The document is an internship report on GST returns and tally, submitted by Goldy Singh for the MBA program under the mentorship of Mr. XYZ. It discusses the implementation, objectives, challenges, and benefits of GST in India, including issues of tax evasion and methods of compliance. The report outlines a framework for GST regulations, the roles of tax authorities, and provides an analysis of tax filing processes.

1

INTERNSHIP REPORT (Batch20………..)

on

GST Return & Tally

Under the mentorship of

Mr. XYZ

Faculty Mentor Submitted by

GOLDY SINGH

MBA 3A

2.

2

CERTIFICATE

This is tocertify that the …………, roll number 2……… having project report entitled “GST

Return & Tally” done under mentorship of Mr.XYZ…, finance department, XYZ

COMPANY..., submitted to the Department of Management Studies, XYZ University in

partial fulfilment for the course of Management Trainee (MGT-202).

Date

Dr XYZ

Assistant Professor

Department of Management Studies

3.

3

Acknowledgement

With immense pleasure,I would like to present this training report on “GST Return & Tally”.

I take the opportunity to express my gratitude to all of them who in some or the other way

helped me to accomplish this project. The study cannot be completed without your guidance,

assistance, inspiration, and co-operation.

I owe my gratitude to various employees; without their help I would have been unable to

complete my project. These people have really been kind enough to help me by answering my

questions. I would also like to thank MR. XYZ who has always there to help and guide me

when I needed help.

I am thankful to them for encouraging me. I am thankful to them for all the addition and

enhancement done to me. It was because of their immense help and support that this project

has been duly completed.

However, I accept the sole responsibility for any possible error and would be extremely grateful

to the readers of this report if they bring such mistakes to my notice.

4.

4

INDEX

1. Cover Page……………………………………………………………….1

2.Training Completion Certificate………………………………………....2

3. Candidate Declaration…………………………………………………....3

4. Acknowledgment………………………………………………………...4

5. Index……………………………………………………………………..5

6. Company Profile ………………………………………………………...6

7. GOODS AND SERVICE TAX(CHAPTER 1)………………………….10

a) Introduction of GST……………………………………...11

b) Literature Review………………………………………...23

c) Research Methodology…………………………………...27

d) Objectives of the study…….……………………..………28

e) Limitations of the study………………………….……….29

f) Findings and Analysis…………………………..………..29

g) Conclusions……………..…………………………..……30

h) Recommendations………………………………………..31

i) Reference…………………………………………………32

8. TALLY PRIME (CHAPTER 2)…………………….. …………………..33

a) Introduction………………………………………………34

b) Research Methodology……………….…………………..47

c) Objectives of the study……………….…………………..48

d) Limitations of the study………….……………………….48

e) Findings and Analysis……………...……………………..49

f) Conclusions………………………………………………..51

g) Recommendations…..……………………………………..52

h) Reference…………………………………………………..52

7

GST (Goods &Service Tax)

ABSTRACT

Since the implementation of the Goods and Services Tax (GST) in India, there were high hopes

that it would enhance government revenue, create a unified market, and eliminate the cascading

effect of taxes. While GST has achieved many of these objectives, it has not completely

eradicated tax evasion and related fraud, which were prevalent in the earlier Value Added Tax

(VAT) system. This paper investigates various modes of tax evasion and the shortcomings in

the regulatory framework of GST that address these issues. Additionally, the study explores

the measures available for curbing tax fraud.

INTRODUCTION

The Kelkar Task Force Committee, which examined the implementation of the Fiscal

Responsibility and Budget Management (FRBM) Act, 2003, highlighted persistent issues in

India's indirect tax policy. Despite moving towards the VAT principle since 1986, the taxation

of goods and services remained fraught with challenges. The tax base was fragmented between

the Central and state governments, and services, a significant portion of the GDP, were not

appropriately taxed. In response, the Kelkar Task Force proposed a comprehensive Goods and

Services Tax (GST) based on the VAT principle. After extensive deliberation, the One Hundred

and First Amendment of the Constitution of India in 2016 introduced a national GST on July

1, 2017, ushering in the era of 'One Nation, One Tax, One Market.' GST, a multi-stage,

destination-based consumption tax, relies on the credit invoice method, taxing only the value

addition at each stage while facilitating the seamless flow of credit along the supply chain. It

replaces all previous indirect taxes on goods and services with a unified system from

manufacturers to consumers, comprising Central GST (CGST), State GST (SGST), and

Integrated GST (IGST).

8.

8

Rationale for GSTImplementation

The shift to GST from the previous complex structure of indirect taxes was motivated by the

need for simplification. Central and State Governments imposed a multitude of taxes, including

Central Excise Duty, Service Tax, Central Sales Tax, VAT, Entry Tax, and more. Each tax was

separate, with varying provisions and compliance requirements, leading to multiple tax evasion

avenues and compliance challenges. The introduction of GST in July 2017 aimed to streamline

this tax regime, bringing uniform tax rates for intra-state and inter-state transactions. Key

outcomes of GST implementation include

Eliminating Cascading Taxes: GST has effectively removed the cascading effect of

taxes by allowing Input Tax Credit on the value addition at each stage of the supply

chain.

Harmonization: It has harmonized tax laws, procedures, and rates across the country,

creating a unified tax structure.

Boosting Investment Climate: GST has improved the overall investment climate in

India, benefiting state-level development.

Enhanced Compliance: The environment of compliance has been improved through

online tax return filing and online verification of input credits, encouraging a more

transparent transaction record.

Unified National Market: GST has eliminated inter-state economic barriers, fostering

the creation of a unified national market.

Increased Government Revenue: It has contributed to government revenue growth by

expanding the tax base and enhancing taxpayer compliance.

9.

9

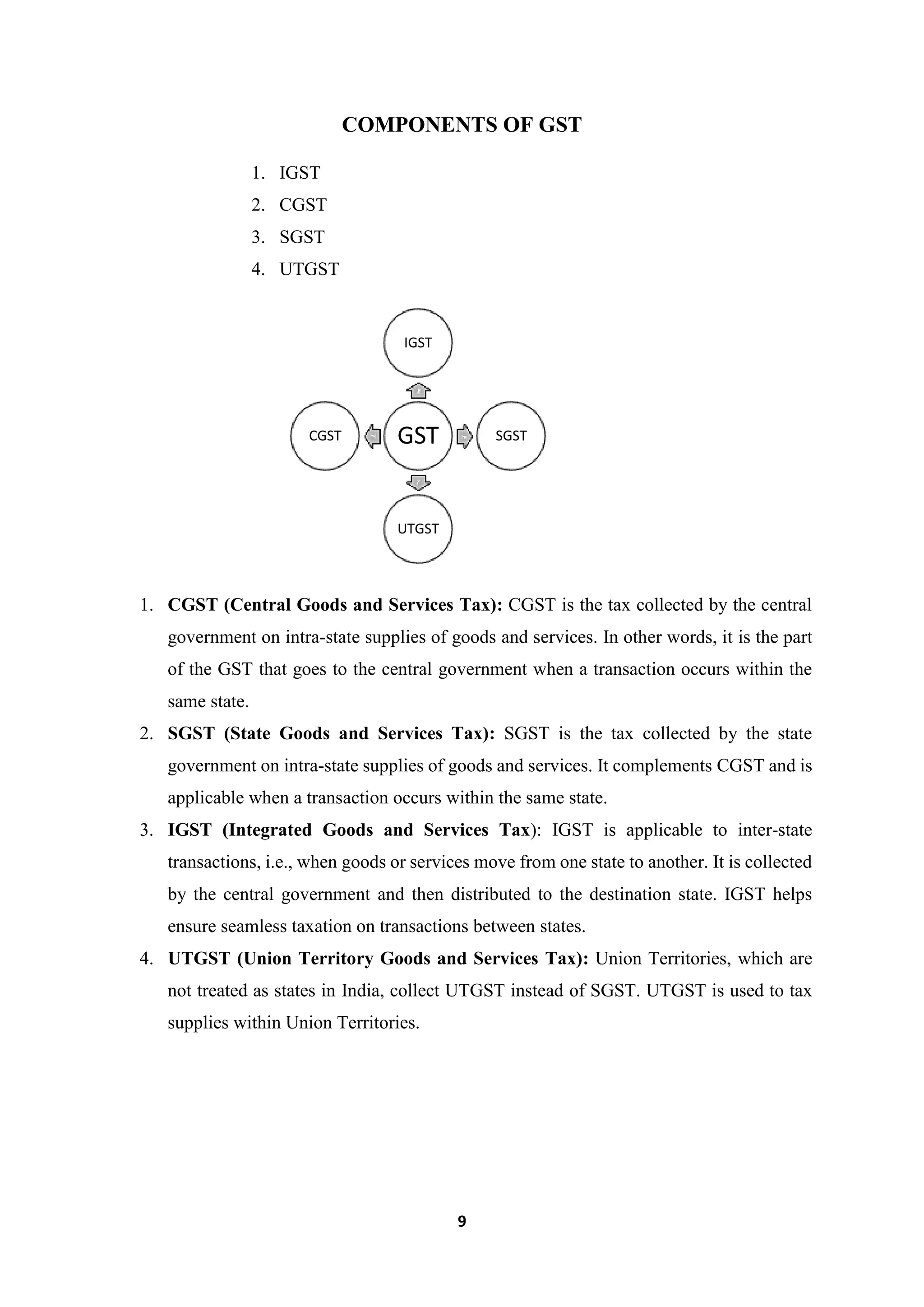

COMPONENTS OF GST

1.IGST

2. CGST

3. SGST

4. UTGST

1. CGST (Central Goods and Services Tax): CGST is the tax collected by the central

government on intra-state supplies of goods and services. In other words, it is the part

of the GST that goes to the central government when a transaction occurs within the

same state.

