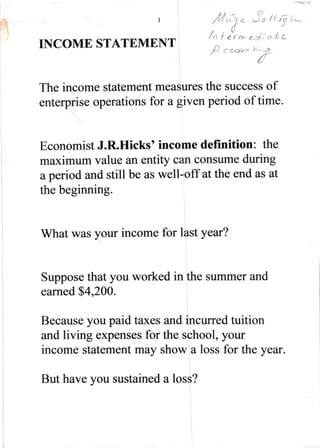

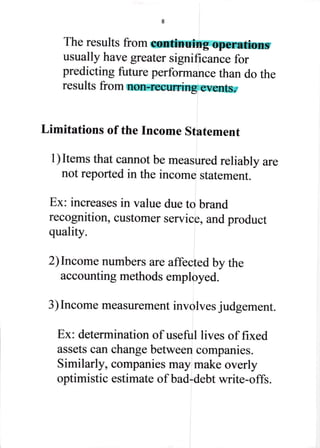

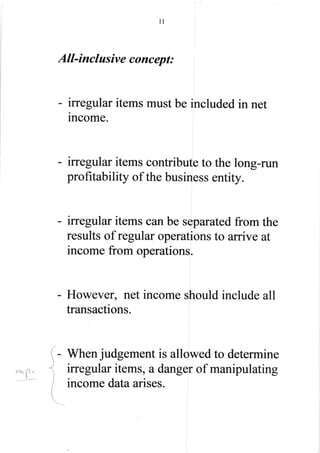

The income statement measures the success of a business over a period of time. It assesses revenues earned and expenses incurred. However, income totals can be affected by accounting methods used and involve judgement in some cases. Determining what is included in net income, such as irregular gains and losses, is an issue because it impacts the portrayal of a company's performance. There are debates around whether irregular items should impact net income or be directly reflected in retained earnings.

![The past decade has witnessed an exceptional

degree of attention on subtotals that make up

the income statement.

The opportunistic use of income statement to

alter earnings performance is also important.

Earnings management can be performed by

accelerating or decelerating the recognition of

revenue or gains and expenses or losses.

Earnings can be shifted among different

peri ods(interperiod version).

Different classification or disclosure of items

within the income statement of a single period

may also lead to earnings management.

66ni,^.fif ivt 1t""t 1

v]

Nt In|rcl..rlcJ

Fnr(k'9 "t"''t6'* ::*l^

l" 'L"Jl .-c; ik .'^r tr

t ''Tt' Pt''

6

./

Infczpcrr:C'

)tr,ft;a ea^;^?3

^.",8

uor*'u^r

(v'J+](https://image.slidesharecdn.com/intermediateii-150226100040-conversion-gate02/85/Intermediate-ii-5-320.jpg)

![Banking std8 nikunj.pptx [autosaved]](https://cdn.slidesharecdn.com/ss_thumbnails/bankingstd8nikunj-150501044045-conversion-gate01-thumbnail.jpg?width=640&height=640&fit=bounds)