WHAT ARE IAS?

Setof guidelines for preparing financial statements

Importance :

1)Consistency: Standardize financial reporting across

countries.

2)Transparency: Provide clear and understandable financial

statements.

3)Comparability: Facilitate comparison of financial

information globally.

4)Credibility: Enhance reliability and trust in financial data.

5)Decision-Making: Support informed decisions by

stakeholders.

6)Global Trade: Promote international trade and investment.

3.

IAS 1-PRESENTATION OFFINANCIAL

STATEMENTS

The main objective of IAS 1 is to ensure that financial statements provide comparable,

understandable, relevant, and reliable information to users.

Scope of IAS 1:

IAS 1 applies to all general-purpose financial statements prepared in accordance with

IFRS Standards.

Key Principles of IAS 1:

1)Complete Set of Financial Statements which includes:

• Statement of Financial Position (Balance Sheet)

• Statement of Profit or Loss and Other Comprehensive Income (OCI)

• Statement of Changes in Equity

• Statement of Cash Flows

• Notes to the Financial Statements, including accounting policies

4.

KEY PRINCIPLES OFIAS 1

2)Fair Presentation

The financial statements must fairly present

the financial position, performance, and

cash flows of the entity.

3)Going Concern

The financial statements are prepared in

every period.

5.

IAS 2-INVENTORIES

IAS 2is the International Accounting Standard that deals with the accounting treatment for

inventories. It sets out the guidelines for recognition, measurement, and disclosure of inventories in

financial statements. IAS 2 ensures that inventories are reported at a realistic value on the balance

sheet and that expenses related to inventory are recognized properly in the income statement.

Objective of IAS 2

To prescribe how inventories should be measured and how to recognize them as an expense when they

are sold. The standard also provides guidance on writing down inventories to their net realizable

value (NRV).

Scope of IAS 2

IAS 2 applies to all inventories, except:

Work in progress related to construction contracts (covered under IFRS 15 or IAS 11, if still

relevant in certain cases).

Financial instruments.

Biological assets (covered under IAS 41).

6.

IAS 2-INVENTORIES

Definition ofInventories.Inventories include:

• Assets held for sale in the ordinary course of business.

• Assets in the production process for such sale (work in progress).

• Materials and supplies to be consumed in production.

7.

IAS 2-MEASUREMENT OFINVENTORIES

1)Cost of Inventories

Inventory cost includes:

• Purchase costs (purchase price, import duties, transport).

• Conversion costs (direct labor, direct materials, and overhead allocation).

• Other costs necessary to bring inventory to its present condition and location.

2)Exclusions from Inventory Cost

The following are not included in inventory cost:

• Abnormal waste.

• Storage costs (unless part of the production process).

• Administrative overheads unrelated to production.

• Selling and distribution costs.

8.

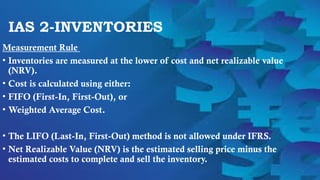

IAS 2-INVENTORIES

Measurement Rule

•Inventories are measured at the lower of cost and net realizable value

(NRV).

• Cost is calculated using either:

• FIFO (First-In, First-Out), or

• Weighted Average Cost.

• The LIFO (Last-In, First-Out) method is not allowed under IFRS.

• Net Realizable Value (NRV) is the estimated selling price minus the

estimated costs to complete and sell the inventory.

9.

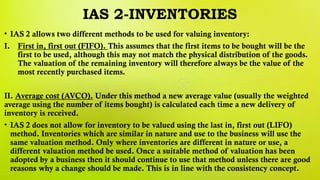

IAS 2-INVENTORIES

• IAS2 allows two different methods to be used for valuing inventory:

I. First in, first out (FIFO). This assumes that the first items to be bought will be the

first to be used, although this may not match the physical distribution of the goods.

The valuation of the remaining inventory will therefore always be the value of the

most recently purchased items.

II. Average cost (AVCO). Under this method a new average value (usually the weighted

average using the number of items bought) is calculated each time a new delivery of

inventory is received.

• IAS 2 does not allow for inventory to be valued using the last in, first out (LIFO)

method. Inventories which are similar in nature and use to the business will use the

same valuation method. Only where inventories are different in nature or use, a

different valuation method be used. Once a suitable method of valuation has been

adopted by a business then it should continue to use that method unless there are good

reasons why a change should be made. This is in line with the consistency concept.

10.

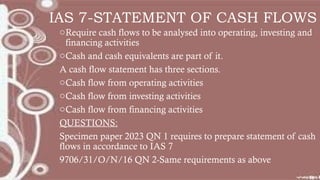

IAS 7-STATEMENT OFCASH FLOWS

oRequire cash flows to be analysed into operating, investing and

financing activities

oCash and cash equivalents are part of it.

