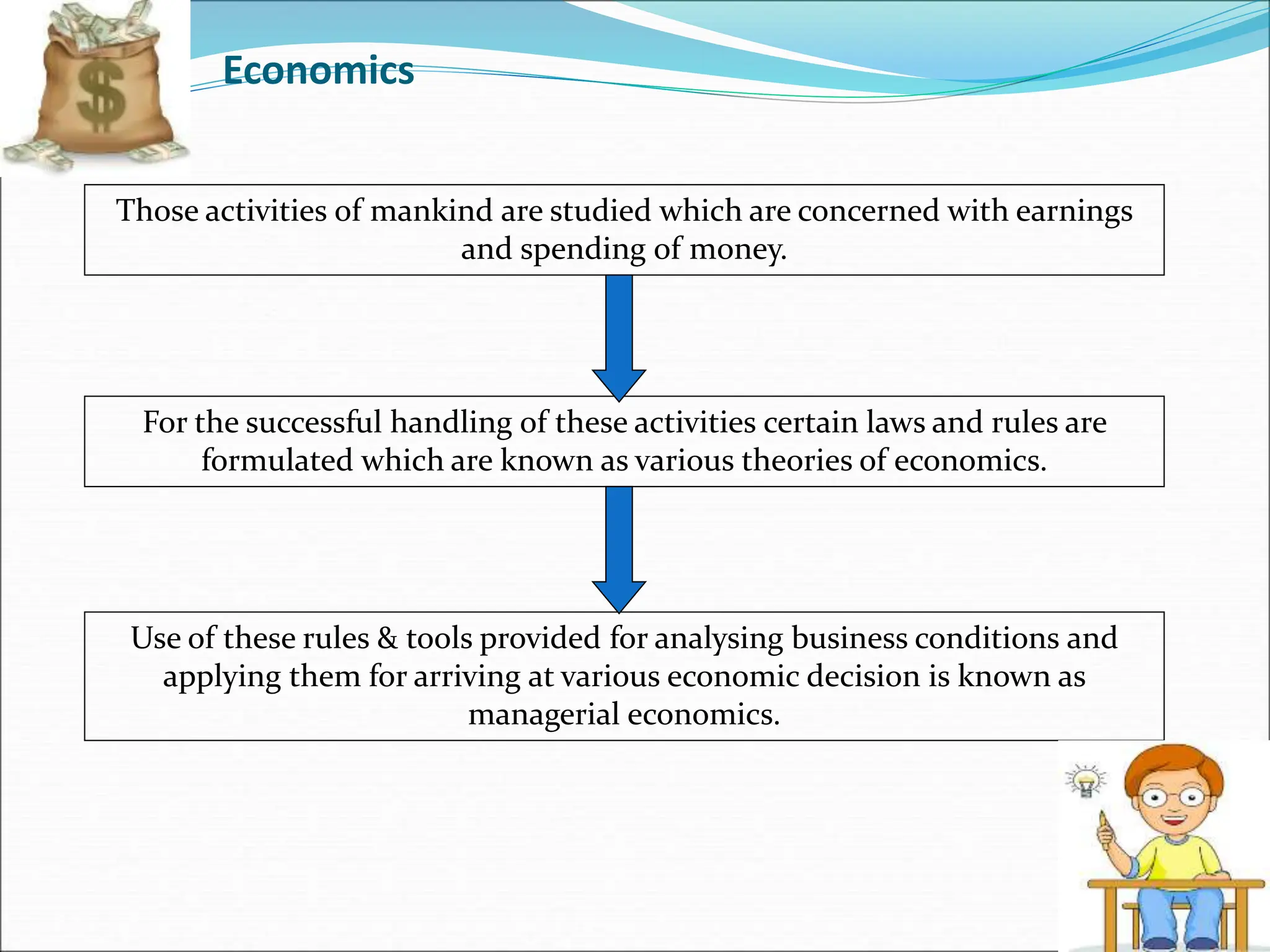

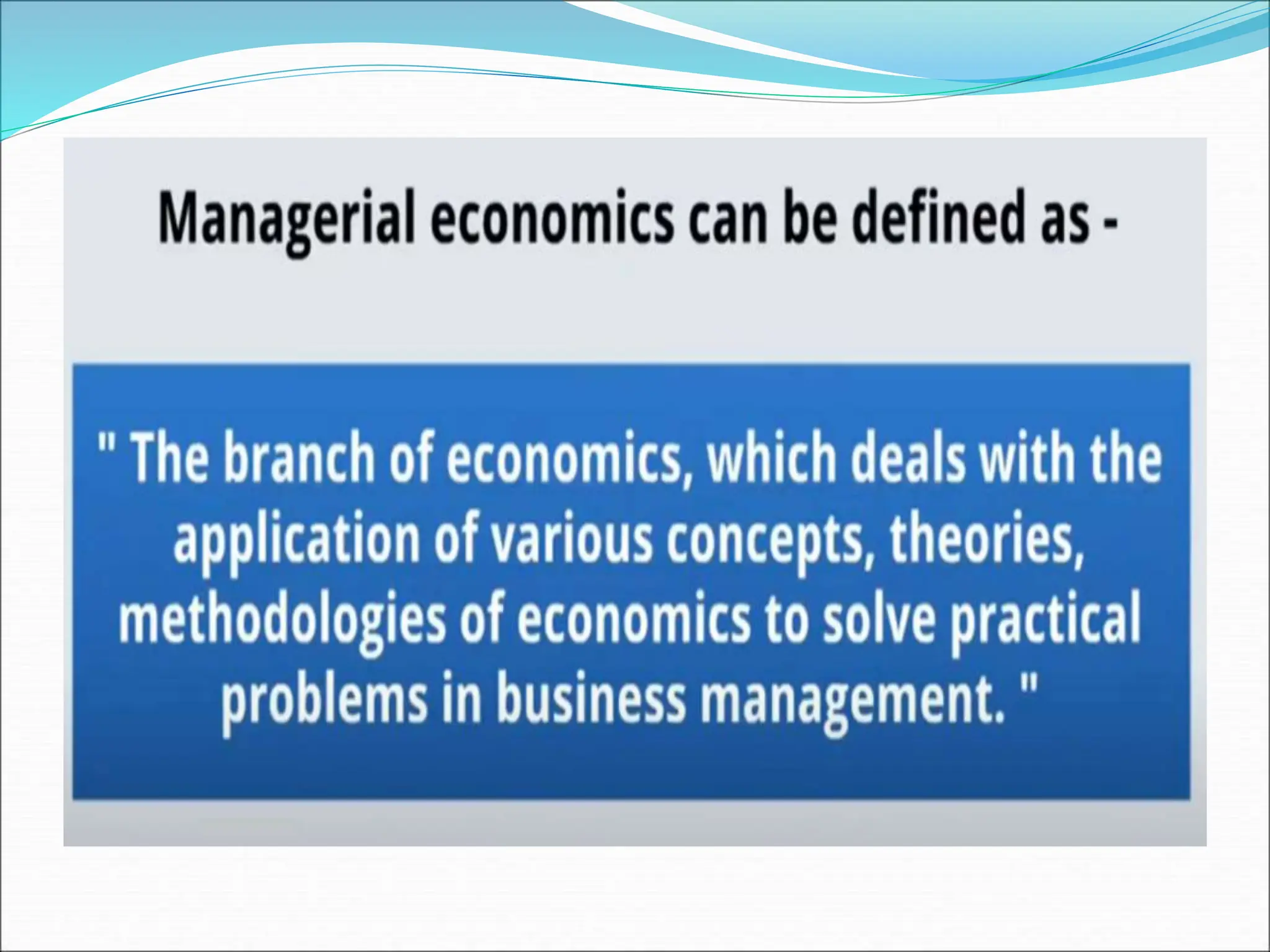

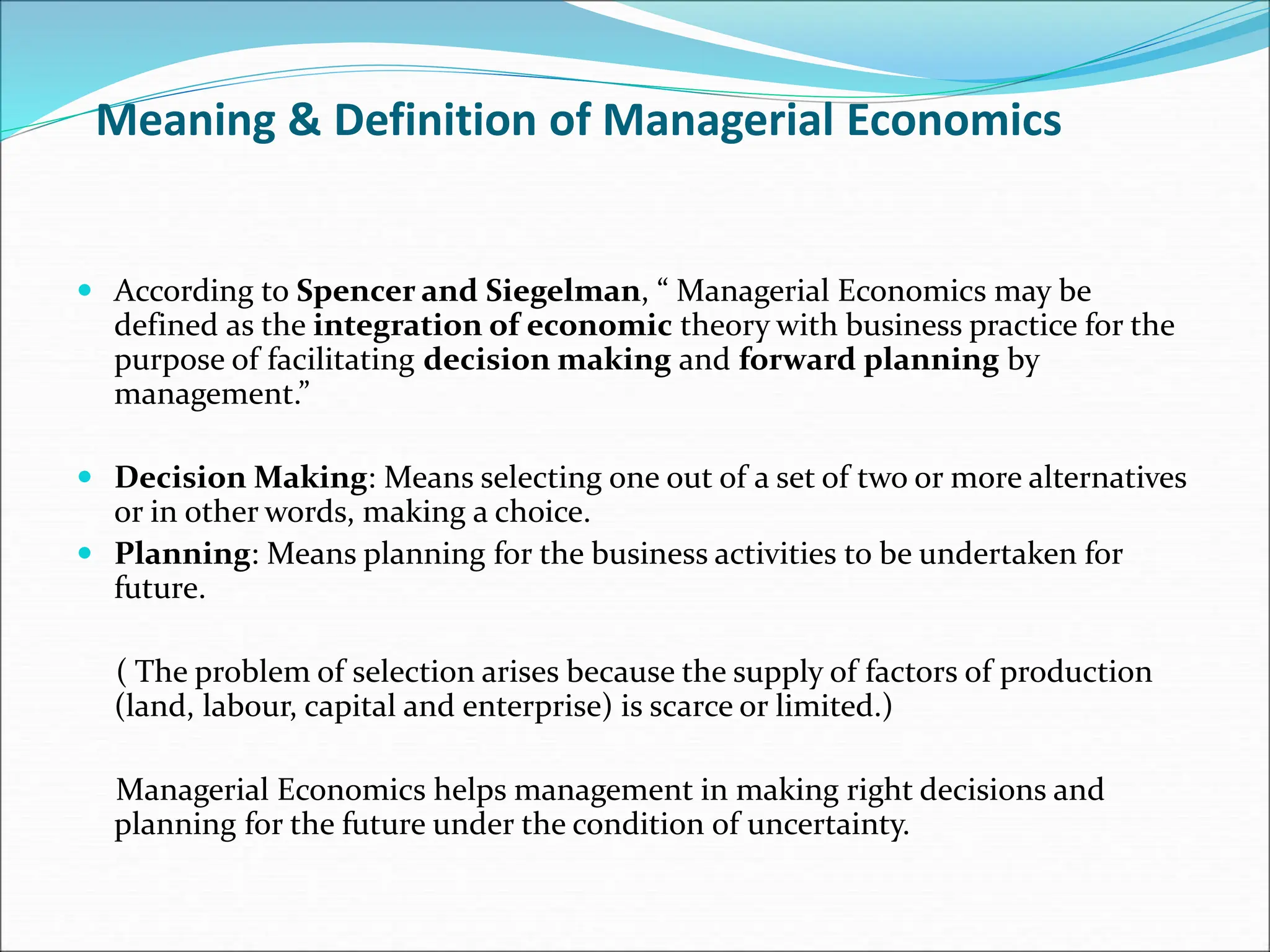

