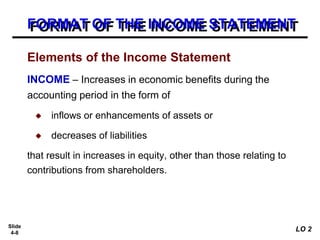

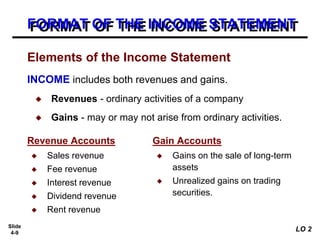

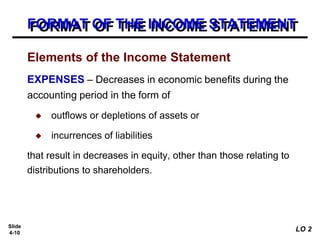

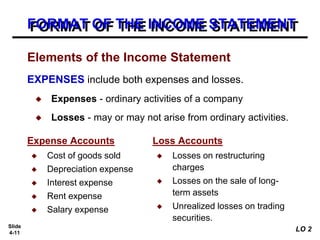

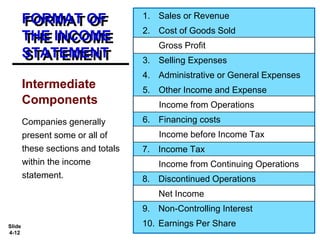

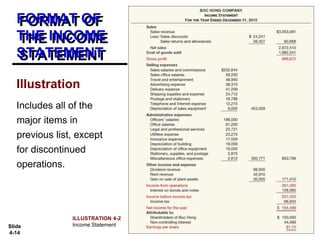

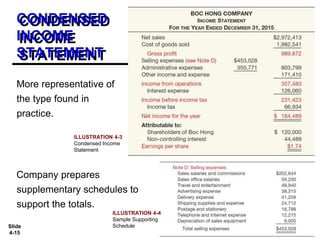

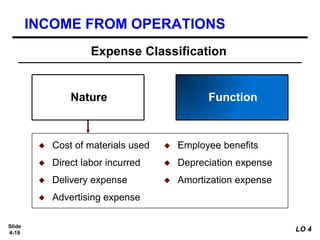

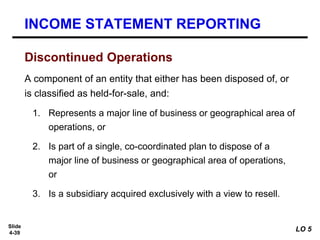

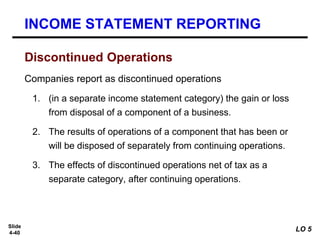

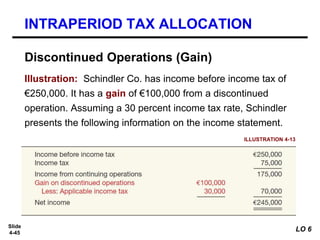

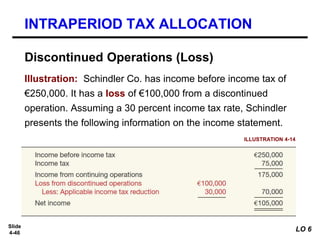

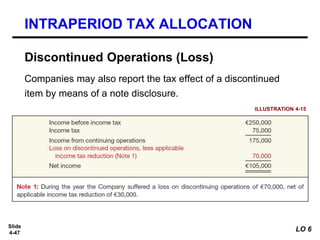

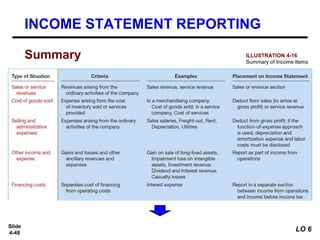

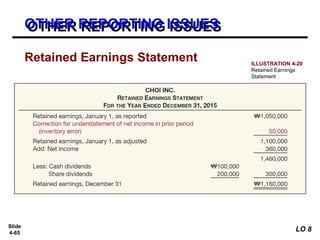

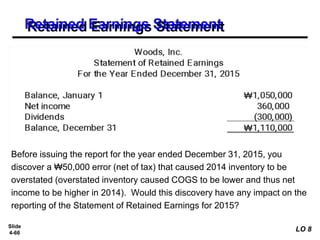

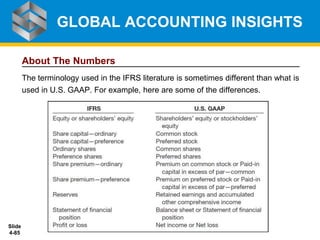

This document provides an overview of key concepts that will be covered in a chapter on income statements and related information. The learning objectives cover understanding the uses and limitations of income statements, their content and format, how to prepare them, and how to report various items. The chapter will explain the components of an income statement including revenues, expenses, gains and losses. It will also cover reporting earnings per share, discontinued operations, and other comprehensive income. Sample income statements and numerical examples are provided to illustrate the concepts.