2. SGST (State Goods and Services Tax): SGST is the tax collected by the state

government on intra-state supplies of goods and services. It complements CGST and is

applicable when a transaction occurs within the same state.

3. IGST (Integrated Goods and Services Tax): IGST is applicable to inter-state

transactions, i.e., when goods or services move from one state to another. It is collected

by the central government and then distributed to the destination state. IGST helps

ensure seamless taxation on transactions between states.

4. UTGST (Union Territory Goods and Services Tax): Union Territories, which are

not treated as states in India, collect UTGST instead of SGST. UTGST is used to tax

supplies within Union Territories.

GST

IGST

SGST

UTGST

CGST

10.

10

REGULATORY AUTHORITIES

The Goods& Services Tax Council is the highest regulatory authority responsible for

offering recommendations to both the Union and State Governments on matters pertaining

to Goods and Service Tax (GST). Established in accordance with Article 279A of the

amended Constitution, the GST Council holds a constitutional status and is chaired by the

Union Finance Minister. Its members include the Union State Minister of Revenue or

Finance, along with the Ministers in charge of Finance or Taxation from all the states. The

GST Council serves as the principal policymaking body, and it is only upon its

recommendations that parliament and state legislatures enact laws and rules related to GST.

For operational purposes, the Central Board of Indirect Taxes and Customs (CBIC) and the

states' Commercial Tax Departments (CTD) play a pivotal role in implementing and

regulating GST at the Central and State levels, respectively.

The CBIC, a part of the Department of Revenue under the Ministry of Finance, Government

of India, handles the formulation of policies concerning the levy and collection of Customs,

Central Excise duties, Central Goods & Services Tax, Integrated Goods & Services Tax

(IGST), prevention of smuggling, and administration of matters related to Customs, Central

Excise, Central Goods & Services Tax, IGST, and Narcotics within its purview. Similarly,

the States' Commercial Tax Departments (CTD) are responsible for internal resource

mobilization within the State Government and deal with policy formulation and the

collection of State Goods & Services Tax (SGST).

Mandate of GST Council

The GST Council's mandate encompasses various key responsibilities, including:

a) Making recommendations to the Union and the states regarding taxes, cesses, and

surcharges levied by the Union, states, and local bodies, which can be subsumed within the

ambit of goods and services tax.

b) Providing recommendations on the inclusion or exemption of goods and services under

the goods and services tax.

c) Formulating model goods and services tax laws, principles for levying the tax,

apportionment of goods and services tax on supplies in the course of inter-state trade or

commerce under Article 269A, and the principles governing the place of supply.

11.

11

d) Determining thethreshold limit of turnover below which goods and services may be

exempted from goods and services tax.

e) Recommending the rates, including floor rates with bands, for goods and services tax.

f) Suggesting special rates for a specified period to raise additional resources during natural

calamities or disasters.

g) Creating special provisions for certain states, such as Arunachal Pradesh, Assam, Jammu

and Kashmir, Manipur, Meghalaya, Mizoram, Nagaland, Sikkim, Tripura, Himachal

Pradesh, and Uttarakhand.

h) Addressing any other matter related to the goods and services tax, as determined by the

GST Council.

MAJOR MODES OF TAX EVASION UNDER GST

Under the Goods and Services Tax (GST) regime, Sections 42 and 43 of Chapter IX of the

Central Goods and Services Tax (CGST) and State Goods and Services Tax (SGST) Acts

provide a framework for matching tax invoices, a cornerstone of the GST system. However,

challenges and modes of tax evasion have arisen as follows:

1.MISMATCH IN INVOICES

Matching invoices is pivotal to the equitable distribution of Input Tax Credit (ITC) on the

Goods and Services Tax Network (GSTN). The transaction of goods and services from one

party to another creates a chain the seller's supply is the buyer's purchase. Suppliers must

declare all supplies in their GSTR1, which should align with the recipient's

GSTR2A/GSTR2 for ITC to be eligible. ITC can only be availed to the extent that invoices

match, making this a real-time, monthly process where parties upload invoices and

counterparts accept. While GST extended ITC availability from intra-state to inter-state

supplies, the high volume of transactions and invoice mismatches pose a significant

challenge to achieving a balance between fair ITC distribution and safeguarding public

revenue. Mismatches can occur when:

The recipient avails more ITC than the tax declared by the supplier.

The recipient claims ITC, but the supplier does not declare the outward supply.

The recipient falsely claims Input Tax Credit.

12.

12

2.OVER-CLAIMING OF INPUTTAX CREDIT (ITC)

Over-claiming ITC is an explicit way to exploit the ITC mechanism. Established businesses

with GST liabilities on their outputs face limits in this regard, as excessive credit claims

would suggest unrealistically low profit margins. However, new businesses have more

leeway to exaggerate input claims without raising suspicion, especially if they make

significant initial purchases of capital goods and inputs without an immediate

corresponding level of sales. Export frauds also lead to fraudulent claims, with goods not

actually being exported out of the country. Such fraud may involve fictitious commodities

or authentic ones sold in the domestic market. A false ITC credit claim of ₹1 costs the

government the same as a fraudulent refund of ₹1. Therefore, fraudulent ITC refunds are a

major concern.

3. FAILURE OF BUSINESSES TO REGISTER

In the GST system, businesses operating near the threshold for compulsory registration

often fail to register. This helps them evade both the GST for which they are liable and

GST compliance costs. These businesses, often referred to as "ghosts," remain entirely

unknown to revenue authorities, and they can potentially evade both income taxes and GST.

This category typically comprises firms selling to final consumers or other unregistered

businesses.

4.TAX COLLECTED BUT NOT REMITTED

Tax evasion may occur when businesses charge customers GST but fail to remit the

collected tax to the authorities. The so-called "missing trader" frauds usually involve

registered businesses that vanish before paying the due tax. This may result from

underreporting sales, engineering bankruptcy before paying taxes, or other tactics.

Addressing these modes of tax evasion is essential for ensuring the integrity of the GST system

and preserving government revenue. Effective measures and continuous improvements in the

GST framework are necessary to combat fraudulent practices and maintain tax compliance.

13.

