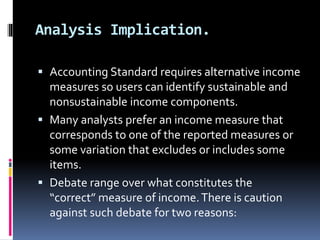

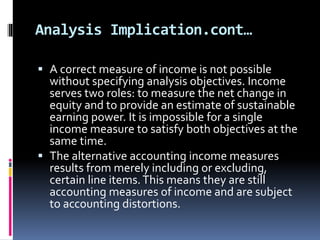

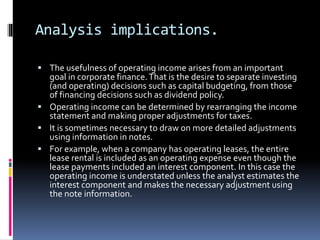

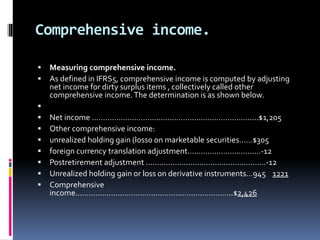

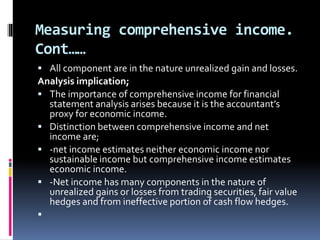

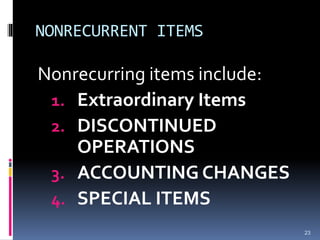

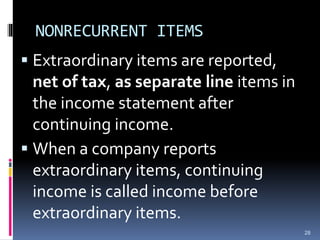

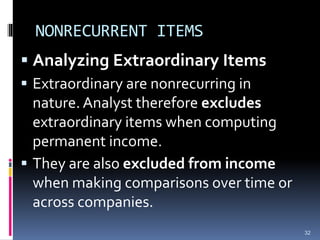

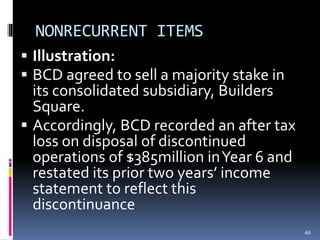

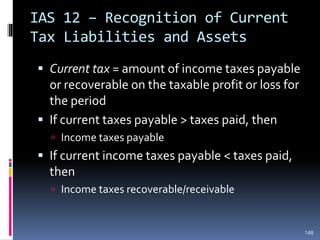

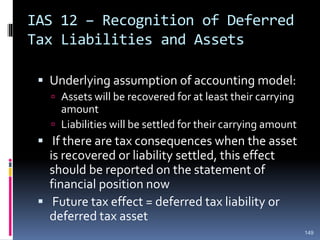

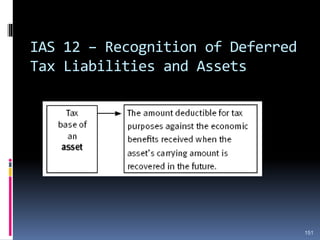

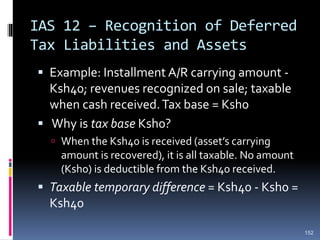

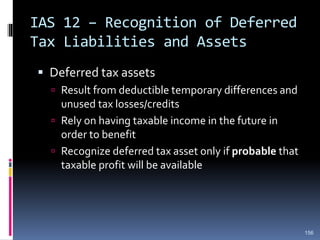

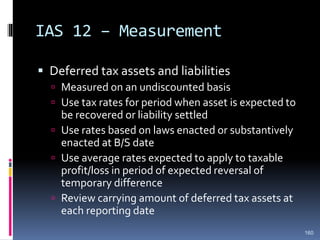

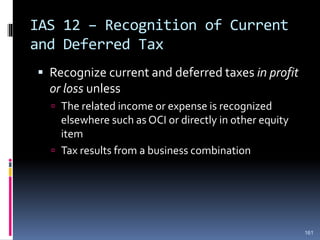

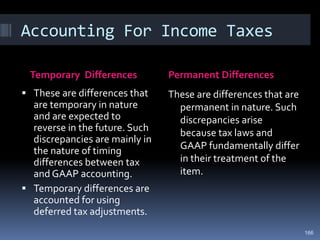

The document analyzes operating activities in corporate financial reporting, emphasizing the measurement of income and its implications for financial analysis. It discusses the classification of income into recurring and nonrecurring components, as well as various alternative income measures such as comprehensive income and net income. Additionally, it covers the treatment of extraordinary items, discontinued operations, and accounting changes, highlighting their significance in understanding sustainable earnings and financial performance.

![Alternative Measure of

Accounting Income : cont…

4. Core Income:

Is a measure that excludes all nonrecurring

items that are reported as separate line items on

the income statement. In the illustration, Core

income equals the continuing income reported in

2006 and 2004.Yet in 2005, Core income is

different-it excludes the after tax effect of the

restructuring charge of $1016m. In this case, core

income equals continuing income plus the

restructuring charge that is multiplied by one

minus the 35% marginal tax rate, or

$463{computed as $(197) plus the $1016×0.65]](https://image.slidesharecdn.com/group4analyzingoperatingactiviies-240520052756-d7f98a09/85/Group_4_ANALYZING_OPERATING_ACTIVIIES-ppt-13-320.jpg)