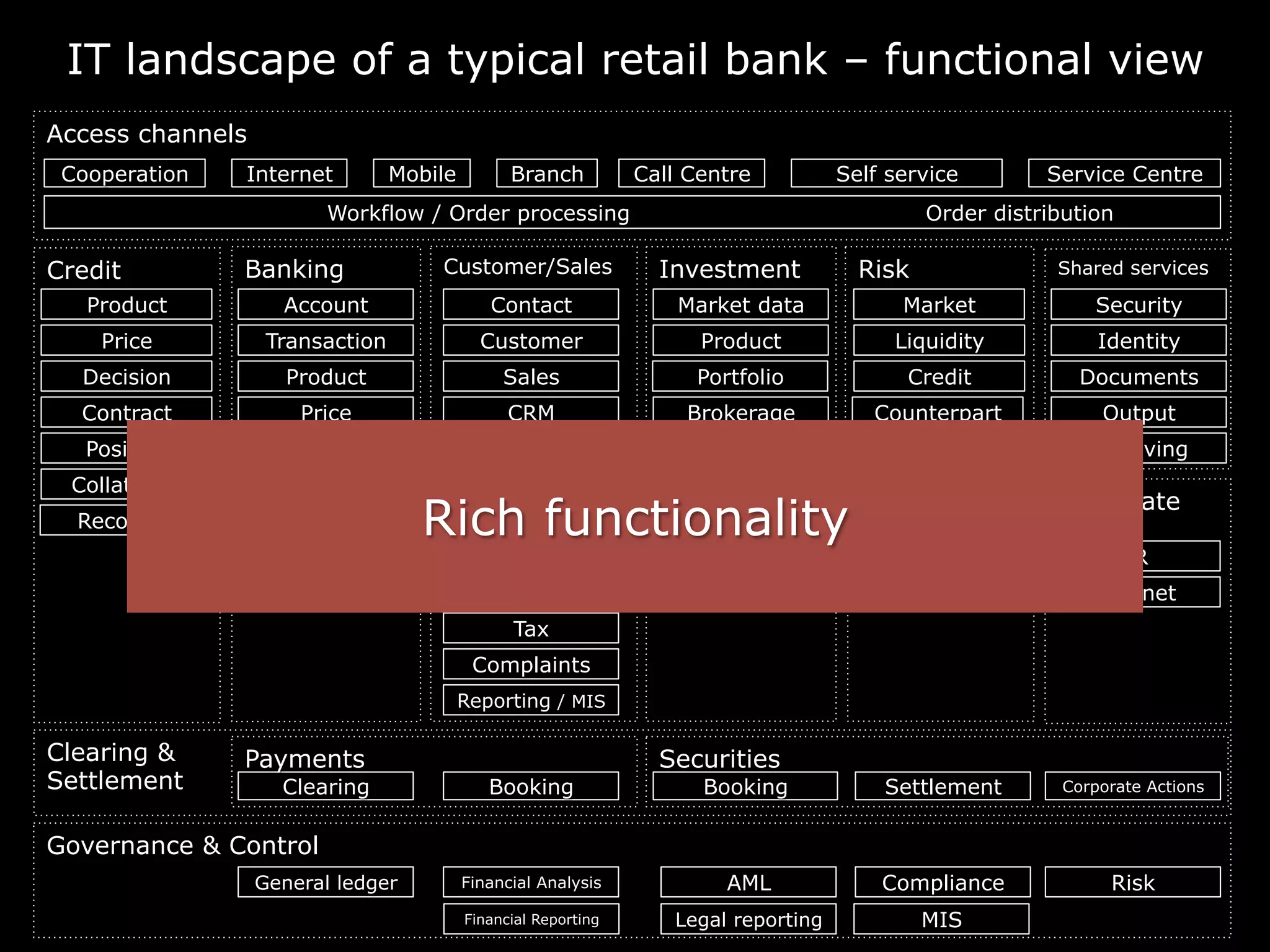

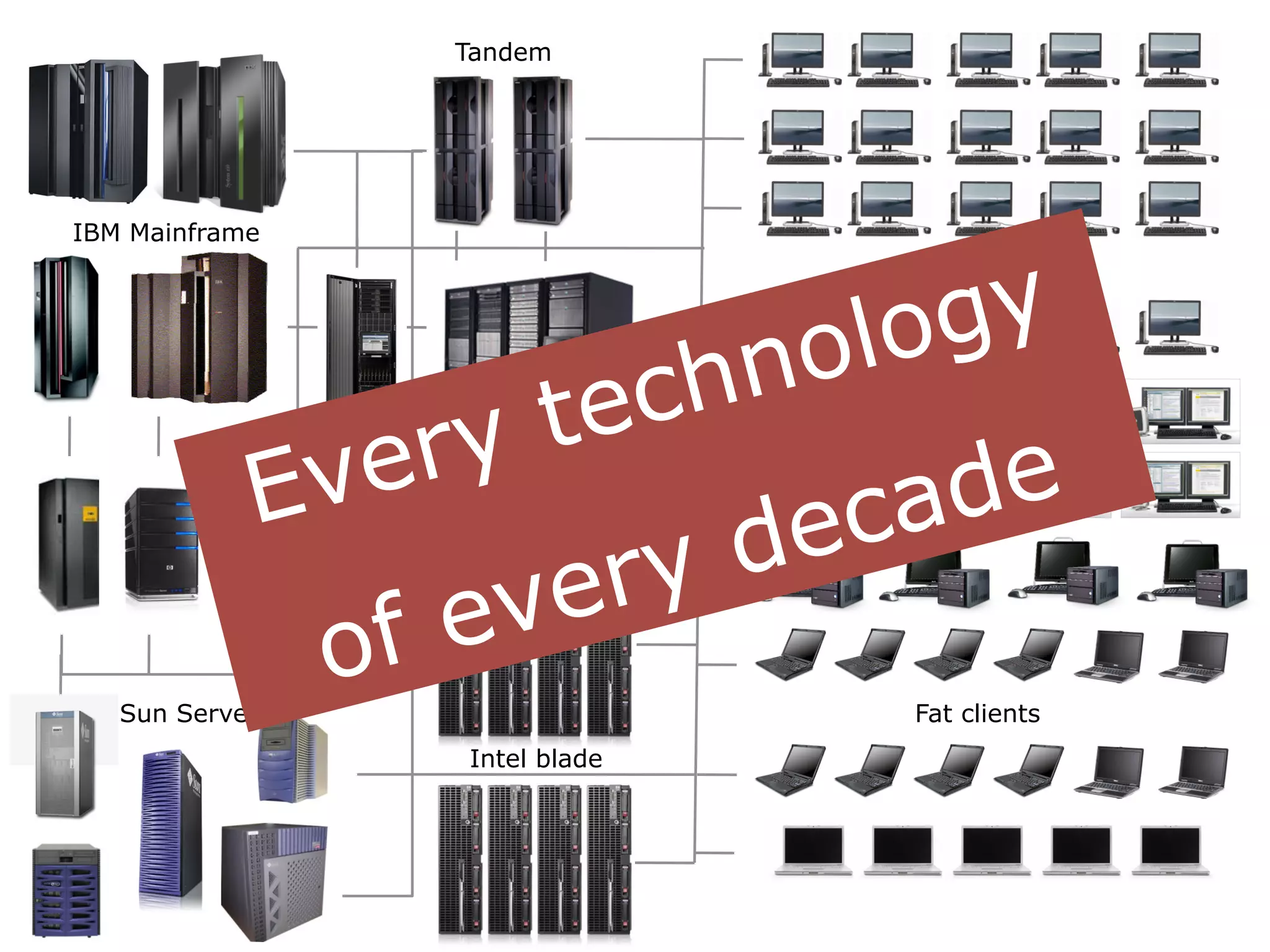

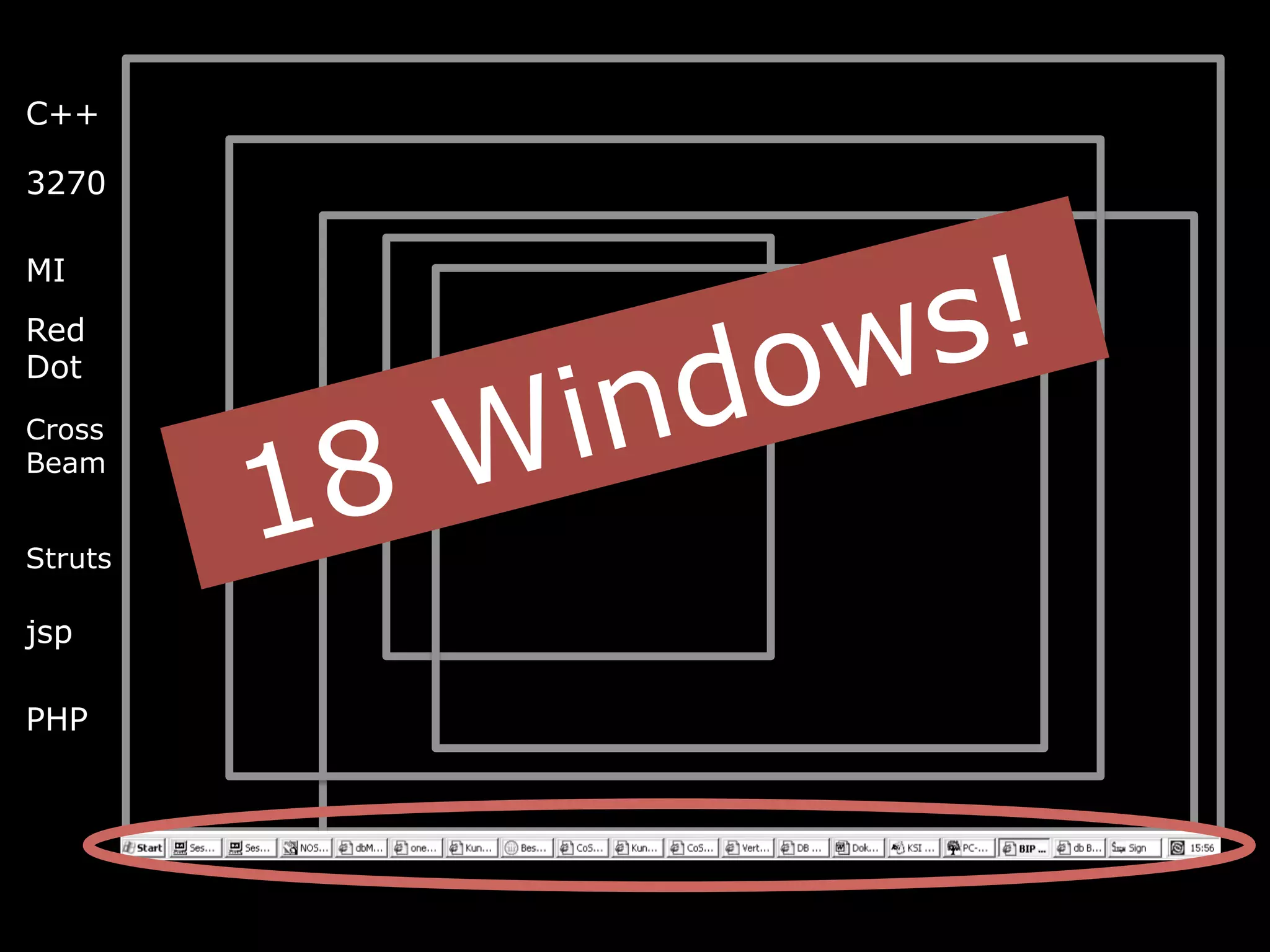

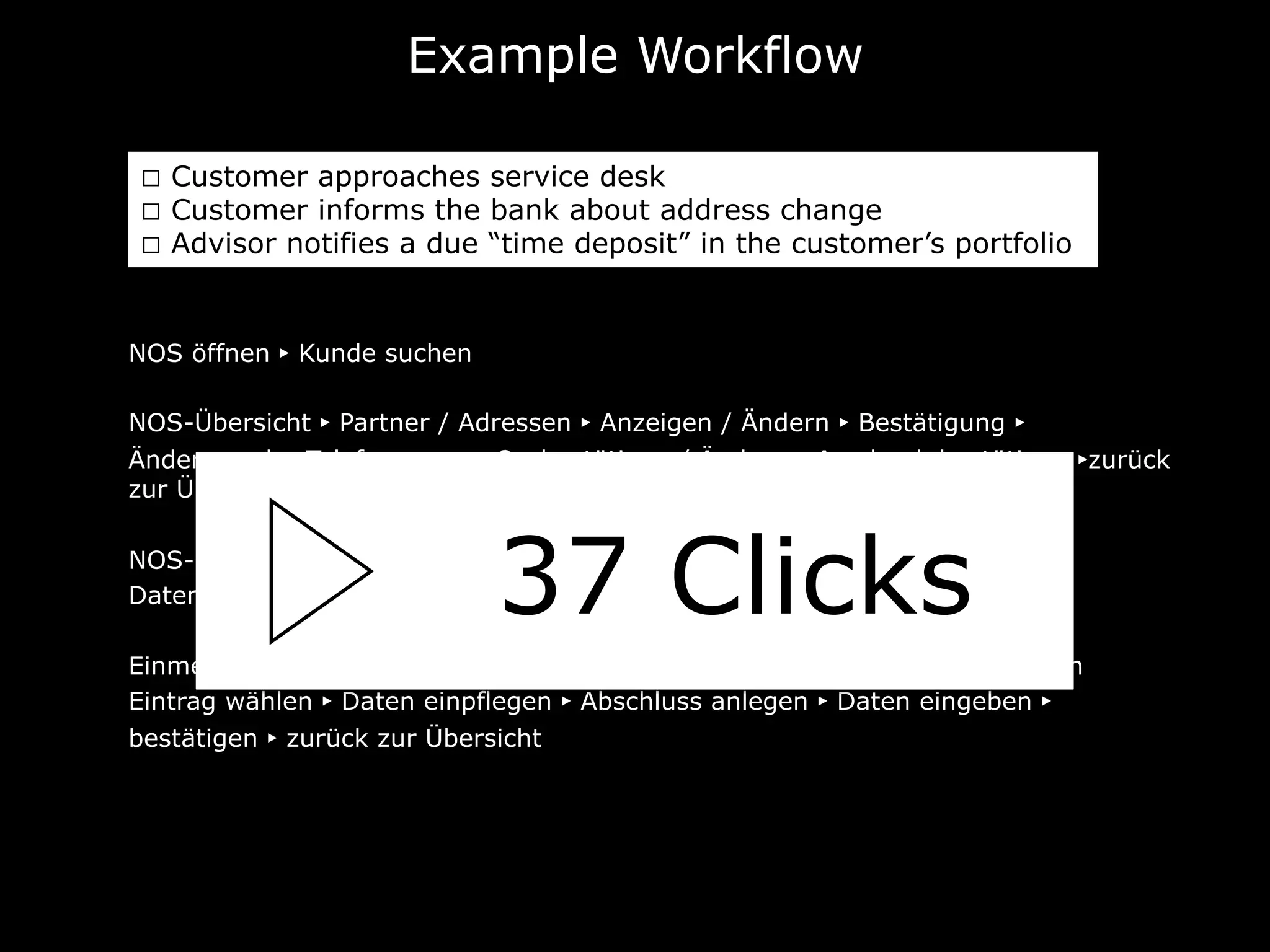

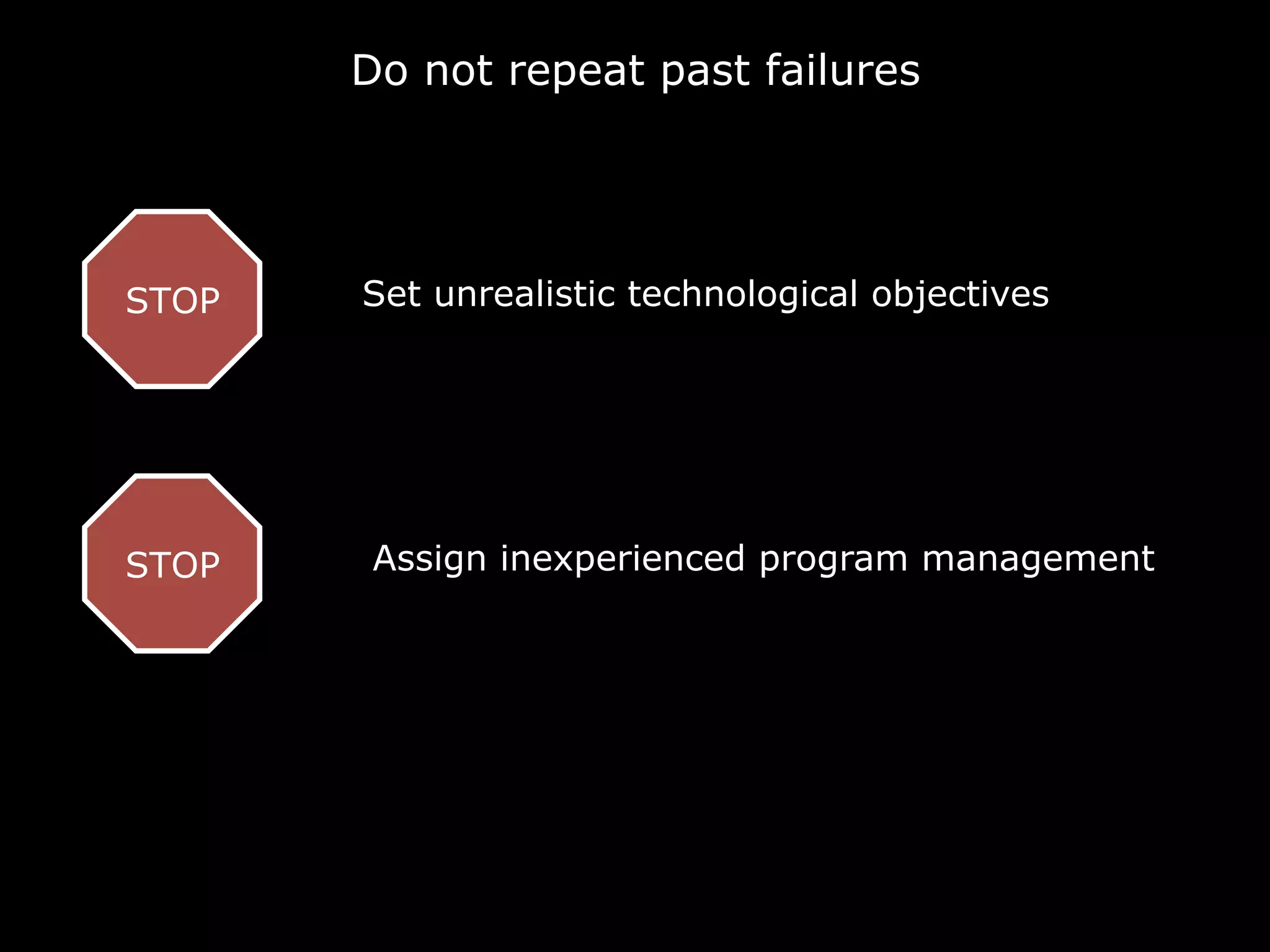