13

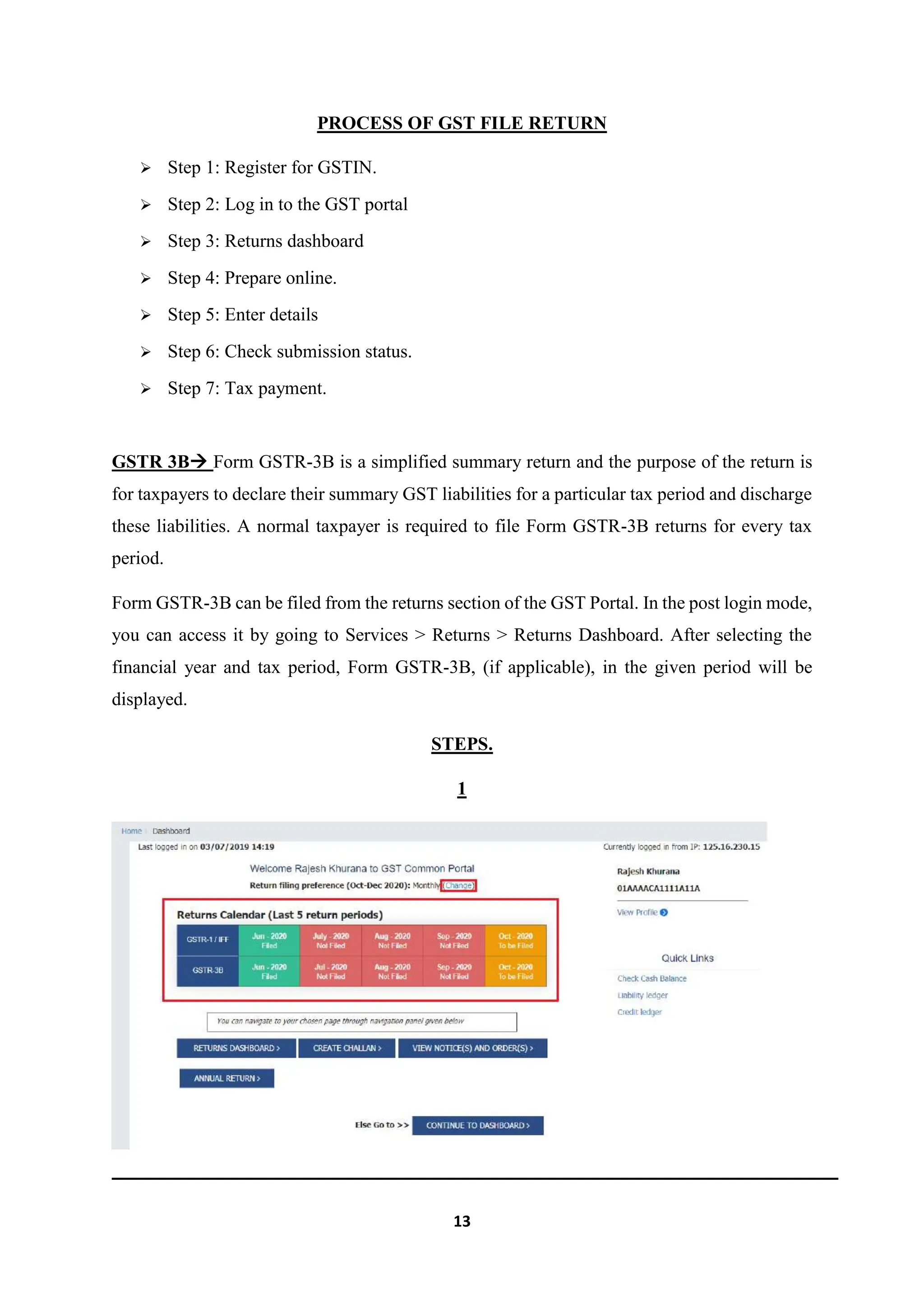

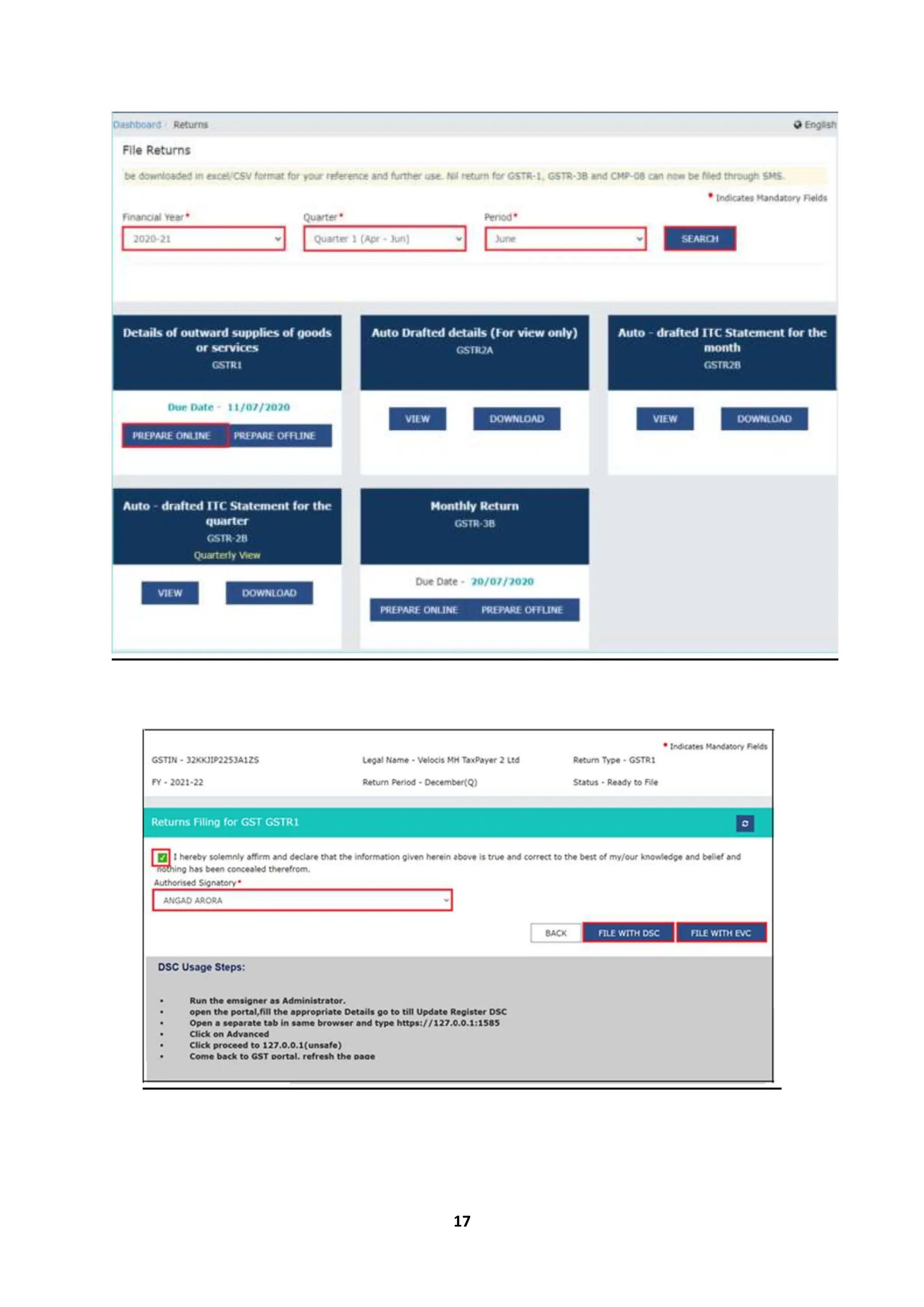

PROCESS OF GSTFILE RETURN

Step 1: Register for GSTIN.

Step 2: Log in to the GST portal

Step 3: Returns dashboard

Step 4: Prepare online.

Step 5: Enter details

Step 6: Check submission status.

Step 7: Tax payment.

GSTR 3B Form GSTR-3B is a simplified summary return and the purpose of the return is

for taxpayers to declare their summary GST liabilities for a particular tax period and discharge

these liabilities. A normal taxpayer is required to file Form GSTR-3B returns for every tax

period.

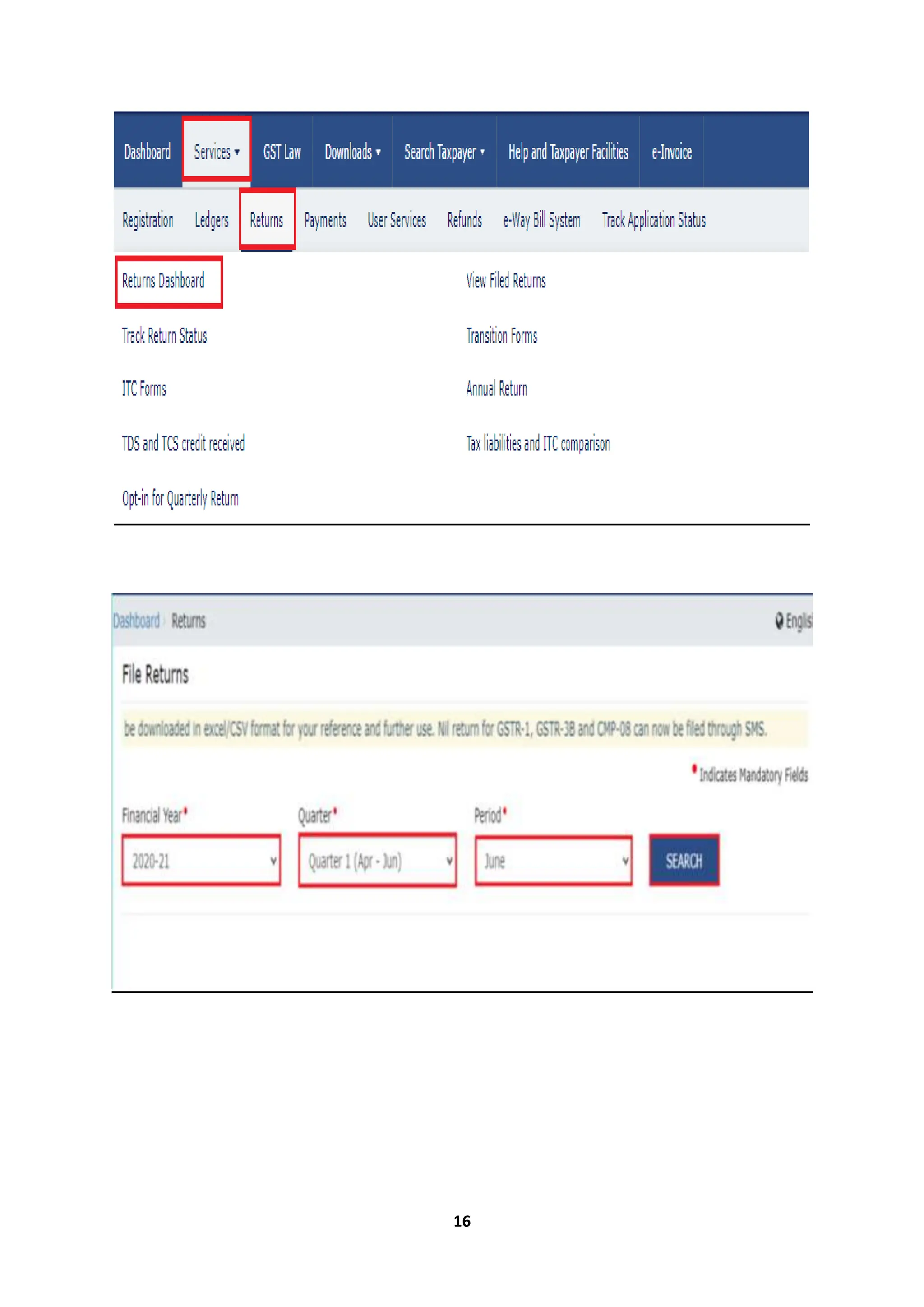

Form GSTR-3B can be filed from the returns section of the GST Portal. In the post login mode,

you can access it by going to Services > Returns > Returns Dashboard. After selecting the

financial year and tax period, Form GSTR-3B, (if applicable), in the given period will be

displayed.

