Downloaded 28 times

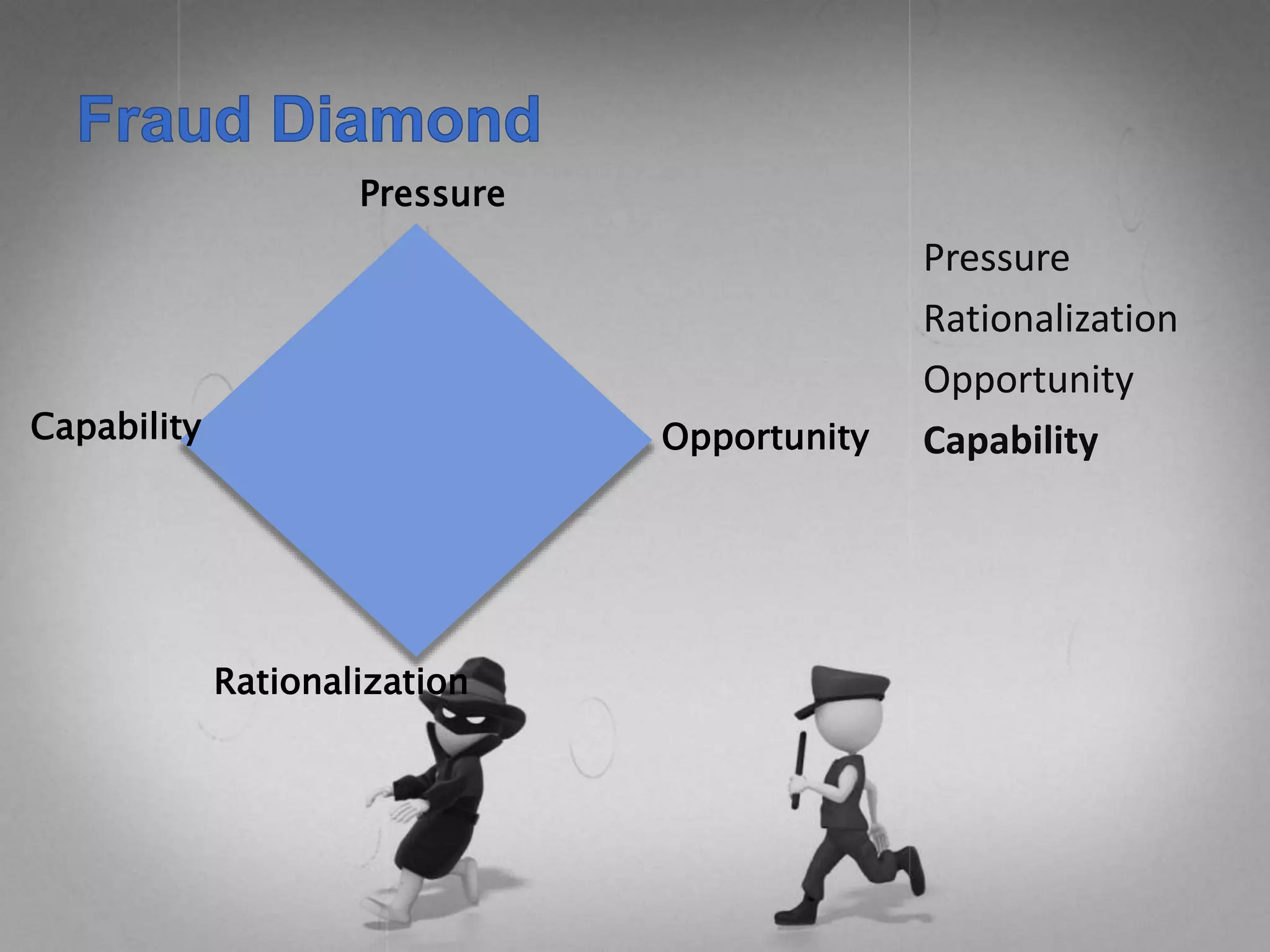