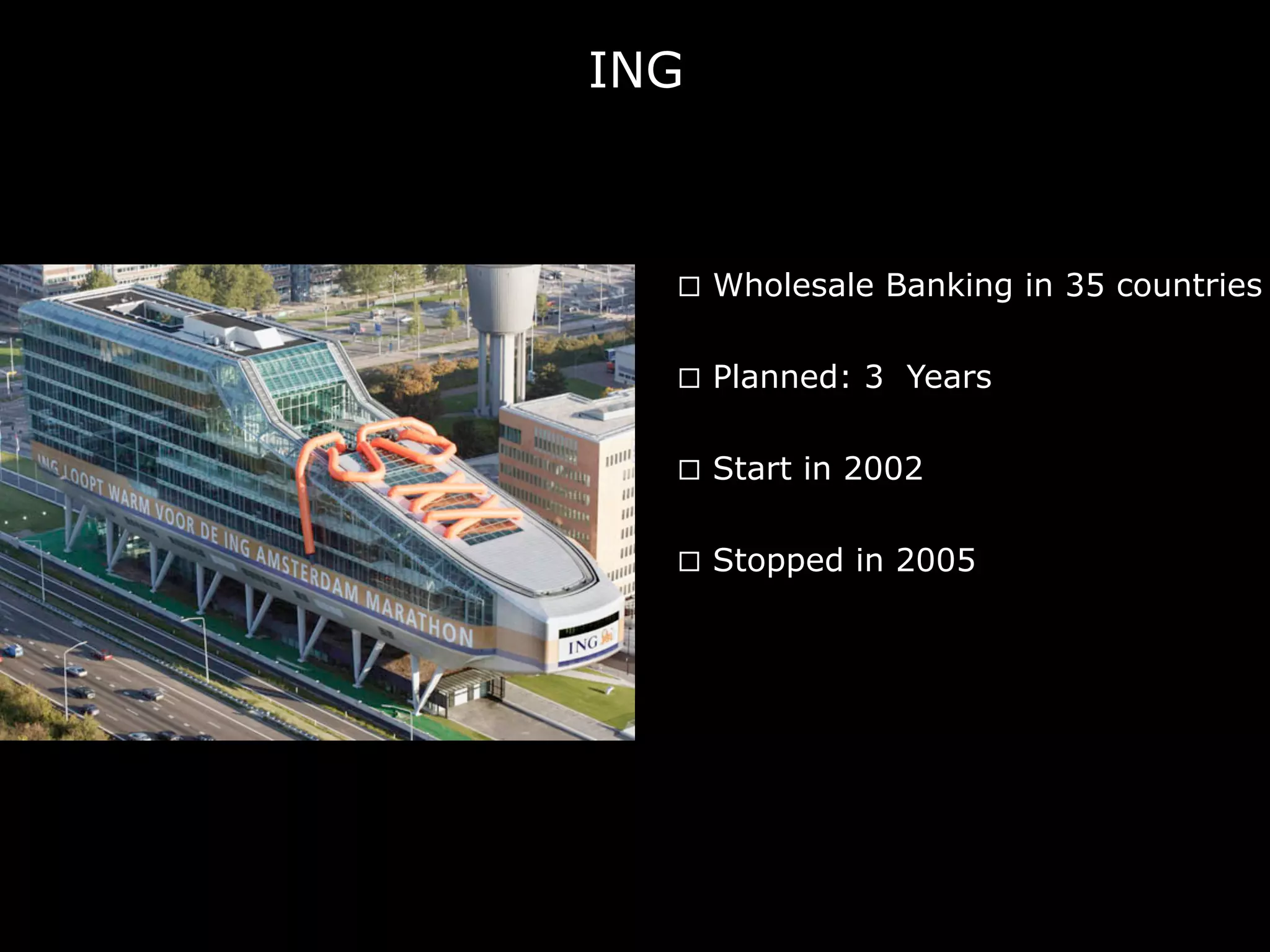

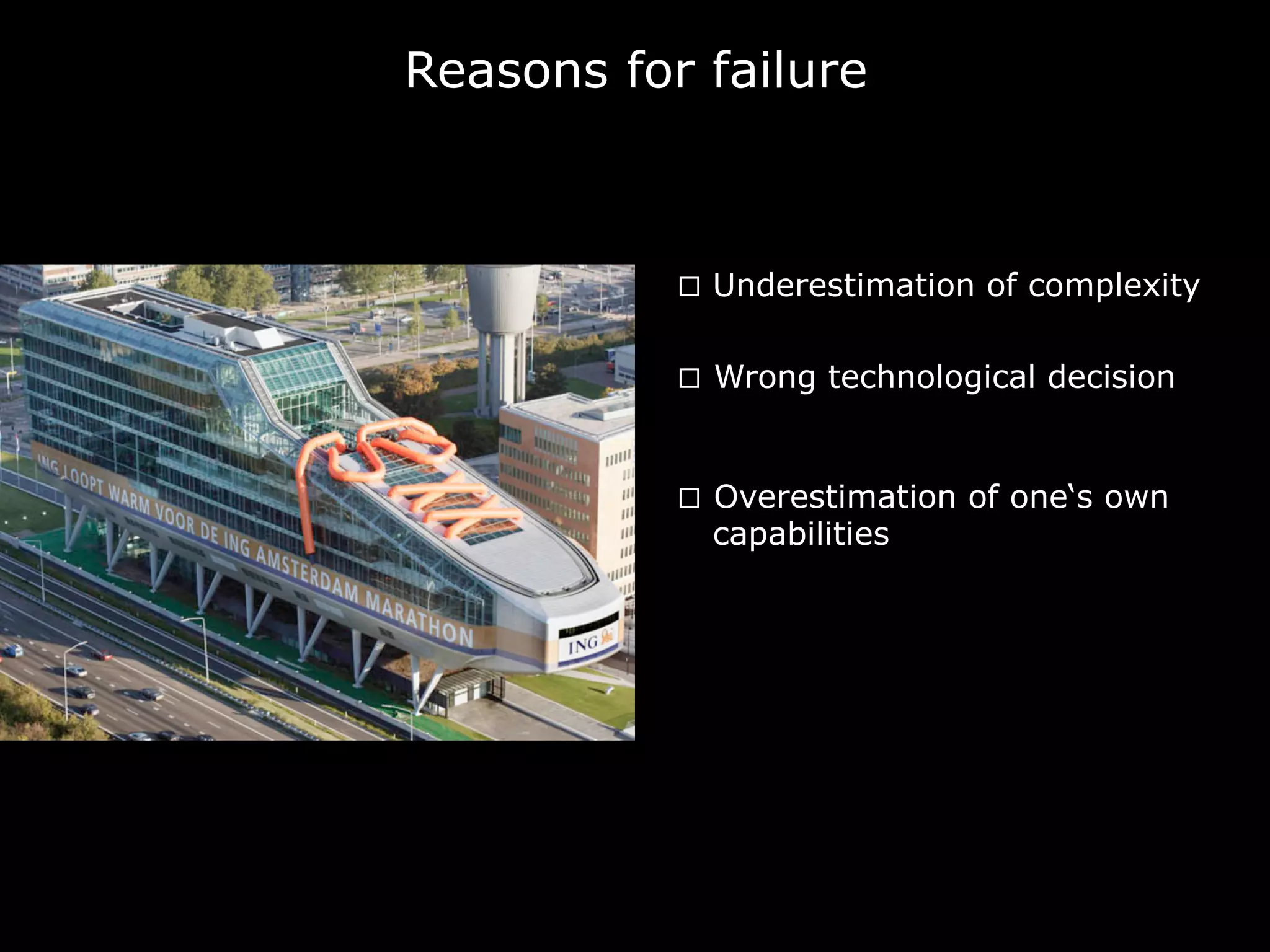

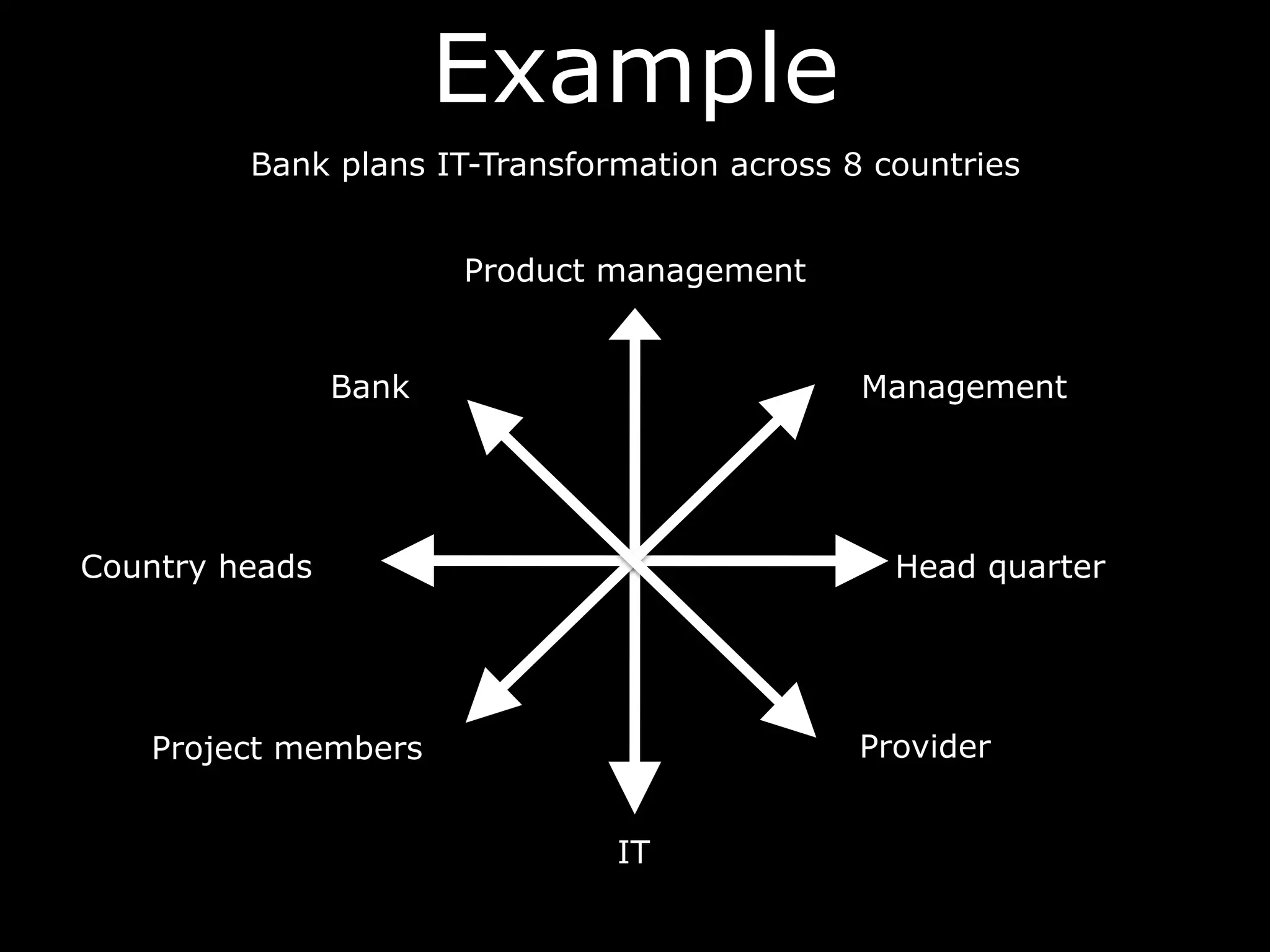

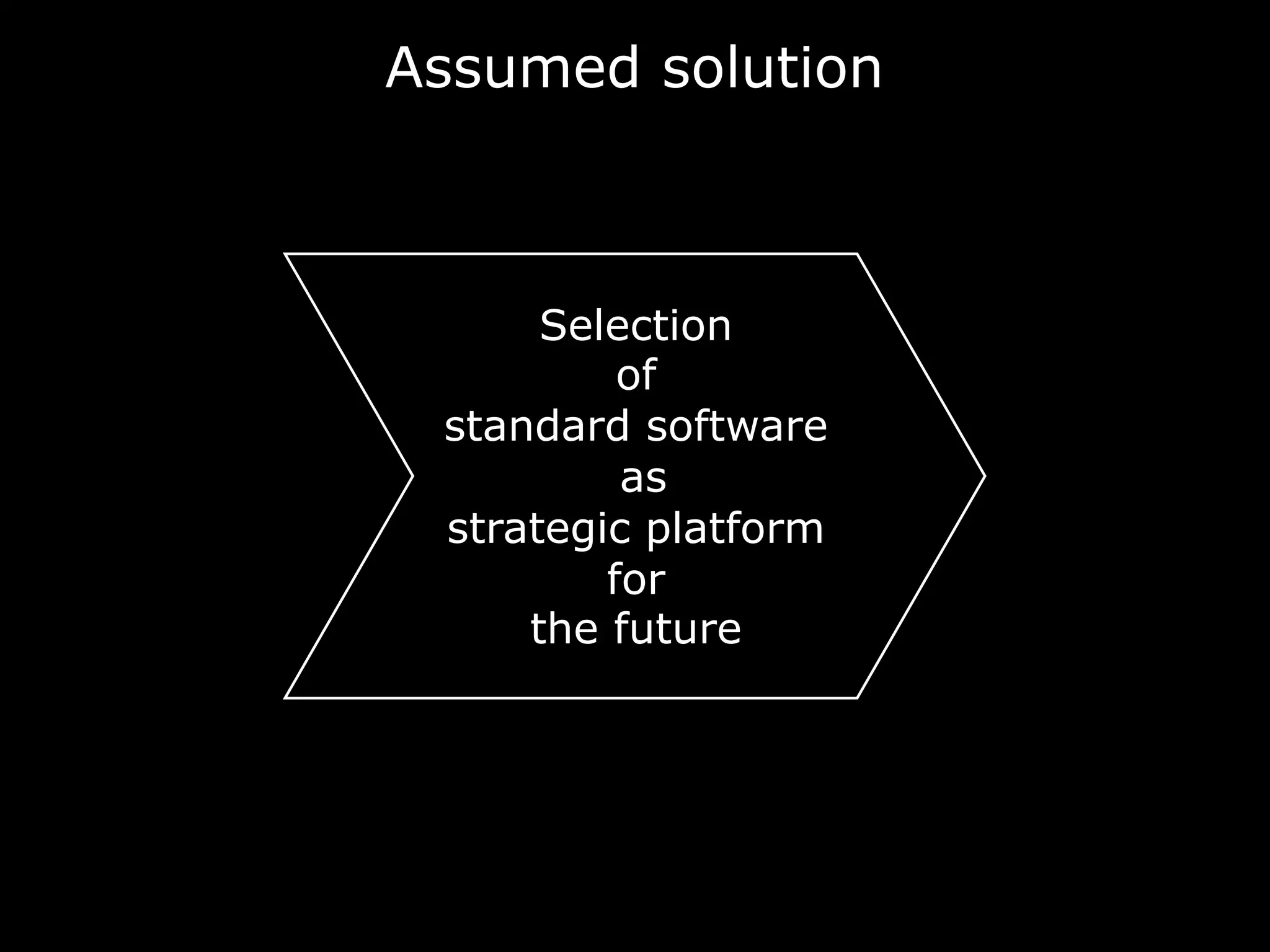

