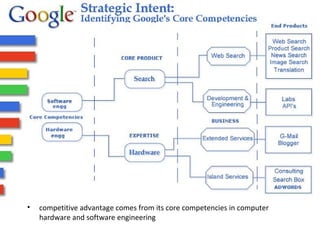

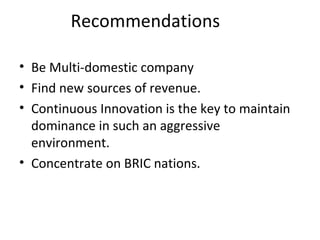

The document provides a strategic analysis of Google, outlining its vision and mission to organize the world's information and enhance user experience through innovation. It discusses Google's competitive landscape, major products, revenue models, and the impact of online advertising growth. Recommendations include diversifying revenue sources, maintaining focus on search innovation, and expanding in emerging markets.