Downloaded 483 times

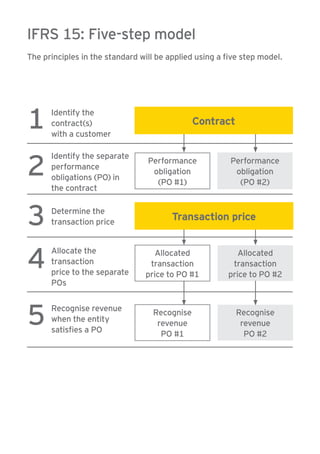

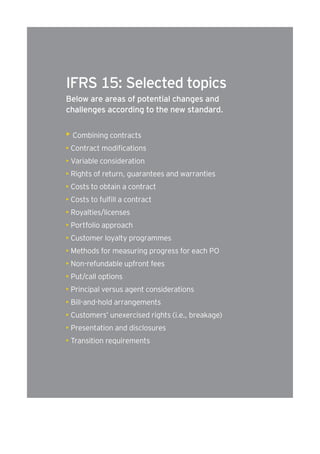

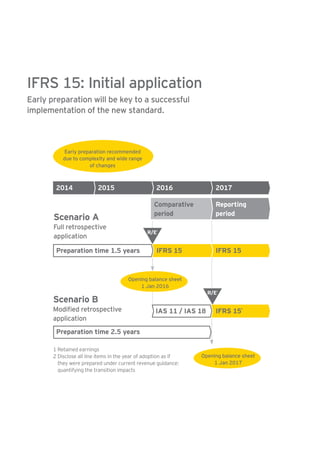

The document outlines IFRS 15, the new revenue recognition standard, which introduces a unified model for recognizing revenue from contracts with customers, effective from January 1, 2017. It emphasizes the importance of early preparation for implementation due to the complexity and wide range of changes involved, and details a five-step model for applying the standard. Specific industry challenges and considerations for transition are also highlighted, along with the necessary resources for compliance and implementation support.