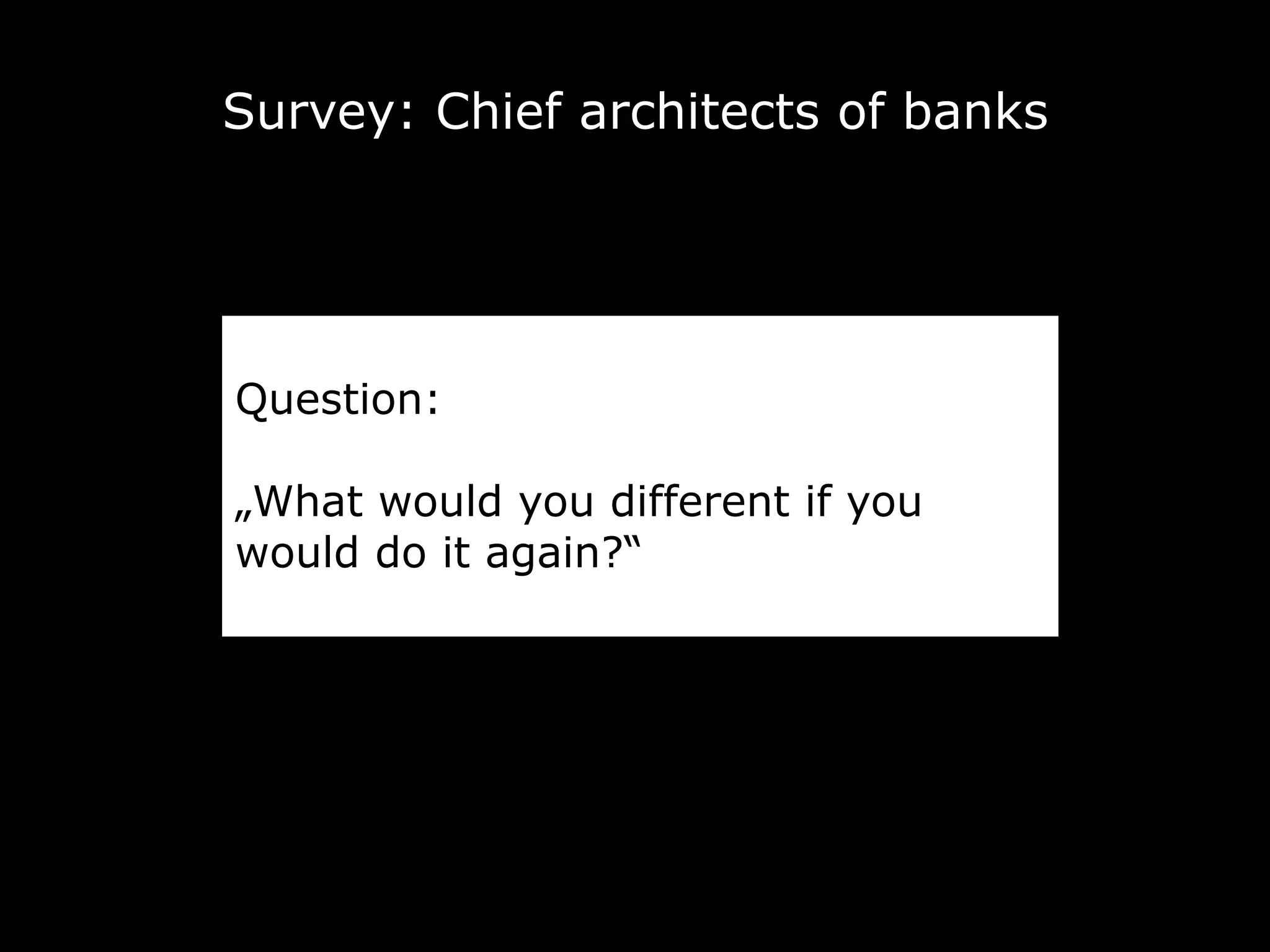

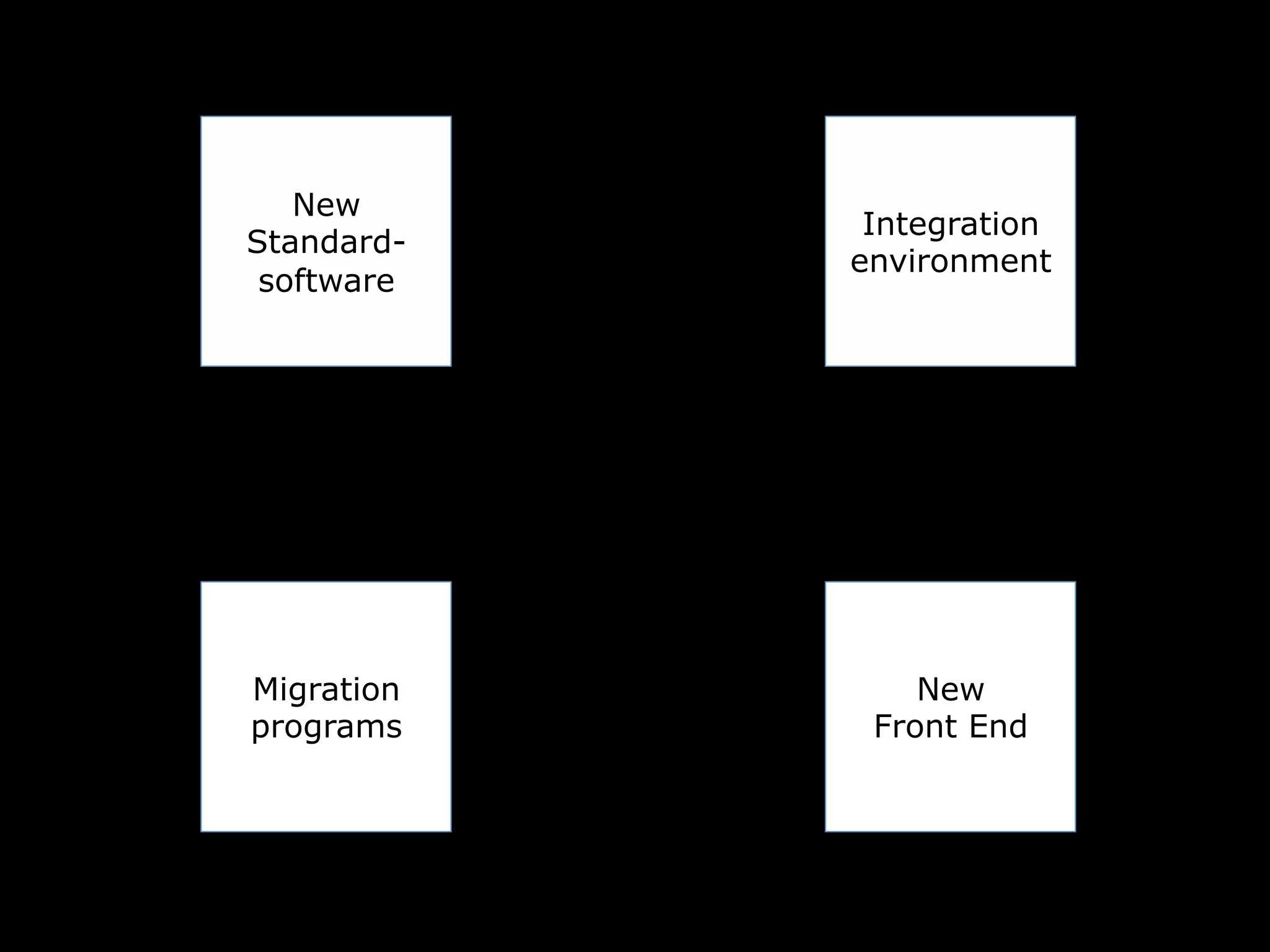

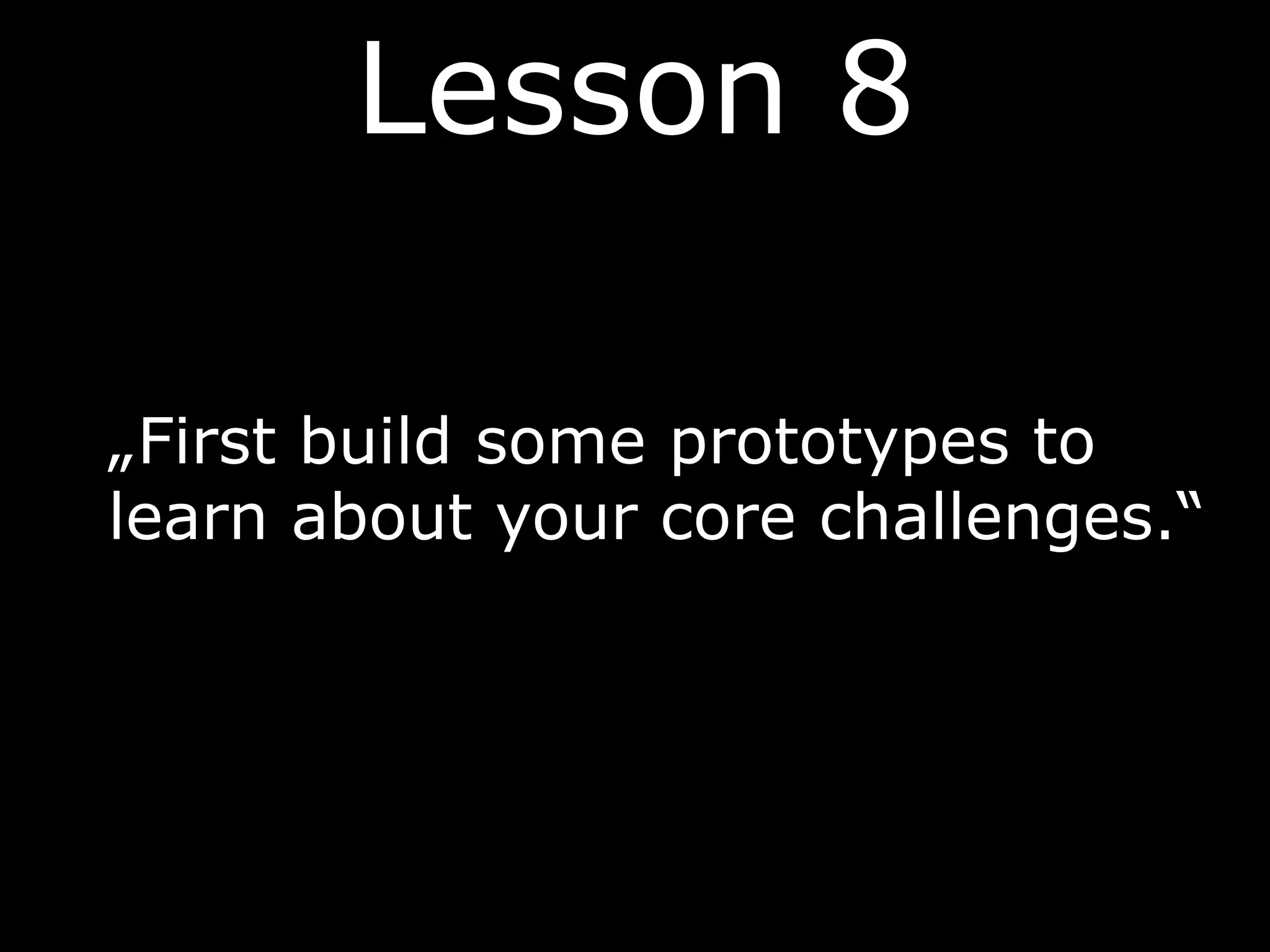

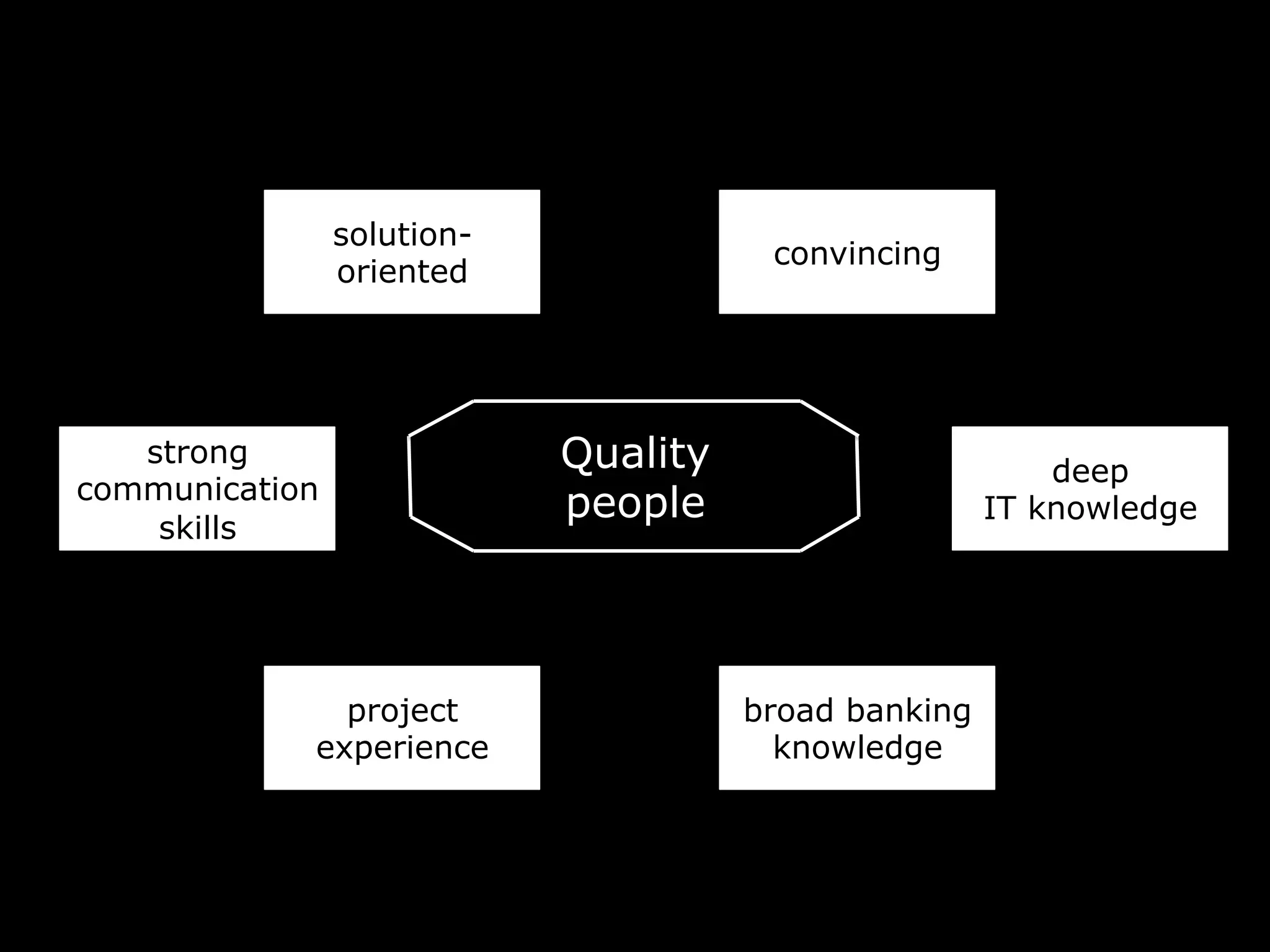

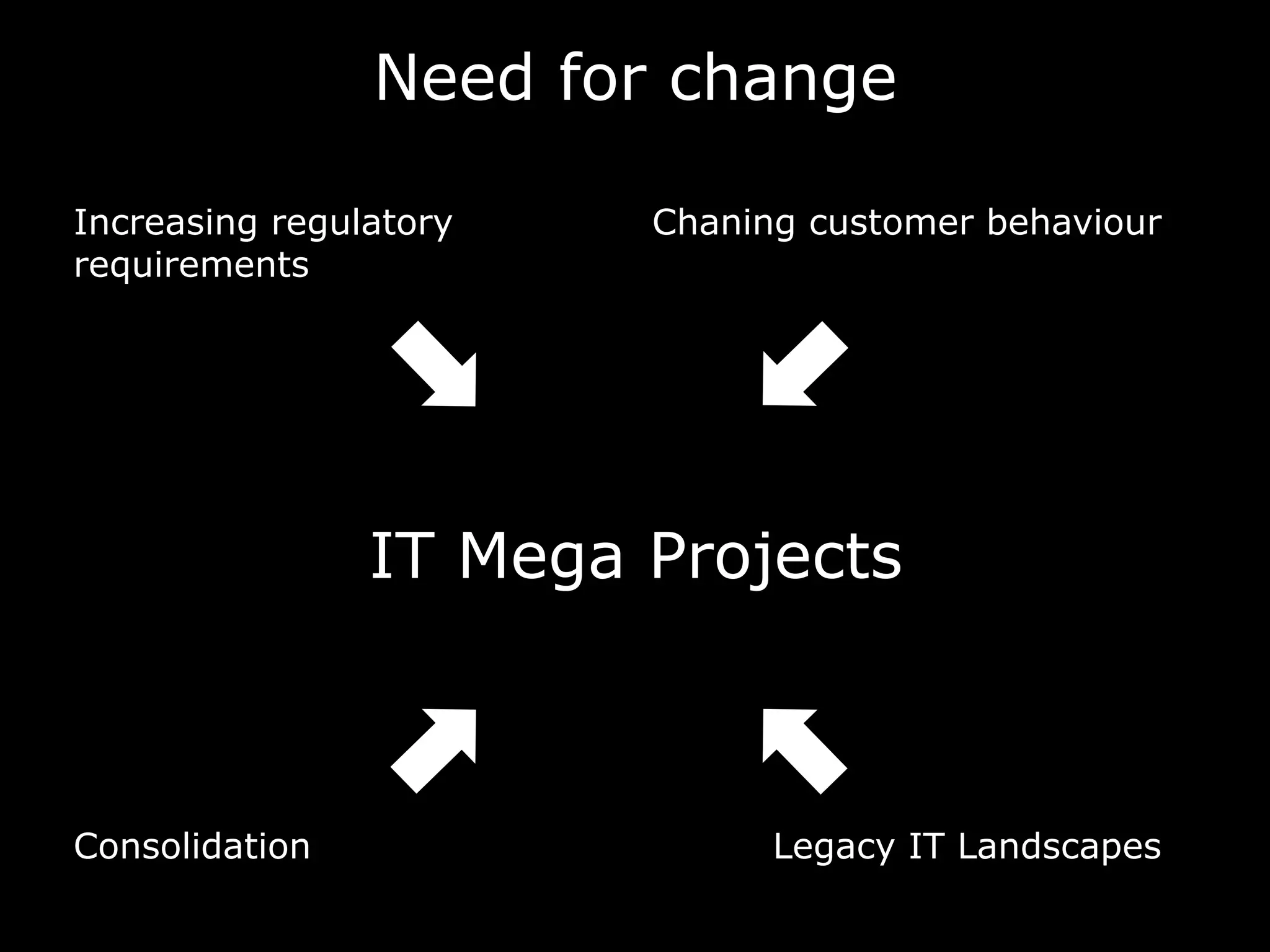

