Download to read offline

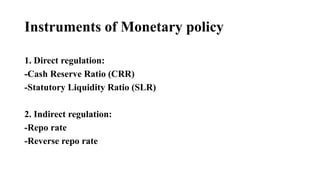

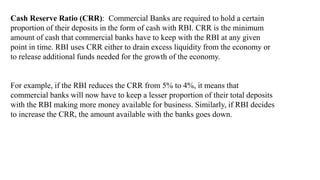

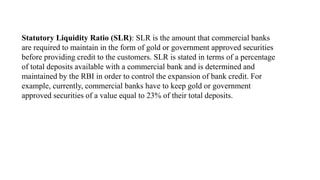

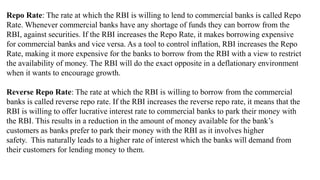

The Reserve Bank of India (RBI) uses various instruments of monetary policy to control the supply of money in the economy and maintain price stability. These include direct tools like the Cash Reserve Ratio (CRR) and Statutory Liquidity Ratio (SLR), which require banks to hold certain percentages of deposits as cash reserves and government securities. Indirect tools include the repo rate and reverse repo rate, which are the interest rates at which the RBI lends to and borrows from commercial banks. By adjusting these rates, the RBI can increase or decrease the availability of funds in the economy in order to manage inflation and economic growth.