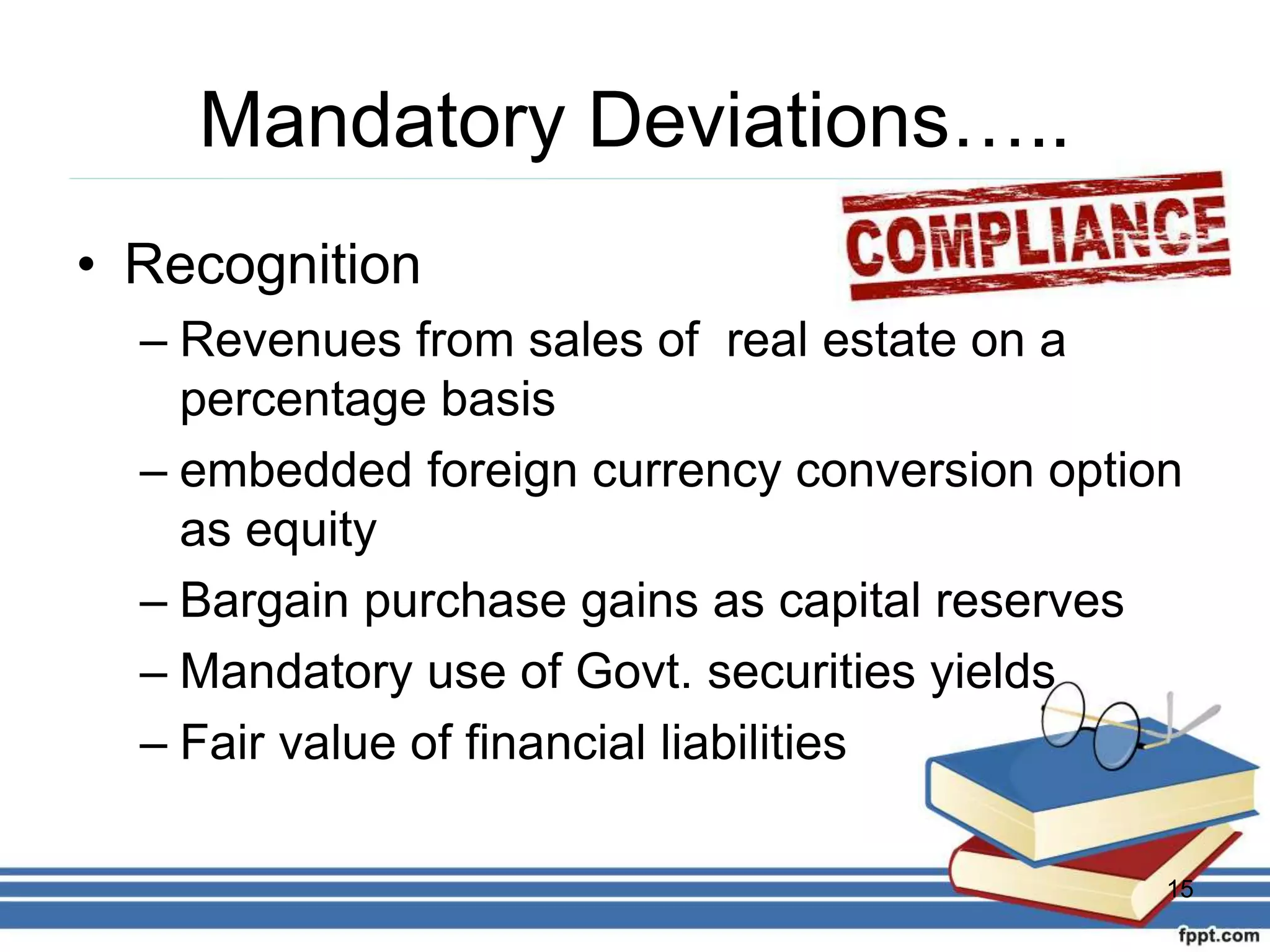

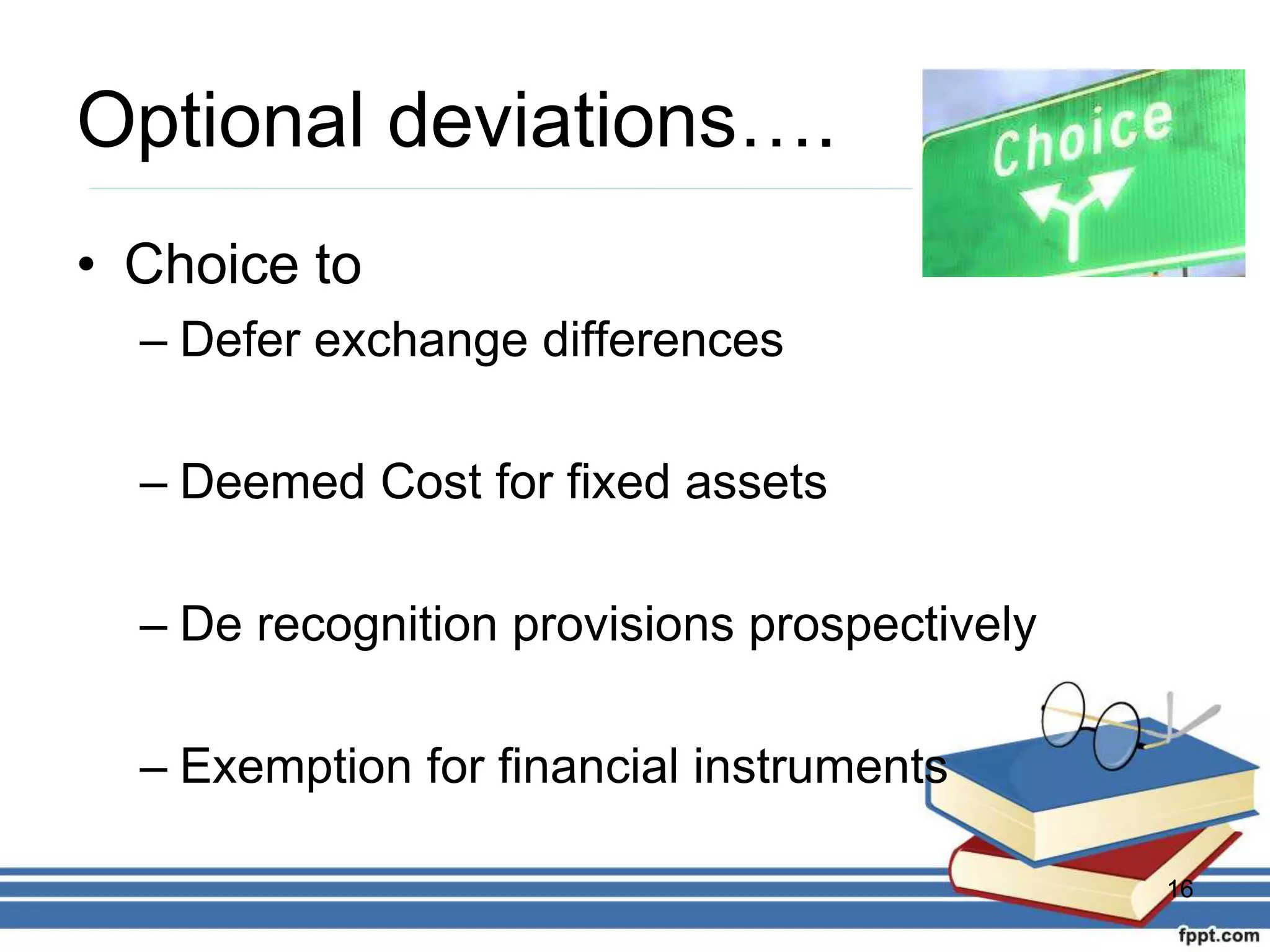

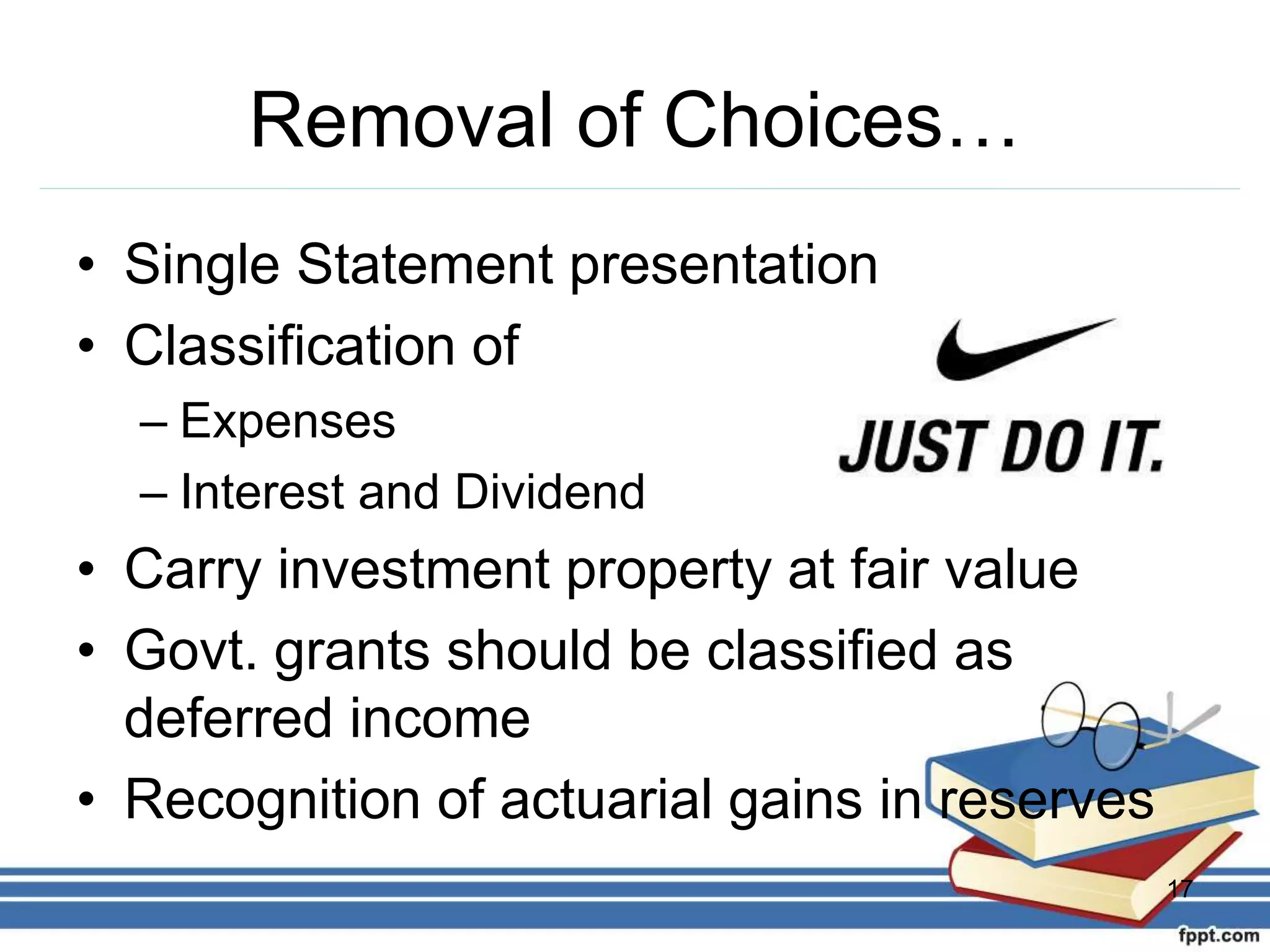

This document discusses India's convergence with International Financial Reporting Standards (IFRS). It provides definitions of IFRS and outlines reasons for its adoption, including the demand for global accounting standards. It describes India's specified approach, including the 35 applicable IFRS standards and implementation timeline. It also summarizes the roadmap set by the Institute of Chartered Accountants of India, including allowing two sets of standards, and specifies companies required to adopt IFRS. The document outlines benefits of global compatibility and major changes between IFRS and existing standards, as well as challenges to implementation.