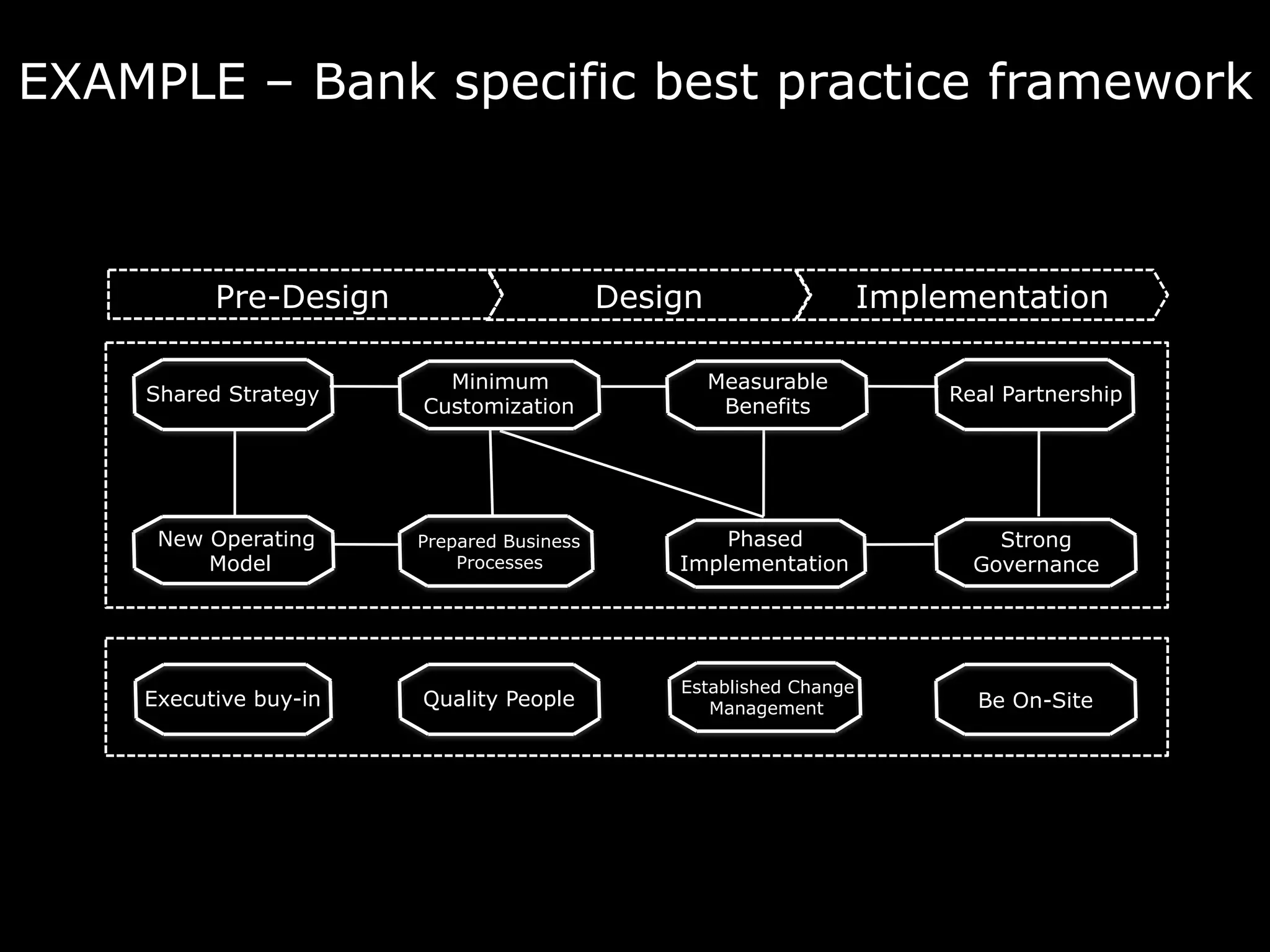

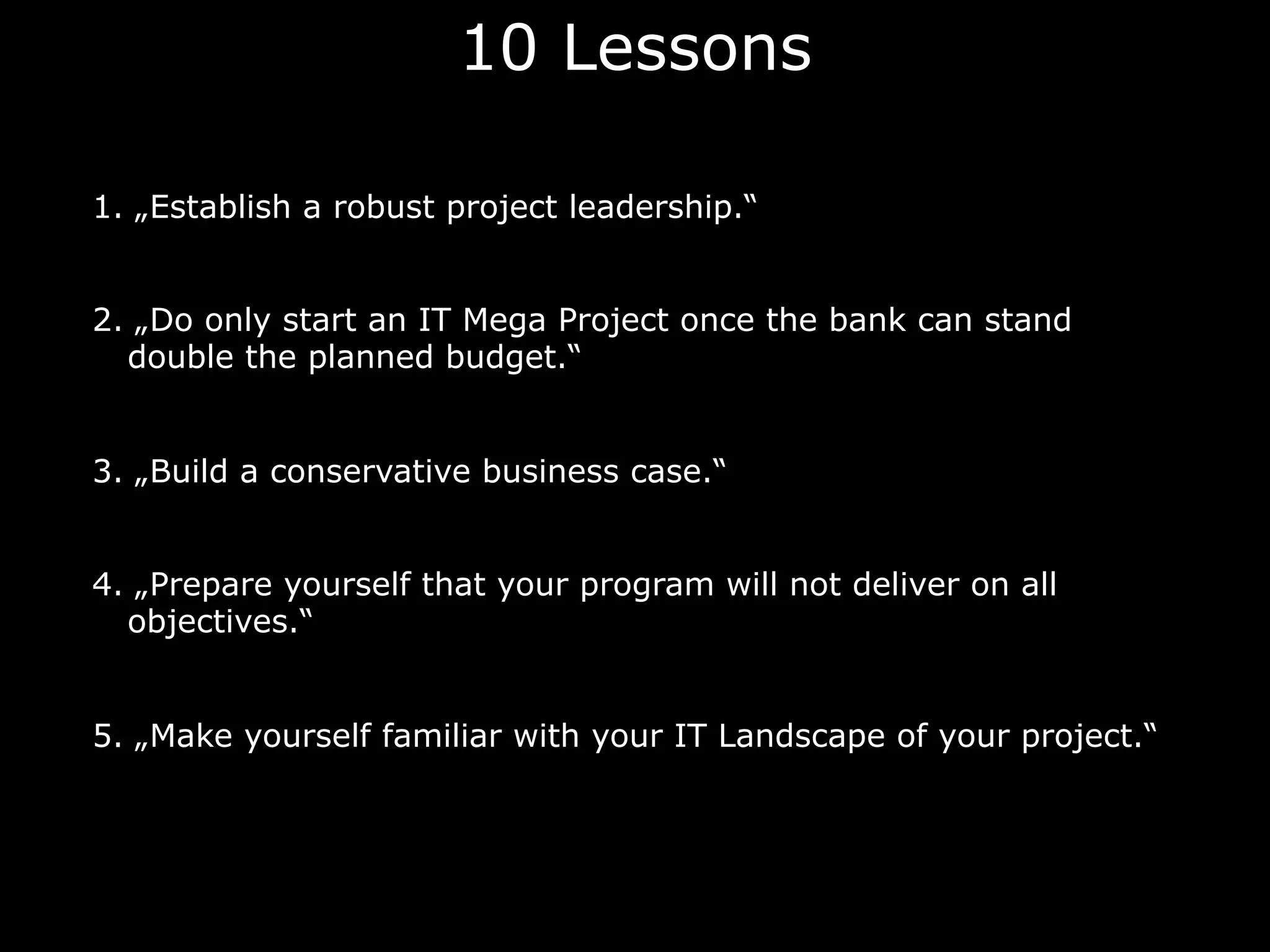

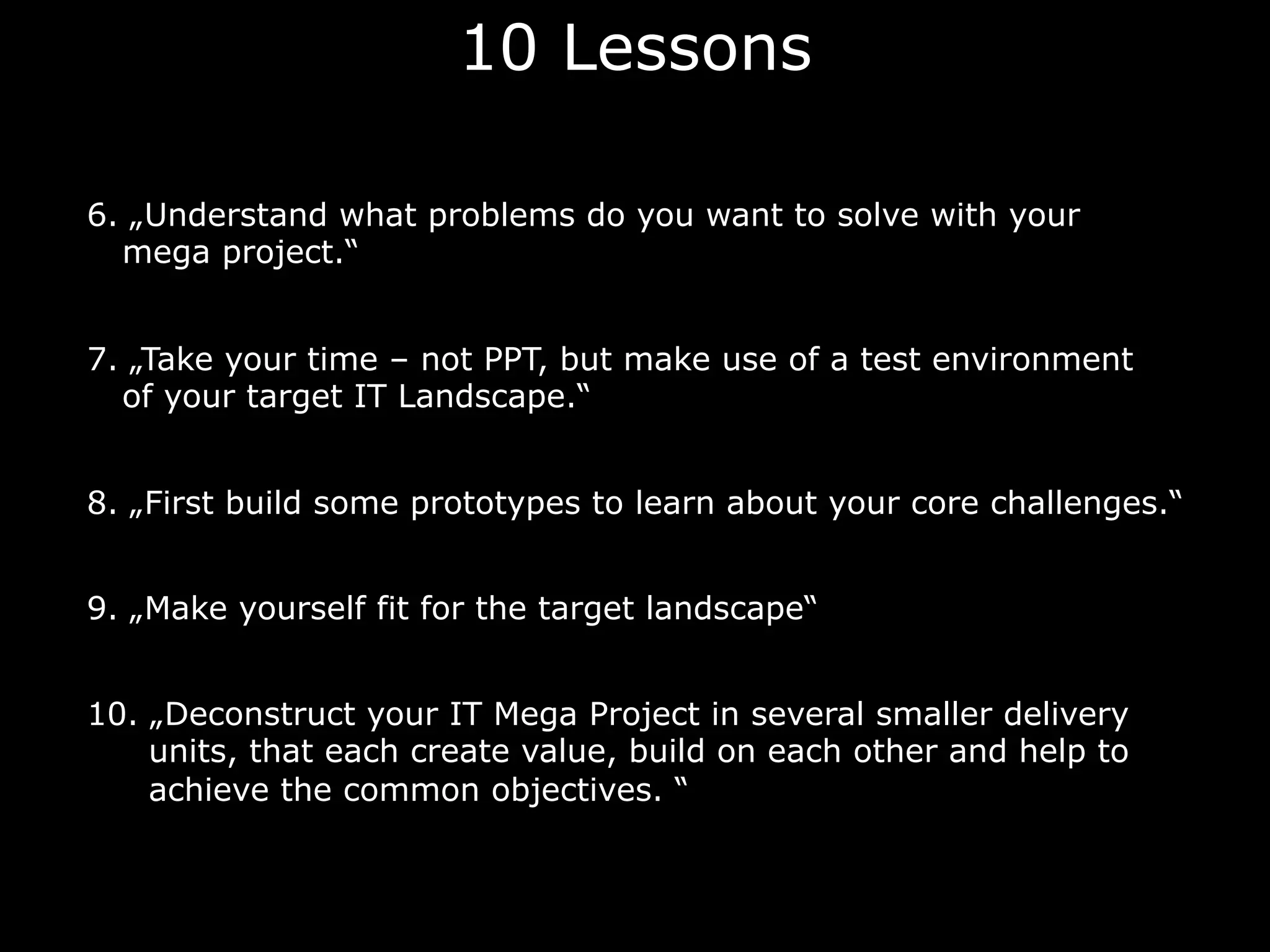

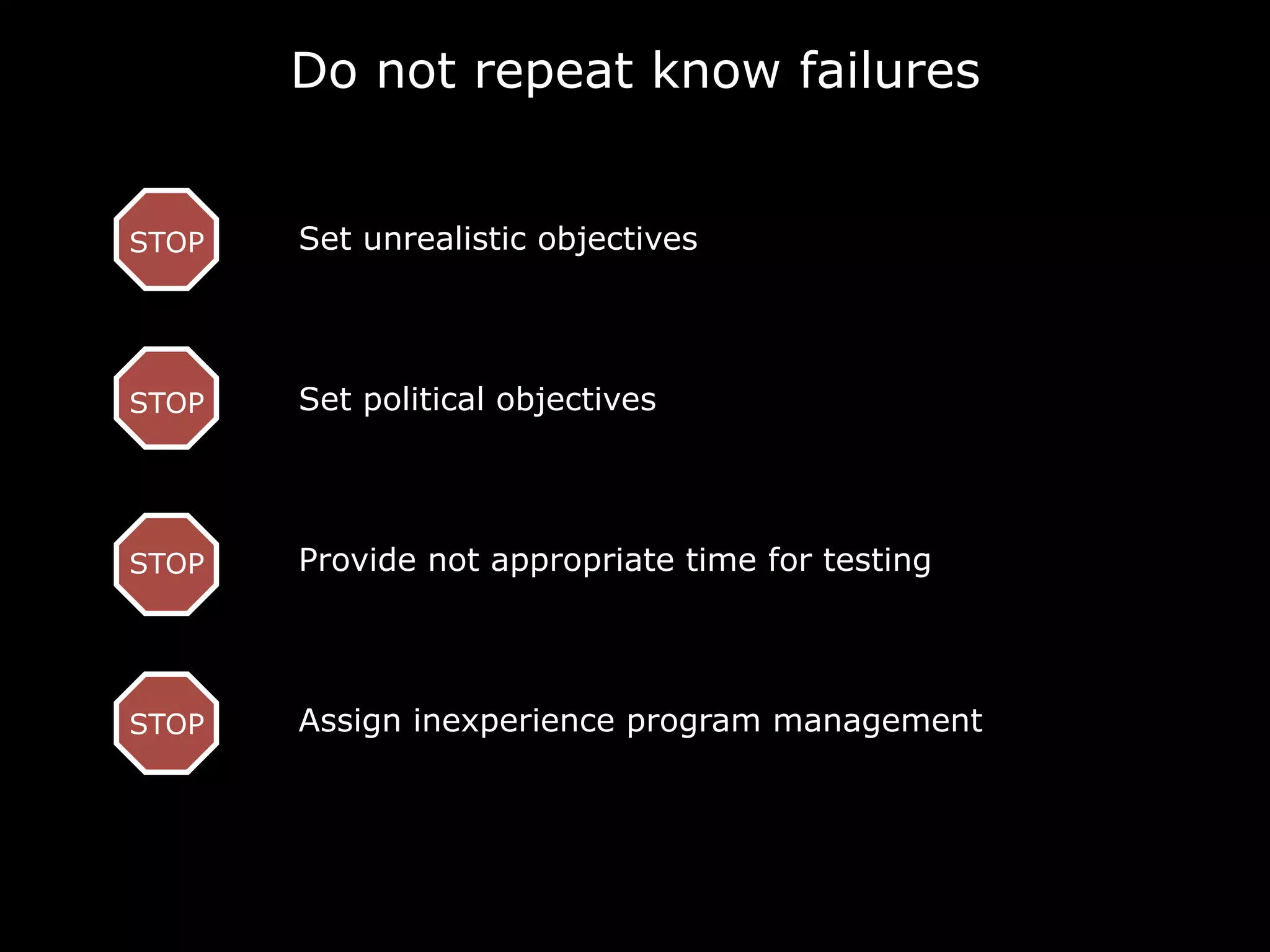

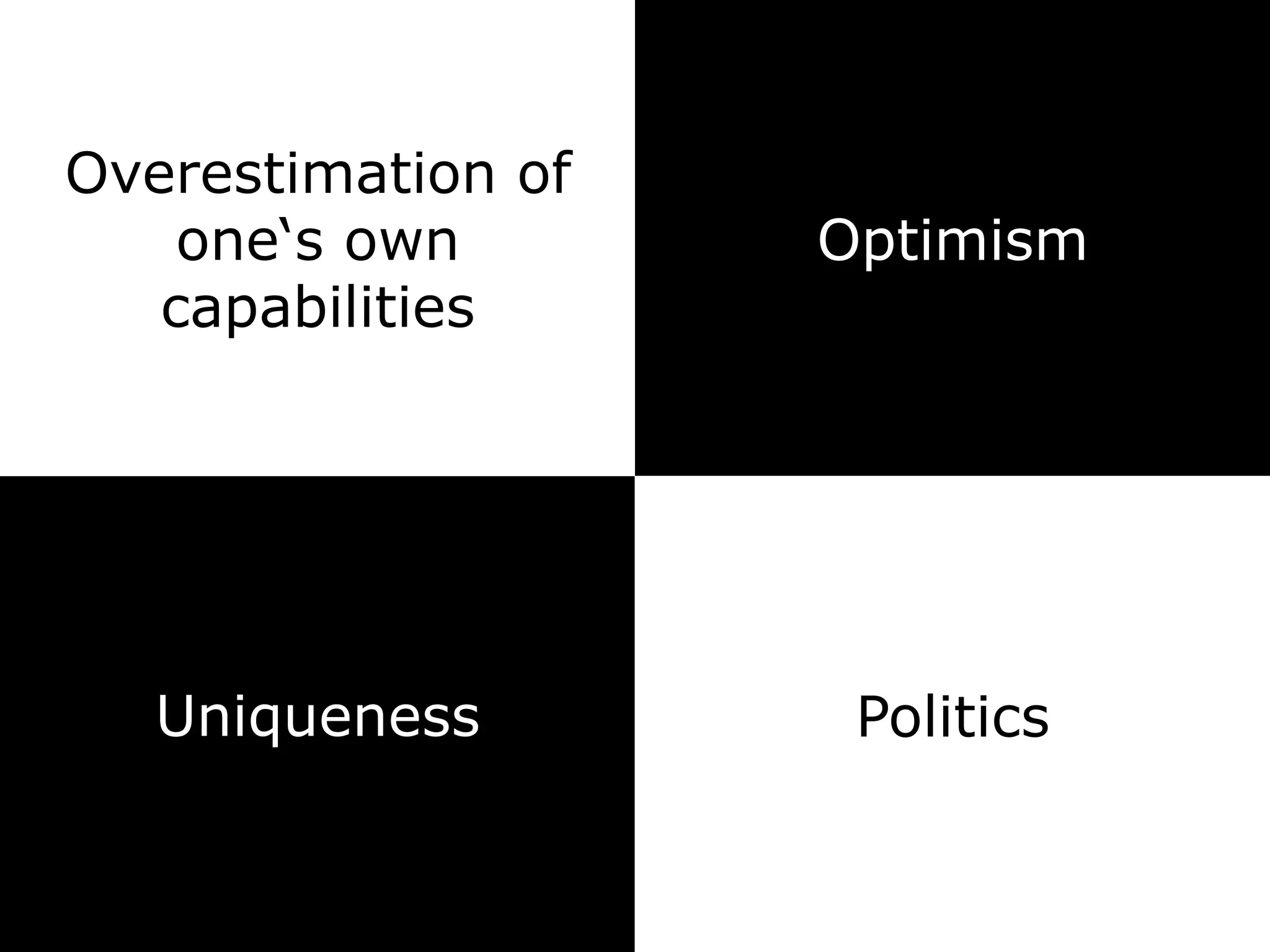