A cash flow statement has three sections.

oCash flow from operating activities

oCash flow from investing activities

oCash flow from financing activities

QUESTIONS:

Specimen paper 2023 QN 1 requires to prepare statement of cash

flows in accordance to IAS 7

9706/31/O/N/16 QN 2-Same requirements as above

12.

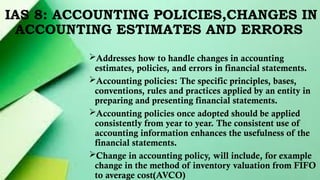

IAS 8: ACCOUNTINGPOLICIES,CHANGES IN

ACCOUNTING ESTIMATES AND ERRORS

Addresses how to handle changes in accounting

estimates, policies, and errors in financial statements.

Accounting policies: The specific principles, bases,

conventions, rules and practices applied by an entity in

preparing and presenting financial statements.

Accounting policies once adopted should be applied

consistently from year to year. The consistent use of

accounting information enhances the usefulness of the

financial statements.

Change in accounting policy, will include, for example

change in the method of inventory valuation from FIFO

to average cost(AVCO)

13.

IAS 8: ACCOUNTING

POLICIES,CHANGESIN ACCOUNTING

ESTIMATES AND ERRORS

A change in accounting policy is permitted only if the change:

is required by a new IAS

results in more true and fair view of financial statements

Dealing with errors:

Errors such as mathematical mistakes, misinterpretation of facts, misapplication

of notes may occur need to be corrected retrospectively in next set of financial

statements authorized after their discovery.

Example of significant error-Uber: Incorrectly calculated driver commissions,

reducing profit by $45–50 million.

14.

IAS 10-EVENTS AFTERREPORTING PERIOD

oThe first version of IAS 10 was issued in 1978, and formed on Jan 2005

Objective:

When: the entity should adjust its financial statement for the effects of the event that happened

after the reporting period

What: disclosures an entity should give in relation to these events in the financial system

Also; If the events after the event after the reporting period indicate that going concern

assumption is not appropriate than the entity should not prepare it's financial statements on the

going concern basis

oEvents after reporting period :

-The end of reporting period

-The date when financial statements are authorised for issue

IAS 10 applies to all business entities that prefer International Financial Reporting Standards

(IFRS)

15.

IAS 10-EVENTS AFTERREPORTING

PERIOD

TYPES OF EVENTS :

1)ADJUSTING EVENTS

Events that provide additional evidence of conditions that existed at the end of the

reporting period. The financial statements much be adjusted.

Example Bankruptcy of a consumer, Inventory written down.

2)NON ADJUSTING EVENTS

Events that do not relate to conditions exiting at the end of the reporting period but

are significant enough that the users of the financial statement should be informed,

here the financial statements are not adjusted but disclosure is required Examples;

Natural disasters, Major business combinations Significant changes In the share price.

16.

IAS 10-EVENTS AFTERREPORTING PERIOD

Conclusion: IAS 10 ensures that financial statements reflect all relevant post-reporting events while preventing

misleading adjustments for events that do not relate to past conditions. It balances the need for accuracy and

timeliness in financial reporting, ensuring that users receive a fair and complete view of an entity’s financial

position.

Question:

There was a flood at the company’s premises on 29 July 2011 resulting in a material uninsured

loss of $215 000.

On 14 August 2011 the company declared its final dividend for the year ended 30 June 2011 of $0.03 per

share.

IAS 10 (events after the statement of financial position date) identifies two types of event as

adjusting events and non-adjusting events.

REQUIRED

1. State the difference between adjusting and non-adjusting events. Explain their treatment in the

financial statements. [4]

2. State if the items in points 4 and 5 in the additional information are adjusting or non-adjusting events.

Justify your answer. [4] (November 2011)

17.

IAS 16-PROPERTY,PLANT&EQUIPMENT

• Property,Plant and Equipment : This standard sets out how

property, plant and equipment is dealt with.

• Plant, property and equipment is measured at cost. Cost includes

the purchase price, plus any import duties, plus any costs

attributable to make the asset fit for use at the intended location,

plus any estimated costs of dismantling and removing the asset at

the end of its life.

• After acquisition the company must chose to value its assets using:

1)Cost – the asset is shown at cost less accumulated depreciation

and impairment losses.

2)Revaluation– the asset is shown at a revalued amount (that is an

amount at which the asset could be exchanged between

knowledgeable, willing parties in an arm’s length transaction) less

subsequent depreciation and impairment losses.

18.

IAS 16-PROPERTY,PLANT&EQUIPMENT

Depreciation isto be charged on all non-current assets with the exception of

freehold land.

The two methods examined are:

The straight-line method

The diminishing (reducing) balance method.