STEPS.

1

15

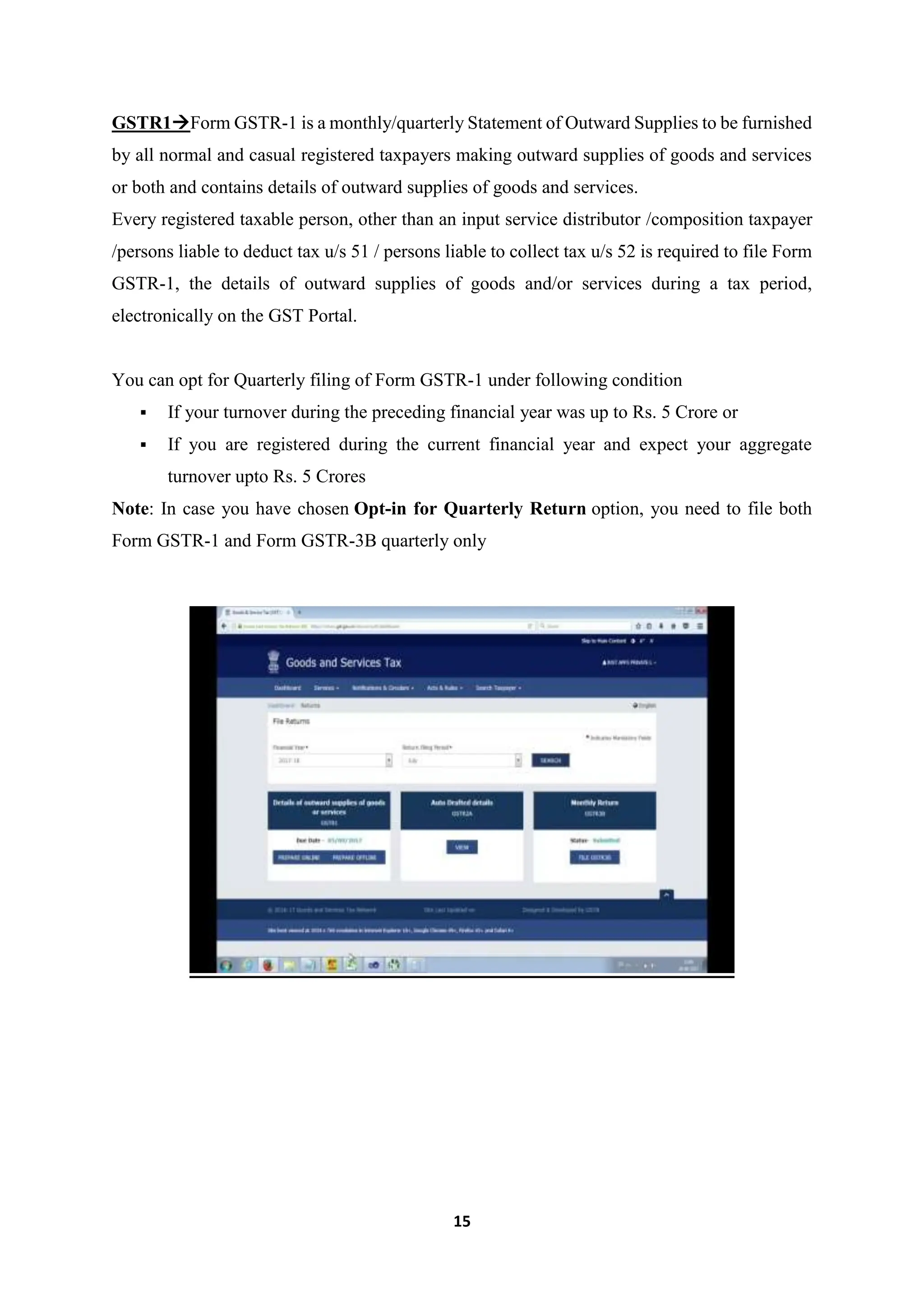

GSTR1Form GSTR-1 isa monthly/quarterly Statement of Outward Supplies to be furnished

by all normal and casual registered taxpayers making outward supplies of goods and services

or both and contains details of outward supplies of goods and services.

Every registered taxable person, other than an input service distributor /composition taxpayer

/persons liable to deduct tax u/s 51 / persons liable to collect tax u/s 52 is required to file Form

GSTR-1, the details of outward supplies of goods and/or services during a tax period,

electronically on the GST Portal.

You can opt for Quarterly filing of Form GSTR-1 under following condition

If your turnover during the preceding financial year was up to Rs. 5 Crore or

If you are registered during the current financial year and expect your aggregate

turnover upto Rs. 5 Crores

Note: In case you have chosen Opt-in for Quarterly Return option, you need to file both

Form GSTR-1 and Form GSTR-3B quarterly only

18

Who should fileGST Returns?

Under the GST regime, regular businesses having more than Rs.5 crore as annual aggregate

turnover (and taxpayers who have not opted for the QRMP scheme) have to file two monthly

returns and one annual return. This amounts to 25 returns each year.

Taxpayers with a turnover of up to Rs.5 crore have the option to file returns under the QRMP

scheme. The number of GSTR filings for QRMP filers is 9 each year, which include 4 GSTR-

1 and GSTR-3B returns each and an annual return. Note that QRMP filers have to pay tax on

a monthly basis even though they are filing returns quarterly.

There are also separate statements/returns required to be filed in special cases such as

composition dealers where the number of GSTR filings is 5 each year (4 statement-cum-

challans in CMP-08 and 1 annual return GSTR-4).

Returns are there under GST

There are 13 returns under GST. They are the GSTR-1, GSTR-3B, GSTR-4, GSTR-5, GSTR-

5A, GSTR-6, GSTR-7, GSTR-8, GSTR-9, GSTR-10, GSTR-11, CMP-08, and ITC-04.

However, all returns do not apply to all taxpayers. Taxpayers file returns based on the type of

taxpayer/type of registration obtained.

Eligible taxpayers, i.e. with a turnover exceeding Rs.5 crore are also required to also file a self-

certified reconciliation statement in Form GSTR-9C.

Besides the GST returns that are required to be filed, there are statements of input tax credit

available to taxpayers, namely GSTR-2A (dynamic) and GSTR-2B (static). There is also an

Invoice Furnishing Facility (IFF) available to small taxpayers who are registered under the

QRMP scheme to furnish their Business to Business (B2B) sales for the first two months of the

quarter. These small taxpayers will still need to pay taxes on a monthly basis using Form PMT-

06.

19.

19

Literature Review

The chosenresearch area for this study focuses on taxation, and as part of the literature review,

various reports of committees on taxes appointed by the Government of India over the years

have been examined.

Parthasarathi Shome Committee (2001) The Parthasarathi Shome Committee,

appointed by the Indian government, focused on tax reforms. It recommended changes

to the tax regime to encourage voluntary compliance, simplify tax laws, and reduce

litigation. The committee also examined issues related to tax administration and transfer

pricing.

Vijay Kelkar Task Force on Direct Taxes (2002) This task force, led by Dr. Vijay

Kelkar, made recommendations for simplifying and rationalizing the direct tax system

in India. It proposed measures to broaden the tax base, reduce tax rates, and improve

tax administration. The task force's recommendations aimed to make the tax system

more taxpayer-friendly and efficient.

Tax Administration Reform Commission (TARC, 2014) TARC was established to

examine the existing tax administration system in India and suggest reforms. It

proposed measures to enhance the efficiency and effectiveness of tax administration,

reduce litigation, and improve taxpayer services. TARC's recommendations aimed at

creating a taxpayer-centric tax administration system.

Justice Easwar Committee (2016) The committee led by Justice R.V. Easwar was

formed to simplify income tax laws and reduce litigation. It made recommendations to

streamline the tax dispute resolution process, making it more efficient and taxpayer-

friendly.

Direct Tax Code Committee (2009) The Direct Tax Code Committee, also known as

the Chidambaram Committee, was tasked with drafting a new direct tax code. Its report

contained comprehensive recommendations for the reform of direct taxes in India,

including changes to tax rates, exemptions, and simplification of tax laws.

20.

