The document provides information about input tax credit (ITC) under the Goods and Services Tax (GST) system in India. Some key points:

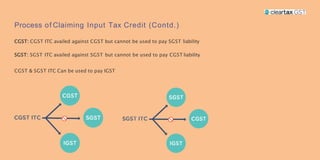

1. ITC allows businesses to offset taxes paid on inputs against output tax liability. It is claimed on goods, capital goods, and services used for business purposes.

2. There are conditions for claiming ITC, such as possessing valid documents and ensuring taxes are paid. ITC must also be adjusted if related outputs are exempt.

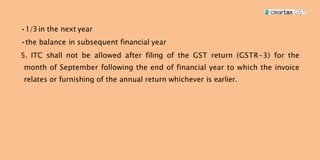

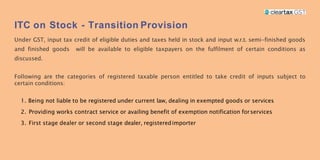

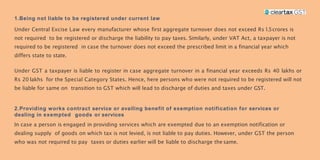

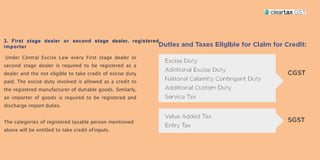

3. Not all purchases are eligible for ITC, such as most motor vehicles, food/beverages, health services, and property construction. Transition provisions allow ITC for stock under certain conditions.