The company chooses the method in a manner that reflects the way in which

the assets’ economic benefits are consumed.

The method used should be reviewed at least annually in order to consider

whether the method used is still the most appropriate method.

20.

IAS 36-IMPAIRMENT OFASSETS

Impairment: A fall in the value of an asset, so that its recoverable amount is

now less than its carrying value in the balance sheet.

This standard sets out the accounting treatment to ensure that assets are

shown in the balance sheet at no more than their value or recoverable amount.

The recoverable amount is the higher of a fair value less any costs that would

be incurred were it to be sold and its present value in use.

The standard applies to non-current assets. Assets need to be reviewed at

each balance sheet date to judge whether there is evidence of any impairment.

If there is an impairment loss, the asset should be shown on the balance

sheet at its recoverable amount and the impairment loss should be shown on

the income statement as an expense.

22.

IAS 37-PROVISIONS, CONTINGENT

LIABILITIESAND CONTINGENT ASSETS

• The objective of the standard is to make sure that appropriate recognition

criteria and measurement bases are applied to provisions, contingent

liabilities and contingent assets.

Recognition of a provision: A provision must be recognised if, and only if:

• A present obligation exists as a result of a past event (the obligating event)

• Payment is probable (more than 50% likelihood of occurrence)

• The amount can be estimated reliably.

• The obligating event creates a legal or constructive obligation

• The amount recognised as a provision should be the best estimate of the

expenditure required to settle the present obligation at the date of the

statement of financial position.

23.

IAS 37-PROVISIONS, CONTINGENT

LIABILITIESAND CONTINGENT ASSETS

Contingent liabilities :A possible obligation (a

contingent liability) is disclosed in the notes to

the financial statements, but not recognised.

However, where the possibility of payment is

remote, no recognition or disclosure is required.

Contingent assets :These should not be

recognised in the financial statements, but

should be disclosed in the notes to the financial

statements where an inflow of economic

benefits is probable and the amount is material.

Where the inflow of economic benefits is

possible or remote, there should be no

recognition and no disclosure.

24.

IAS 38-INTANGIBLE ASSETS

•This standard covers the accounting treatment for intangible assets.

The three critical attributes of an intangible asset are:

• It must be identifiable

• It must be controlled by the entity

• The entity must be able to obtain future economic benefits from the asset such as

revenue or reduced costs

The standard requires an entity to recognise an intangible asset, whether purchased or

self-created (at cost), if:

• • it is probable that the future economic benefits attributable to the asset will flow to

the entity;

• The cost of the asset can be measured reliably.

• The probability of future economic benefits must be based on reasonable and

supportable

• Assumptions about conditions that will exist over the life of the asset.

25.

IAS 38-INTANGIBLE ASSETS

Specificcases

• Research and development costs

• Internally generated brands, customer lists

• Computer software

• Other types of cost Eg internally generated goodwill

Measurement subsequent to acquisition

• Similarly to tangible non-current assets, an entity must choose either

the cost model or the revaluation

• Model for each class of intangible asset.

• Classification based on useful life

• Intangible assets are classified as having either an indefinite life or a

finite life.

26.

IAS 38-INTANGIBLE ASSETS

Disclosure

Foreach class of intangible asset, the following should be disclosed:

1)Useful life or amortisation rate

2)Amortisation method

3)Gross carrying amount

4)Accumulated amortisation and impairment losses

5)Reconciliation of the carrying amount at the beginning and end of

the reporting period

6)The basis for determining that an intangible asset has an indefinite

life

7)Description and carrying amount of individually material

intangible assets.

![IAS 10-EVENTS AFTER REPORTING PERIOD

Conclusion: IAS 10 ensures that financial statements reflect all relevant post-reporting events while preventing

misleading adjustments for events that do not relate to past conditions. It balances the need for accuracy and

timeliness in financial reporting, ensuring that users receive a fair and complete view of an entity’s financial

position.

Question:

There was a flood at the company’s premises on 29 July 2011 resulting in a material uninsured

loss of $215 000.

On 14 August 2011 the company declared its final dividend for the year ended 30 June 2011 of $0.03 per

share.

IAS 10 (events after the statement of financial position date) identifies two types of event as

adjusting events and non-adjusting events.

REQUIRED

1. State the difference between adjusting and non-adjusting events. Explain their treatment in the

financial statements. [4]

2. State if the items in points 4 and 5 in the additional information are adjusting or non-adjusting events.

Justify your answer. [4] (November 2011)](https://image.slidesharecdn.com/ias-250312072051-5dce2726/85/International-accounting-standards-for-year-13-16-320.jpg)

![igcse 421702998-Acc2-Report [Autosaved].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/421702998-acc2-reportautosaved-251114165537-0a29fa9f-thumbnail.jpg?width=640&height=640&fit=bounds)