20

Direct TaxCode Committee (2009) The Direct Tax Code Committee, also known as

the Chidambaram Committee, was tasked with drafting a new direct tax code. Its report

contained comprehensive recommendations for the reform of direct taxes in India,

including changes to tax rates, exemptions, and simplification of tax laws.

Task Force on Direct Tax Code (2017) This task force was set up to review the

existing Income Tax Act and provide recommendations for a new Direct Tax Code. Its

focus was on simplifying and rationalizing India's direct tax laws.

Raja Chelliah Committee (1991) The Raja Chelliah Committee played a significant

role in recommending tax reforms, including the introduction of Value Added Tax

(VAT) and the restructuring of India's tax system.

K.N. Raj Committee (1975) This committee was responsible for examining the Indian

income tax structure and recommending changes to promote equity and economic

development.

R. V. Gupta Committee (1984) The R. V. Gupta Committee focused on tax

exemptions and incentives for the industrial sector, with the aim of promoting industrial

growth and investment.

Justice K.N. Wanchoo Committee (1971) This committee was formed to review the

existing tax laws and recommend measures to reduce tax evasion and improve tax

compliance.

Indirect Taxation Enquiry Committee (1947) This historical committee played a

vital role in shaping India's early indirect tax system, making recommendations on

customs and excise duties.

Kelkar Committee on GST (2009) Dr. Vijay Kelkar led a committee to recommend a

Goods and Services Tax (GST) system for India, which ultimately led to the

implementation of GST in the country.

21.

21

Justice ShahCommittee (2013) The committee, headed by Justice M.B. Shah, focused

on black money and suggested measures to curb the generation and circulation of

unaccounted wealth.

Justice A.P. Shah Committee (2018) This committee was appointed to provide

recommendations for a simplified and taxpayer-friendly income tax return form.

Sinha Committee on GAAR (General Anti-Avoidance Rules, 2012) The

Parthasarathi Shome Committee, led by Dr. Parthasarathi Shome, examined the

implementation of General Anti-Avoidance Rules in India and made recommendations.

Amit Mitra Committee on GST Compensation (2020) Dr. Amit Mitra headed a

committee to examine the issue of compensation to states for revenue loss due to the

introduction of GST.

D. R. Mehta Committee (1999): This committee was formed to review the tax

exemption limits for charitable organizations and suggest measures to ensure the proper

utilization of funds for charitable purposes.

Chelliah Committee on Tax Reforms (1992): The Chelliah Committee focused on

comprehensive tax reforms, covering direct and indirect taxes. It made

recommendations to simplify and rationalize the tax system.

N. K. Singh Committee on Fiscal Responsibility (2003): This committee was tasked

with suggesting measures to ensure fiscal responsibility and budget discipline. It aimed

to create a framework for responsible fiscal management.

Task Force on the Direct Tax Code (2018): A more recent task force was set up to

revisit and revise the existing Direct Tax Code to align it with the evolving economic

landscape and international tax practices.

Justice Narasimham Committee (1991): This committee examined banking sector

reforms, including issues related to non-performing assets and the taxation of banking

income.

22.

22

Committee onTaxation of Services (2004): This committee was appointed to make

recommendations on the taxation of services under the Service Tax regime, including

identifying taxable services and tax rates.

Taxation of Agricultural Income Enquiry Commission (1972): This commission

examined the taxation of agricultural income and suggested measures for bringing

agricultural income into the tax net.

Vijay L. Kelkar Committee on Public-Private Partnerships (2015): Focused on

financing infrastructure development through public-private partnerships, this

committee recommended tax measures to encourage private sector participation.

Committee on Taxation of E-commerce (2020): Given the growing significance of

e-commerce, this committee was appointed to explore the taxation of e-commerce

transactions and recommend appropriate tax measures.

Task Force on National Infrastructure Pipeline (2019): This task force examined

the financing of India's national infrastructure projects and made recommendations on

tax incentives and measures to attract investments in the infrastructure sector.

23.

23

Research Methodology

This researchfollows an exploratory approach, drawing primarily on secondary data from

sources such as journals, articles, newspapers, internet resources, research papers, and feedback

obtained from manufacturers and businessmen. The research design is descriptive and

analytical in nature, aligned with the study's objectives.

Exploratory Approach: This research method is like going on an exciting adventure to

explore something new. Instead of answering specific questions, the researchers are on a

journey to discover more about a topic. They are open to unexpected findings and aim to gain

a XYZper understanding.

Data Sources:

Secondary Data: The researchers are not conducting new surveys or experiments.

Instead, they are like detectives, gathering information from existing sources. These

sources include:

a) Journals: They're looking at articles published in academic journals, which are like

magazines for serious researchers.

b) Articles: They're also considering articles from various sources, which are like shorter

pieces of writing on the topic.

c) Newspapers: Information from newspapers is like getting updates from the latest news.

d) Internet Resources: They're exploring what's available on the internet, which is like

tapping into a vast digital library.

e) Research Papers: These are like detailed reports of other researchers' work, and the

researchers are studying them to see what they've discovered.

f) Feedback from Manufacturers and Businessmen: The researchers are talking to

experts in the field – manufacturers and businessmen – to get their valuable insights

and opinions.

24.

24

Objectives of theStudy

To gain a conceptual understanding of GST.

To examine the features of GST in India.

To identify weaknesses in the current GST model in India.

To propose measures for rectifying these weaknesses.

To gain a conceptual understanding of GST: The primary aim of this study is to

develop a clear understanding of the Goods and Services Tax (GST). Researchers want

to grasp the core concepts and principles of how GST works.

To examine the features of GST in India: In this part of the study, the focus is on

understanding the specific characteristics of GST as it is implemented in India. This

includes how it's structured, what rates are applied, and how it operates within the

Indian tax system.

To identify weaknesses in the current GST model in India: The researchers are keen

to pinpoint any shortcomings or flaws in the existing GST system in India. This means

looking for areas where GST might not be working as effectively as intended.

To propose measures for rectifying these weaknesses: Once weaknesses in the GST

model are identified, the study aims to suggest potential solutions or improvements.

The goal is to provide practical recommendations for making the GST system in India

more efficient and effective.

25.

25

Limitations of theStudy

The study has some limitations, which are important to consider:

Due to time constraints, the researchers were only able to engage with a limited number of

manufacturers as part of their study. This means they might have missed uncovering additional

issues and challenges related to GST implementation. If they had more time, they could have

spoken to a larger and more diverse group of manufacturers to get a more comprehensive view.

FINDINGS AND ANALYSIS

Within the company "XYZ Development Engineers Pvt. Ltd.," a detailed examination of the

taxes they pay and the taxes their suppliers pay is carried out. If there are any differences or

inconsistencies between these taxes, adjustments are made in the financial documents. These

corrected documents are then sent back to the supplier.

Additionally, the study highlights the critical role of verifying two important numbers in this

process:

GST Numbers: These numbers are used to identify the suppliers. Ensuring the accuracy of

these numbers is vital to the smooth operation of the GST system within the company.

UDIN (Unique Document Identification Number): UDIN numbers serve as an alternative

means of identification. If there are discrepancies or inaccuracies in the GST numbers, UDIN

numbers can help maintain the integrity of the transactions within the organization.

26.

26

CONCLUSIONS

In summary, thisresearch has aimed to help us better understand Goods and Services Tax

(GST) in India, with a focus on a specific company, XYZ…….. We had several goals in mind:

to explain the key ideas behind GST, to examine how it works in India, to find problems in the

system, and to suggest ways to fix those problems.

Through our investigation, we learned that GST is important for streamlining taxes and

promoting economic growth in India. But its success depends on how carefully it's put into

practice and how we deal with various challenges.

Our study of XYZ……... showed us the importance of thoroughly checking GST numbers and

Unique Document Identification Numbers (UDIN). Doing this helps a company follow the

GST rules and avoid financial problems.

So, here are the main things we've learned:

Companies should have a clear and automated system to check GST numbers and

UDIN.

Training and education about following GST rules are important for the staff.

Keeping a good record of suppliers' GST information and documents is crucial.

It's helpful to work closely with suppliers to make sure everything goes smoothly.

Regular checks and staying up to date with GST rules are key to following the rules.

When in doubt about GST, it's smart to get advice from experts.

By following these ideas, companies can do better with GST and avoid financial problems.

This also helps make the Indian tax system work well. But we should remember that tax rules

can change, so it's important to keep learning and improving how we follow these rules. This

study is just a start toward a more efficient and honest tax system in India, and we should keep

working on it.

27.

27

RECOMMMEDATION

Implement aRobust Verification Process: Develop a systematic verification process

for GST numbers and Unique Document Identification Numbers (UDIN). This process

should involve cross-referencing invoices, suppliers' GSTIN (Goods and Services Tax

Identification Number), and other relevant documents. Ensure that the verification

process is integrated into the procurement and financial systems to automatically flag

discrepancies.

Automate Invoice Matching: Consider implementing automation tools for invoice

matching. Utilize software solutions that can quickly reconcile invoices with supplier

details and GST numbers, reducing the risk of manual errors and discrepancies.

