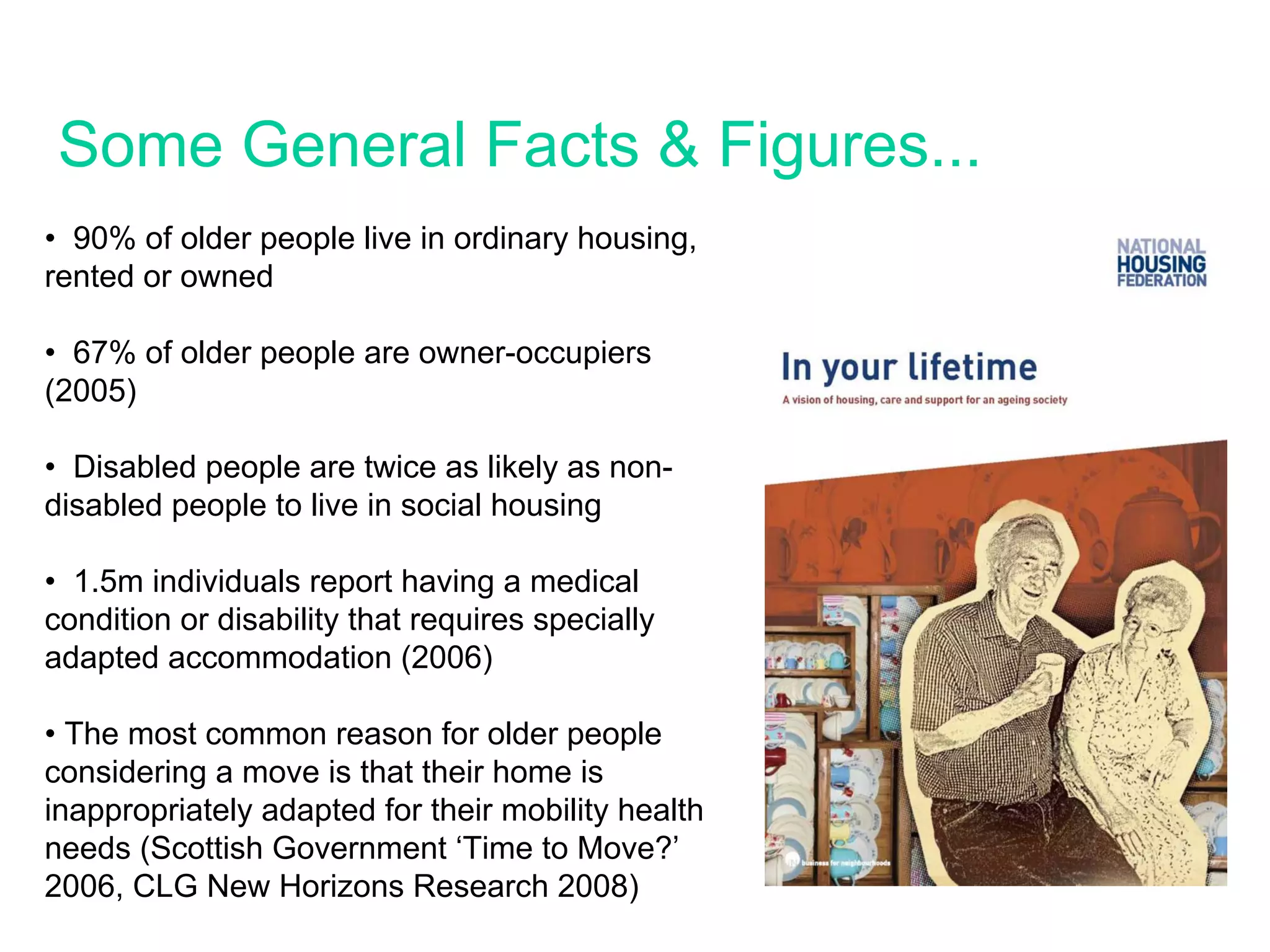

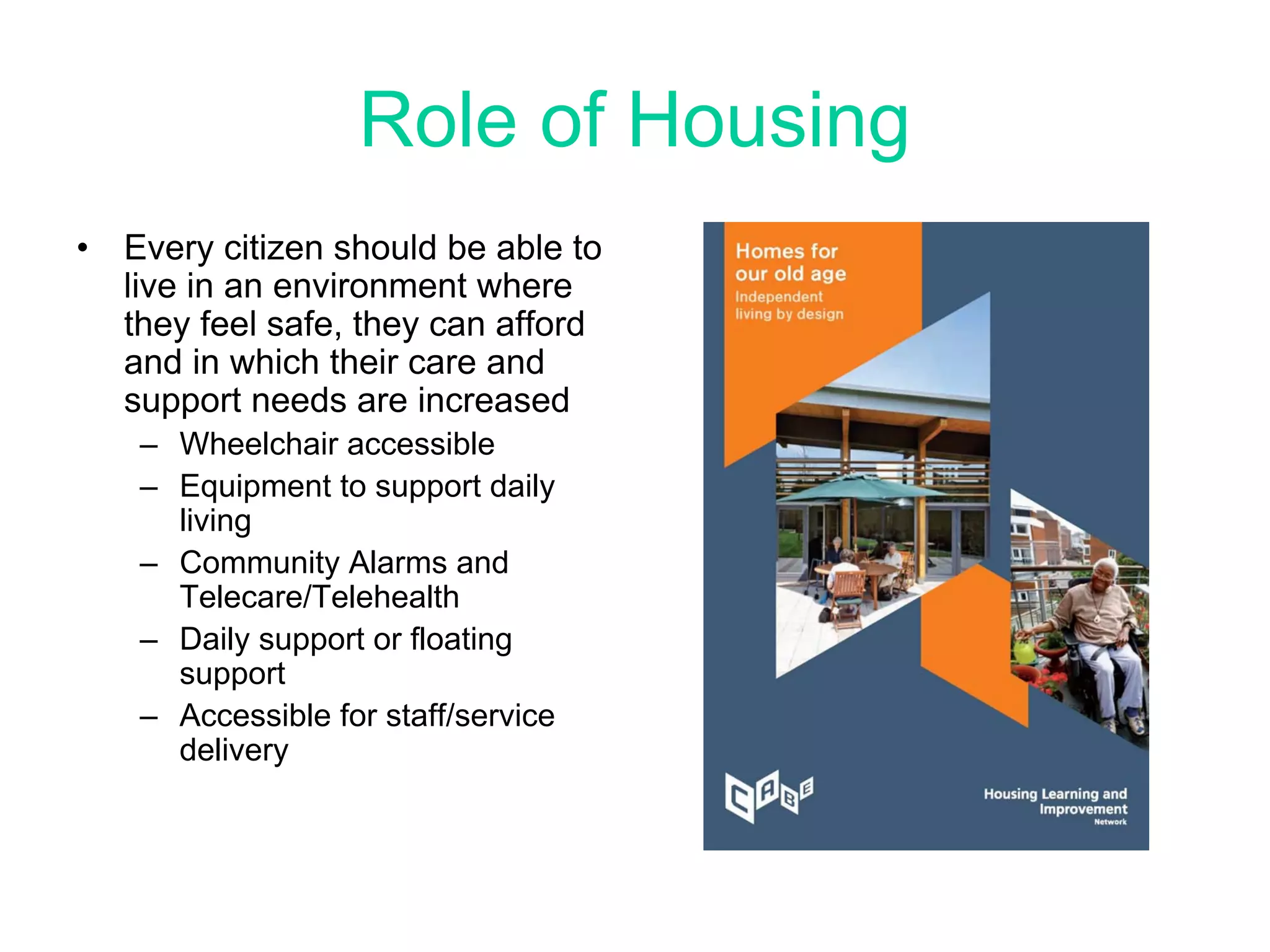

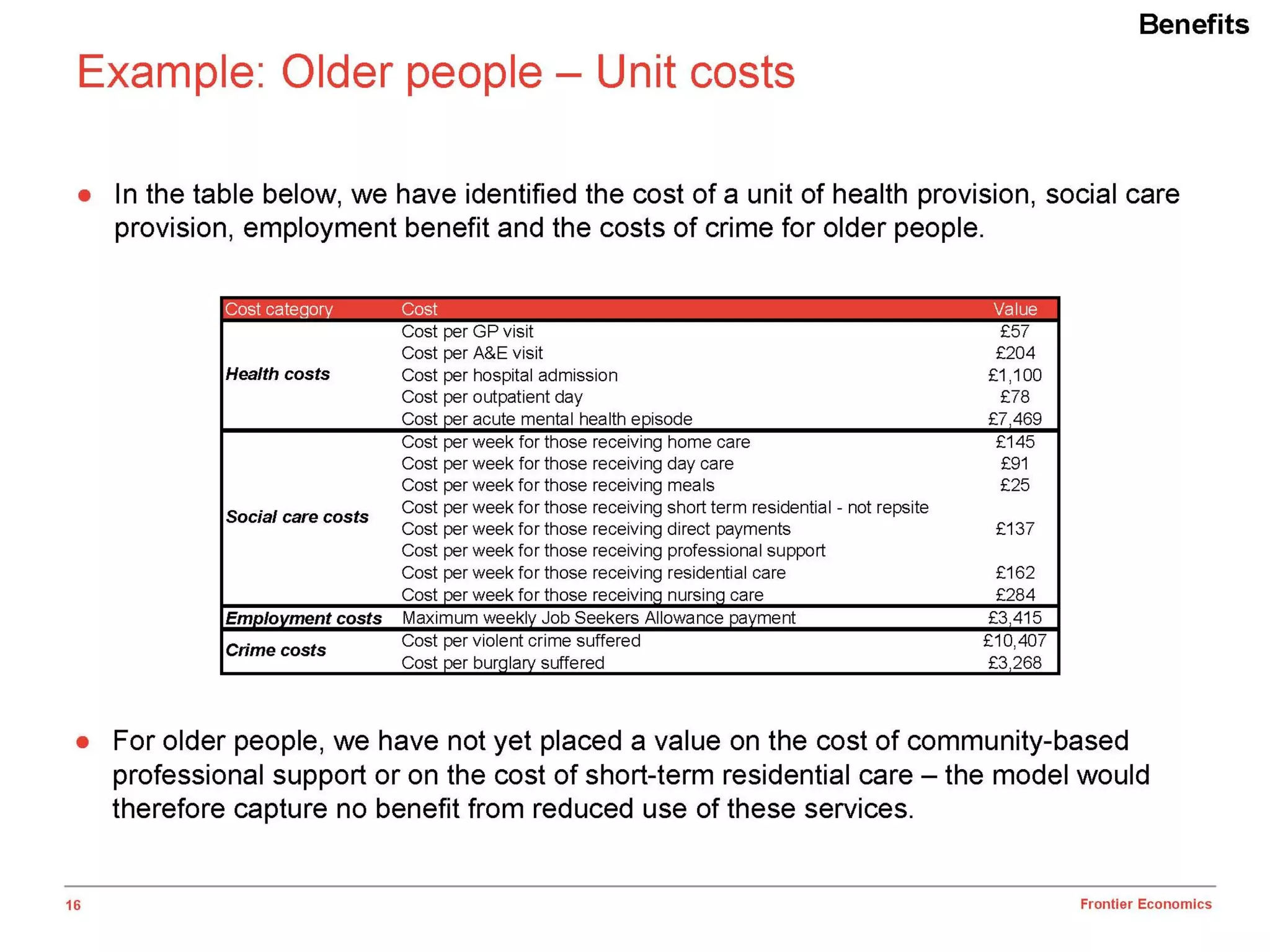

This document discusses the relationship between housing and health, and innovative housing options for older adults. It notes that home modifications can prevent costly falls and injuries, delay entry into residential care, and reduce hospital readmissions. The document then addresses perceived challenges for organizations in providing housing and care, including developing a future vision, addressing sustainability concerns, and fostering innovation. It also discusses the health drivers for good quality housing, an aging population's changing needs and preferences, and general facts about older adults' living situations.