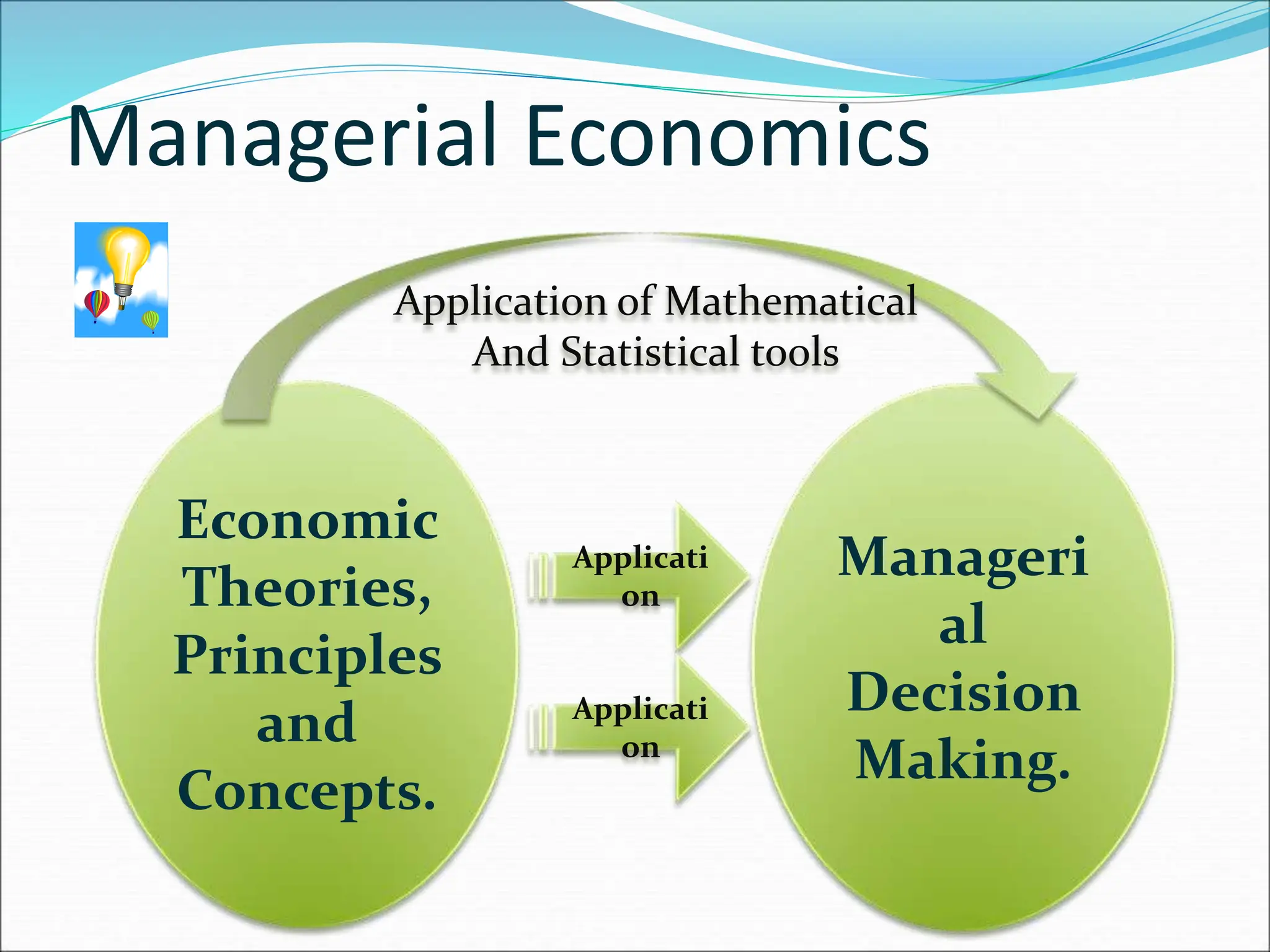

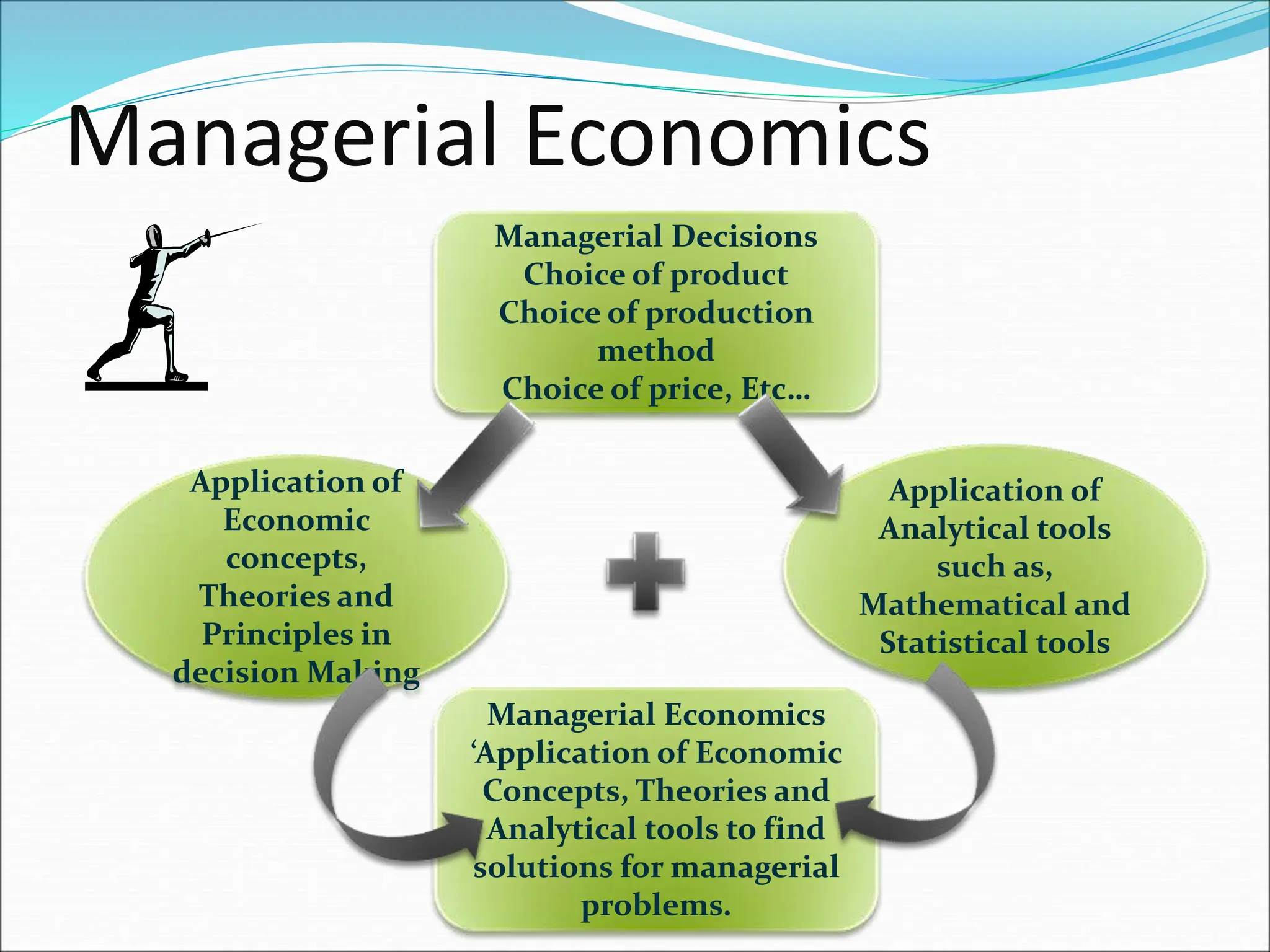

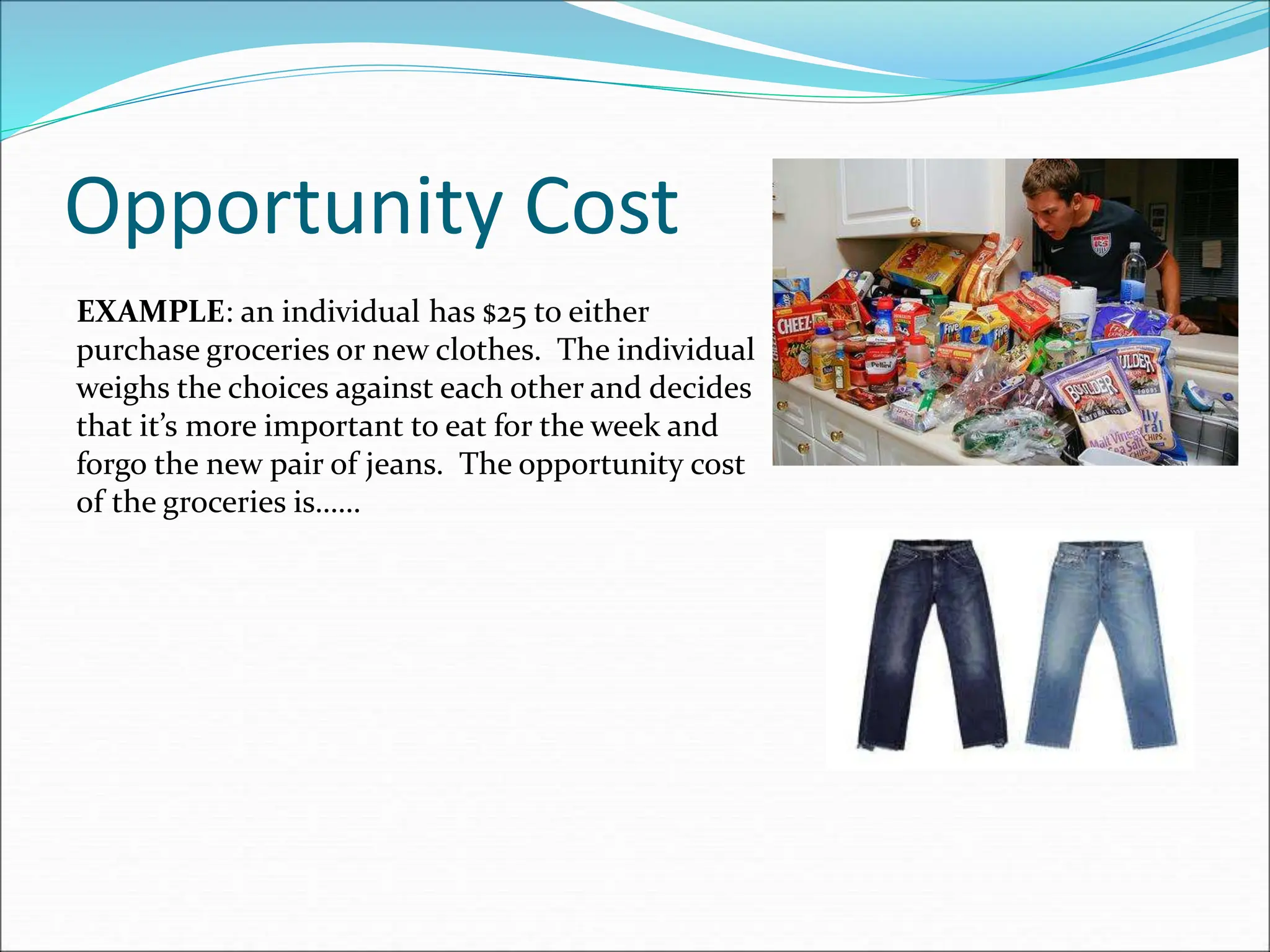

Managerial economics combines economic theory and business practice to facilitate decision-making and planning under uncertainty, helping managers choose optimal alternatives utilizing limited resources. It encompasses demand analysis, production planning, cost management, and pricing policies, alongside methodologies for analyzing business situations. Key principles include opportunity cost, equi-marginalism, and the importance of forecasting, ensuring effective management and profit maximization in business operations.