Automation can expedite the verification process and minimize the likelihood of input

tax credit mismatches.

Regularly Update and Verify GSTIN Data: Maintain an up-to-date database of

suppliers' GSTIN information. Periodically verify and validate this data with official

GST records to ensure accuracy. Any discrepancies or changes in suppliers' GSTIN

should be promptly addressed to avoid compliance issues.

Train and Educate Staff: Conduct training programs for staff responsible for GST

compliance and financial operations. Ensure they are well-versed in the verification and

reconciliation process. Training should cover the importance of accurate GST data, the

potential consequences of non-compliance, and the benefits of a meticulous approach.

Leverage Technology for UDIN Verification: Implement technology solutions for

the verification of UDINs. These solutions can help verify the authenticity of

documents, ensuring that they are not tampered with and maintaining data integrity.

Automated UDIN verification tools can streamline this process.

Maintain a Document Trail: Encourage the practice of maintaining a comprehensive

document trail for all GST-related transactions. This includes invoices, receipts, and

other relevant documents. A well-organized document trail can simplify the verification

process and serve as evidence of compliance during audits.

Regularly Audit and Review Processes: Conduct periodic internal audits to assess the

effectiveness of the verification and adjustment process. Review the accuracy of GST

data, compliance with tax laws, and any potential areas for improvement. Address

issues and inconsistencies promptly to maintain financial integrity.

28.

28

Engage withSuppliers Collaboratively: Foster open communication and

collaboration with suppliers. Discuss the importance of accurate GST data and

encourage them to maintain their records diligently. Collaborative relationships can

lead to smoother transactions and reduce the risk of discrepancies.

Stay Informed About GST Regulations: Keep abreast of changes and updates in GST

regulations. Regulatory updates can impact the verification and adjustment process.

Ensure that your organization is always compliant with the latest tax laws and

regulations.

Seek Professional Advice: When in doubt, seek professional advice from tax experts

or consultants who specialize in GST compliance. They can provide guidance on the

evolving GST landscape, help with complex compliance issues, and ensure that your

organization stays on the right side of the law.

Implement Data Analytics: Utilize data analytics tools to identify patterns and

anomalies in financial data. Data analytics can help detect discrepancies and

irregularities in GST-related transactions more efficiently.

Standardize Documentation: Develop standardized templates for invoices, receipts,

and other GST-related documents. Standardization can reduce errors in documentation

and make the verification process more straightforward.

Segregate Duties: Implement a system of internal controls that segregates duties

related to GST compliance. This reduces the risk of errors and fraud by ensuring that

no single individual has too much control over the process.

REFERENCE

https://www.gst.gov.in/

https://cleartax.in/s/gst-law-goods-and-services-tax

30

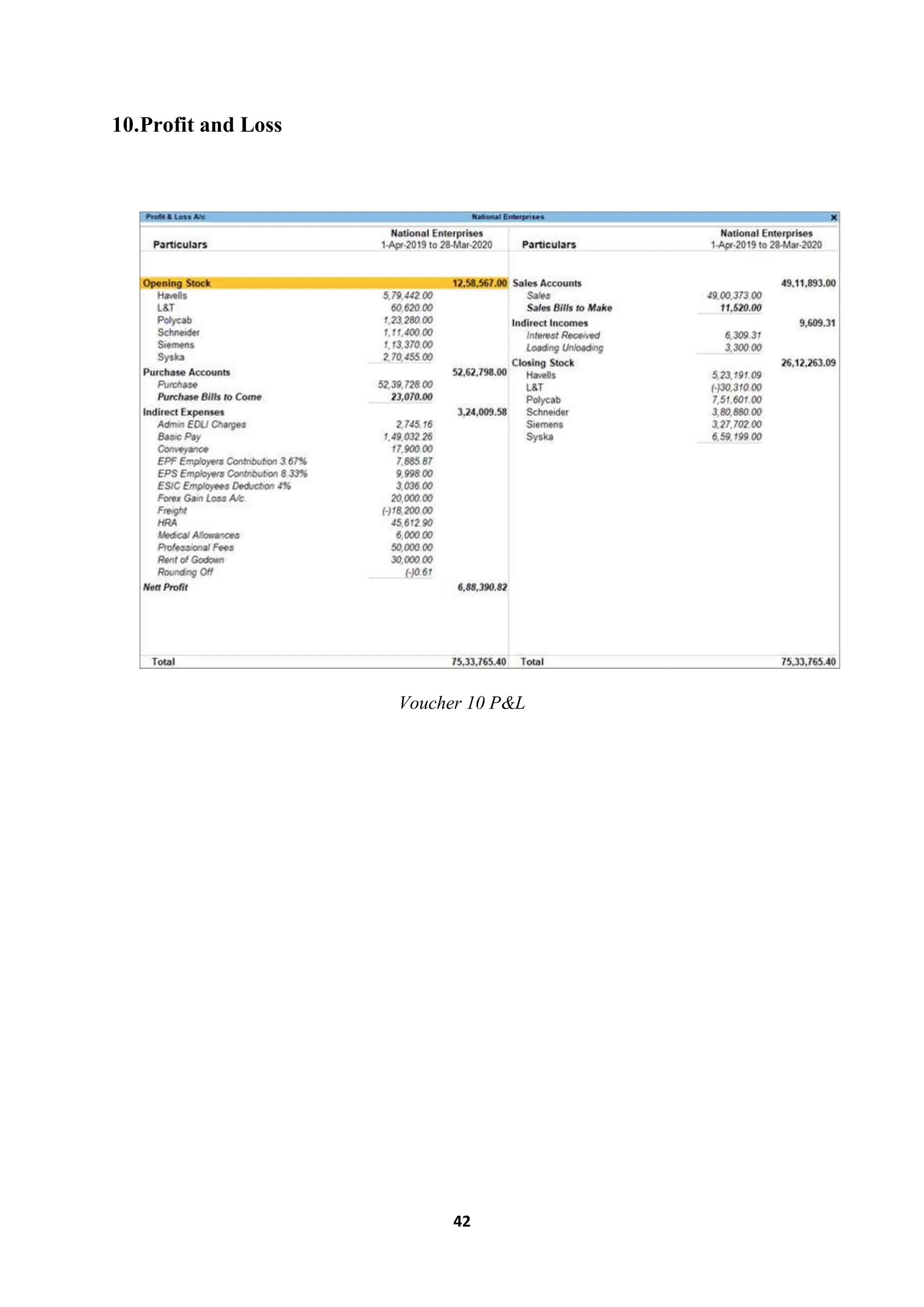

Accounting software TallyPrime

INTRODUCTION

Tally Prime is a robust and versatile business management software designed for

small and medium-sized enterprises (SMEs). It offers a comprehensive suite of

features to streamline various aspects of business operations, including

accounting, inventory management, taxation, payroll, and more. Tally Prime is

intended to simplify complex business processes, allowing users to focus on

business growth. In this context, this research explores the core features and usage

of Tally Prime.

Core Features of Tally Prime

Invoicing & Accounting: Tally Prime simplifies the creation and recording

of invoices with optimized invoice components, multiple billing modes, and

customizable configurations. It adapts to the specific needs of businesses,

making accounting straightforward.

Inventory Management: Tally Prime offers flexible inventory management

with features such as godown management, multiple stock valuation

methods, batch and expiry date tracking, and job costing. The powerful

inventory reports simplify the management of stock.

Insightful Business Reports: Tally Prime provides access to over 400

business reports with valuable insights for informed decision-making. Users

can customize and analyze these reports to suit their business needs.

GST/ Taxation: Users can generate GST-compliant invoices, including tax

invoices and bills of supply, and accurately file GST returns. Tally Prime

also supports the automatic generation of e-invoices and printing with IRN

and QR codes. It helps manage TDS, TCS, and statutory payroll

requirements like PF, ESI, and employee income tax.

Credit and Cash Flow Management: Tally Prime enhances efficiency in

accounts receivable, accounts payable, and inventory management,

optimizing cash flows. Insightful reports assist in monitoring cash flow.

31.

31

Multi-task Capabilities:Tally Prime supports multi-tasking, allowing users

to handle interruptions efficiently. For example, users can switch between

tasks like creating a sales invoice and recording new sales seamlessly.

Go To Feature: The "Go To" feature in Tally Prime simplifies the discovery

of insights and new capabilities. Users can search and find specific functions

within Tally Prime to enhance business operations.

Banking: Tally Prime offers a range of banking features, including auto

bank reconciliation, pre-defined cheque formats, cheque management, and

e-payments, simplifying banking tasks.

Access Business Data Online: Users can access business reports online via

a web browser from anywhere, ensuring that crucial data is always

accessible.

Secure Data: Tally Prime prioritizes data security with multiple user access

controls and feature-based security levels. This ensures that data access is

restricted according to user preferences.

How to use Tally Prime

For the use of Tally prime, following steps must be followed

1. Create a company

2. Enable GST features

3. Ledger creation

Below discuss the details:

1. How to create GST?

a) Go to Gateway of Tally prime > Alt + F3 > Create Company

b) Enter the basic information, i.e., name, mailing name and address of the

company,currency symbol etc.

c) In the ‘maintain field’, select Accounts Only or Accounts with Inventory as

per thecompany requirements.