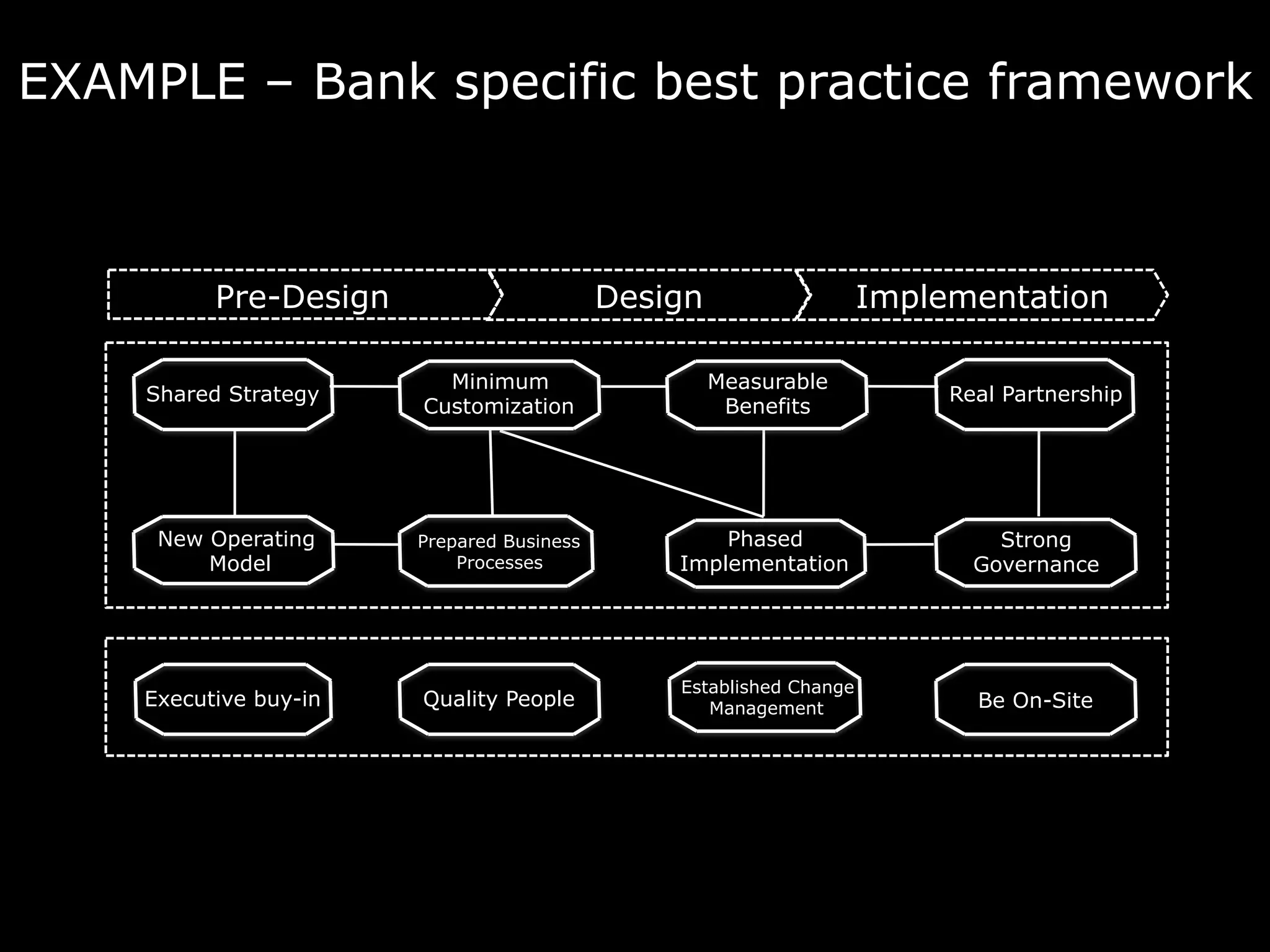

The document presents lessons learned from past IT mega projects in banking, emphasizing the common reasons for failure such as optimism, overestimating capabilities, and political pressures. It outlines ten critical lessons for success, including establishing robust project leadership, building conservative business cases, and understanding the IT landscape of the project. The content is based on case studies and expert insights to avoid repeating past mistakes and ensure better project outcomes.

![Breakthroughs In [It] Project Management Slideshare](https://cdn.slidesharecdn.com/ss_thumbnails/breakthroughsinitprojectmanagement-slideshare-100213212942-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)