32.

32

d) In theFinancial Year from, the first day of the current financial year for e.g.,

01-04-2023 will be displayed by default, which can be changed as per

requirement.

e) Enter the Tally prime Vault Password if required.

f) Press Enter to accept and save.

Figure 1 Create company

2. Enabling GST FEATURES

a. Go to Gateway of Tally > F11 Features > F3 Statutory & Taxation

b. In the screen you will find following options

c. Enable goods and service tax (GST) Yes, Set/alter GST Details -Yes.

This will display another screen where you can set GST details of the

company suchas the state in which company is registered, registration type,

GSTIN number etc.

Press Y or Enter to accept and save.

33.

33

3. LEDGER CREATION

Aftercreating a company and activating GST features, you need to create ledgers that

will enable you to pass accounting entries in Tally.

Here are the following steps:

Go to Gateway of Tally > Accounts Info > Ledgers > Create-

Enter the Name for the ledger want to create such as purchase, sales, receive etc.

Select the appropriate group to which such ledger belongs for example state

tax underduties and taxes group.

Enter the other related information required and press Y or Enter to accept and save.

After having done the above 3 steps, you can start entering accounting entries in Tally.

For this, Go to Gateway of Tally >Accounting Vouchers. There are many Accounting

Vouchers in Tally such as Payment, Receipt, Contra, Sales, Purchase, etc. Choose the

relevant Voucher and start passing the accounting entries.

Figure 2 Ledger creation

34.

34

Types of Vouchers

Belowis the voucher, books & register of Tally software

1. Receipt VoucherTo Receipt voucher records all receipt in to Bank or Cash

Accounts. Suchas receipt from debtors, any income refund of loan or advance, sales

of fixed assets etc.

Go to Gateway to Tally Accounting Voucher Click on F6

Receipt button presentation the button panel to have the Receipt Voucher Creation

Screen.

Voucher 1 Receipt Voucher

35.

35

2. Payment Voucher Payment Vouchers records all the payments made through

Bank & Cash. It is also used forpayment of fixed assets, purchase, loan & advance

etc.

Go to Gateway to Tally Accounting Voucher Click on F5

Payment buttonpresentation the button panel to have the Payment Voucher Creation

Screen.

Voucher 2 Payment Voucher

36.

36

3. Journal VoucherJournalvoucher is for adjustment between any two ledgers.

Go to Gateway to Tally Accounting Voucher Click on F7

Journal buttonpresentation the button panel to have the Journal Voucher Creation

Screen.

Voucher 3 Journal voucher

37.

37

4. Sales Voucher

Goto Gateway to Tally Accounting Voucher Click on F8 Click on V(As

Invoice) Sales Invoice Creation Screen.

Voucher 4 Sales invoice

38.

38

5. Sales Voucher

Goto Gateway to Tally Accounting Voucher Click on F8 Click on V(As Voucher)

Sales Voucher Creation Screen.

Voucher 5 Sales Voucher

39.

39

6. Purchase Invoice

Goto Gateway to TallyAccounting Voucher Click on F9 Click on V(As Invoice)

Purchase Invoice Creation Screen.

Voucher 6 Purchase Invoice

40.

40

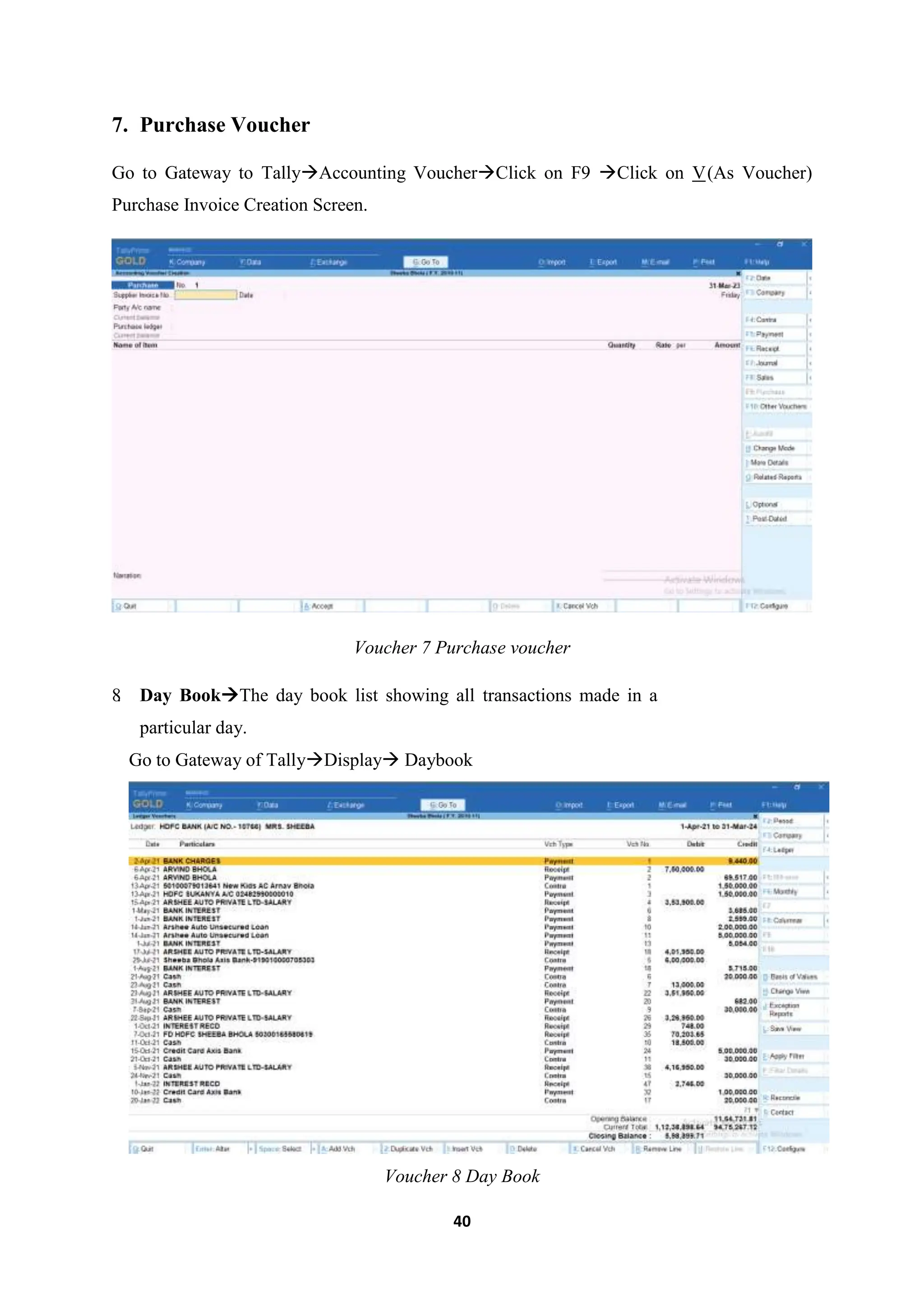

7. Purchase Voucher

Goto Gateway to TallyAccounting VoucherClick on F9 Click on V(As Voucher)

Purchase Invoice Creation Screen.

Voucher 7 Purchase voucher

8

. Day BookThe day book list showing all transactions made in a

particular day.

Go to Gateway of TallyDisplay Daybook

Voucher 8 Day Book

41.

41

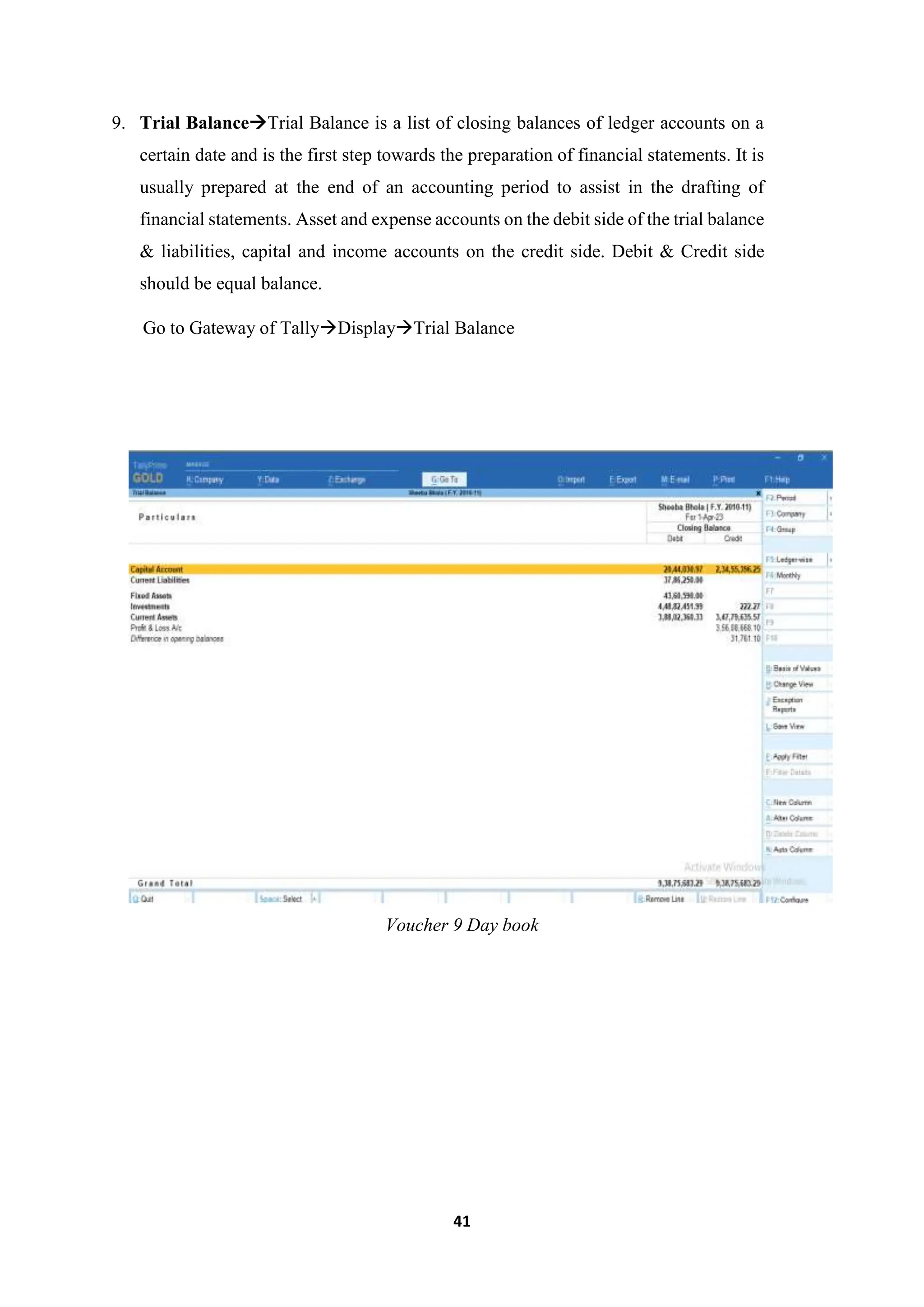

9. Trial BalanceTrialBalance is a list of closing balances of ledger accounts on a

certain date and is the first step towards the preparation of financial statements. It is

usually prepared at the end of an accounting period to assist in the drafting of

financial statements. Asset and expense accounts on the debit side of the trial balance

& liabilities, capital and income accounts on the credit side. Debit & Credit side

should be equal balance.

Go to Gateway of TallyDisplayTrial Balance

Voucher 9 Day book

43

Research Methodology

This researchis like an adventurous journey where we want to find out how Tally is really used

in the real world. We're not looking for specific answers, but we're exploring different

possibilities.

To do this, we're using two different tools. First, we have a descriptive tool, which is like

taking a good look at Tally's features and how it works. It's like examining all the parts of a

puzzle to understand the big picture. Second, we use an analytical tool, which is like thinking

XYZply about how Tally affects the real world. It's like figuring out why Tally is important in

practical situations.

We also use two types of information. One is about how people feel and what they think about

Tally, which is like listening to their stories. The other is about the numbers and data that show

us the real impact of Tally.

By combining all of these methods, we hope to uncover the many ways Tally is used and why

it matters in real life.

Data Collection: Data collection for this research is primarily based on secondary

materials to ensure a comprehensive understanding of Tally's applications and

conceptuality. The following sources have been used:

Journals and Articles: Scholarly journals and articles provide in-depth insights

into Tally's features, best practices, and real-world applications.

Newspapers: Newspaper articles offer valuable information on current trends

and actual uses of Tally in various industries and sectors.

Internet Content: Information from online sources, such as blogs, forums, and

websites, provides diverse viewpoints, case studies, and user experiences with

Tally.

Research Papers: Academic research papers contribute insights into the

technical aspects of Tally and its influence on businesses and accounting

practices.

Feedback from Manufacturers and Businessmen: Interviews and surveys with

manufacturers and businessmen who use Tally in their daily operations provide

first-hand accounts of its practical applications and effectiveness.

44.

44

Objectives of theStudy

To understand the conceptuality of Tally.

To understand the use of Tally in the real world.

o To Understand the Conceptuality of Tally: This research aims to develop into the

core conceptuality of Tally, including its technical features and functionalities.

o To Understand the Real-World Applications of Tally: The study explores how Tally

is practically used in various industries and sectors.

Limitations of the Study

This research primarily relies on secondary data sources and employs an exploratory research

design. The limitations include:

The dependence on existing data may limit the ability to gather customized and up-to-

date information.

The descriptive design may not provide an exhaustive understanding of Tally's

applications, as it is focused on gaining insights into its conceptuality and practical

applications.

45.

45

FINDINGS AND ANALYSIS

Inour research, we found that Tally has numerous real-world applications, making it a valuable

tool for accountants and businesses alike. Below are some of the key findings and their

analysis:

Accurate Financial Records: One of the key findings of this research is that Tally is

widely used to maintain accurate financial records. It assists businesses in efficiently

tracking income and expenses. Accountants can record transactions, reconcile accounts,

and generate financial reports. This accuracy supports better decision-making and

financial planning.

Analysis: Maintaining accurate financial records is essential for businesses of all sizes.

Tally streamlines this process, reducing errors and ensuring that financial data is readily

available for decision-makers.

Simplified Accounting Processes: Tally simplifies complex accounting processes. Its

user-friendly interface and features like ledger management, invoicing, and taxation

tools make it an indispensable tool for accountants. It automates many accounting tasks,

reducing errors and saving time.

Analysis: Tally's user-friendly interface and automation features contribute to more

efficient accounting processes. This can lead to increased productivity and reduced

errors in financial management.

Real-Time Data Access: Tally provides real-time access to financial data, which is

crucial for making informed decisions. Businesses can monitor their financial

performance as it happens, identify trends, and react promptly to changes. This real-

time access enhances the agility and responsiveness of organizations.

Analysis: Real-time data access is a competitive advantage in the fast-paced business

world. Tally's ability to provide this access is a significant asset for organizations

looking to stay agile and make data-driven decisions.

46.

46

GST Compliance:With the introduction of Goods and Services Tax (GST) in various

countries, Tally has become an essential tool for GST compliance. It simplifies GST

return filing, eases input tax credit reconciliation, and ensures that businesses comply

with tax regulations.

Analysis: GST compliance is a legal requirement in many regions. Tally's ability to

streamline this process not only ensures compliance but also reduces the administrative

burden on businesses.

Customization and Scalability: Tally is known for its flexibility and scalability. It can

be customized to suit the specific needs of different industries and business sizes. This

adaptability is one of the reasons for its widespread use across various sectors.

Analysis: The ability to customize and scale Tally to meet specific business needs is a

significant advantage. This flexibility allows businesses to adapt the software to their

unique requirements.

47.

47

Conclusion

In conclusion, thisresearch provides compelling evidence of Tally's versatility and practical

applications in the real world. It serves as a valuable tool for accountants and businesses,

helping them maintain accurate financial records, simplify accounting processes, ensure GST

compliance, and access real-time financial data. While this study couldn't develop XYZply into

all of Tally's features due to time constraints, it lays a solid foundation for understanding the

conceptuality and significance of Tally in the business world.

Furthermore, the findings of this research offer valuable insights for businesses, accountants,

and policymakers seeking to enhance financial management and compliance. The study

highlights the importance of Tally's role in maintaining accurate records, streamlining

accounting processes, and staying up to date with tax regulations. Future research can explore

additional features and applications of Tally in even greater detail, providing a more nuanced

understanding of its impact on businesses and the broader economy. Tally's adaptability and

utility make it an indispensable asset in the world of accounting and finance.

48.

48

RECOMMENDATIONS

Stay Updated:Regularly keep up with the latest GST rules and regulations to ensure

you're aware of any changes that may affect your compliance.

Check Supplier Details: Always verify your suppliers' GST numbers and invoices to

avoid any discrepancies in your records.

Use Technology: Leverage technology and GST software to automate calculations and

filings, reducing the chances of manual errors.

Timely Filing: File your GST returns on time to avoid penalties and interest charges.

Set up reminders to ensure you meet deadlines.

Record-Keeping: Maintain organized records of all GST-related documents, making

it easier to reconcile and verify data.

Cross-Check Documents: Cross-reference your invoices, receipts, and purchase

orders to ensure they match and are consistent.

Audit Internally: Regularly conduct internal audits to spot and rectify any issues in

your GST compliance process.

Open Communication: Foster open communication with your suppliers and

customers regarding GST matters to avoid misunderstandings.

Training Staff: Train your employees responsible for GST compliance, so they

understand their roles and responsibilities.

Use GSTIN Validation Tools: Utilize GSTIN validation tools to confirm the accuracy

of GST Identification Numbers, reducing the risk of errors.

Reference

https://tallysolutions.com/

https://en.wikipedia.org/wiki/Tally_Solutions