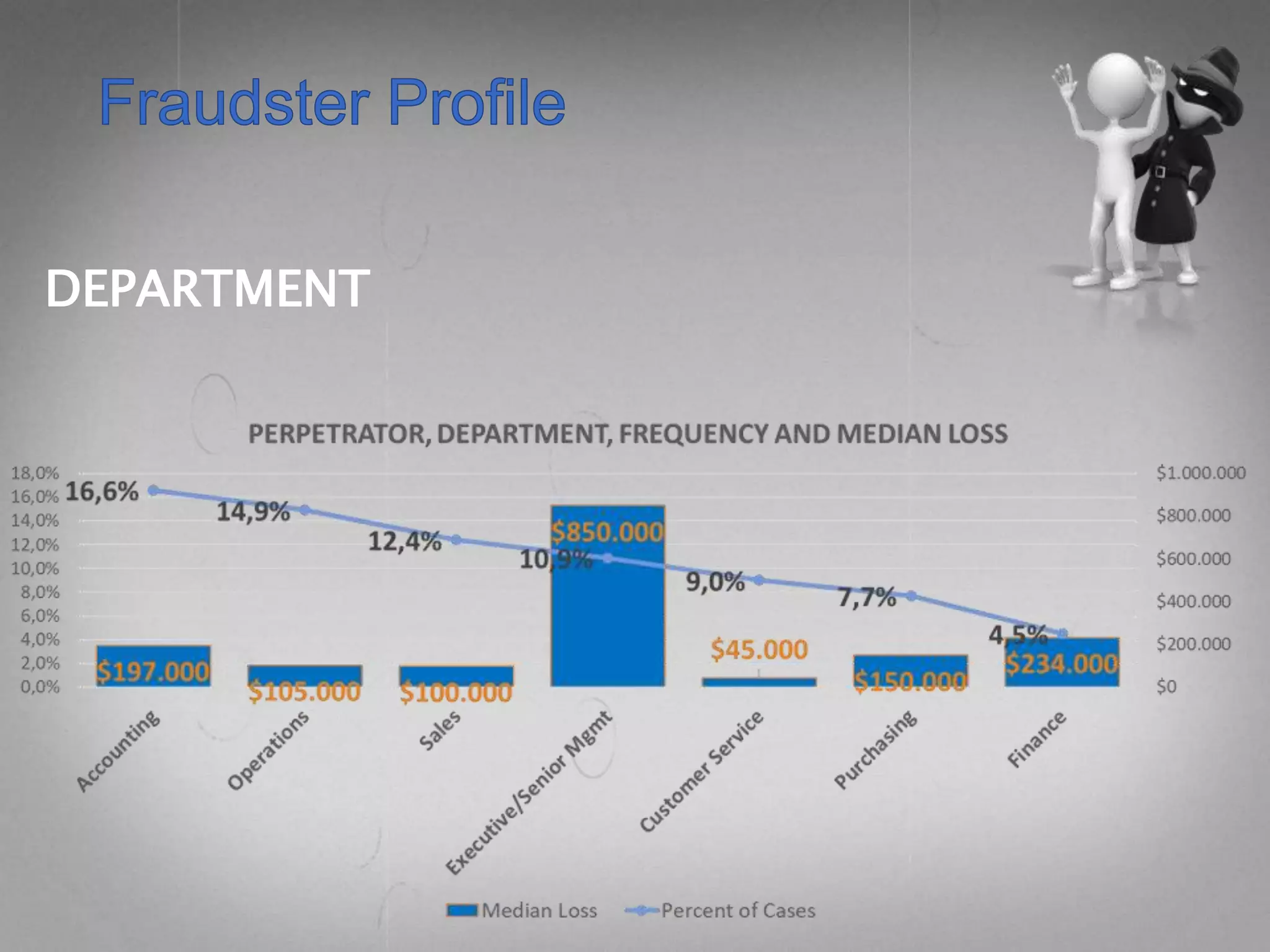

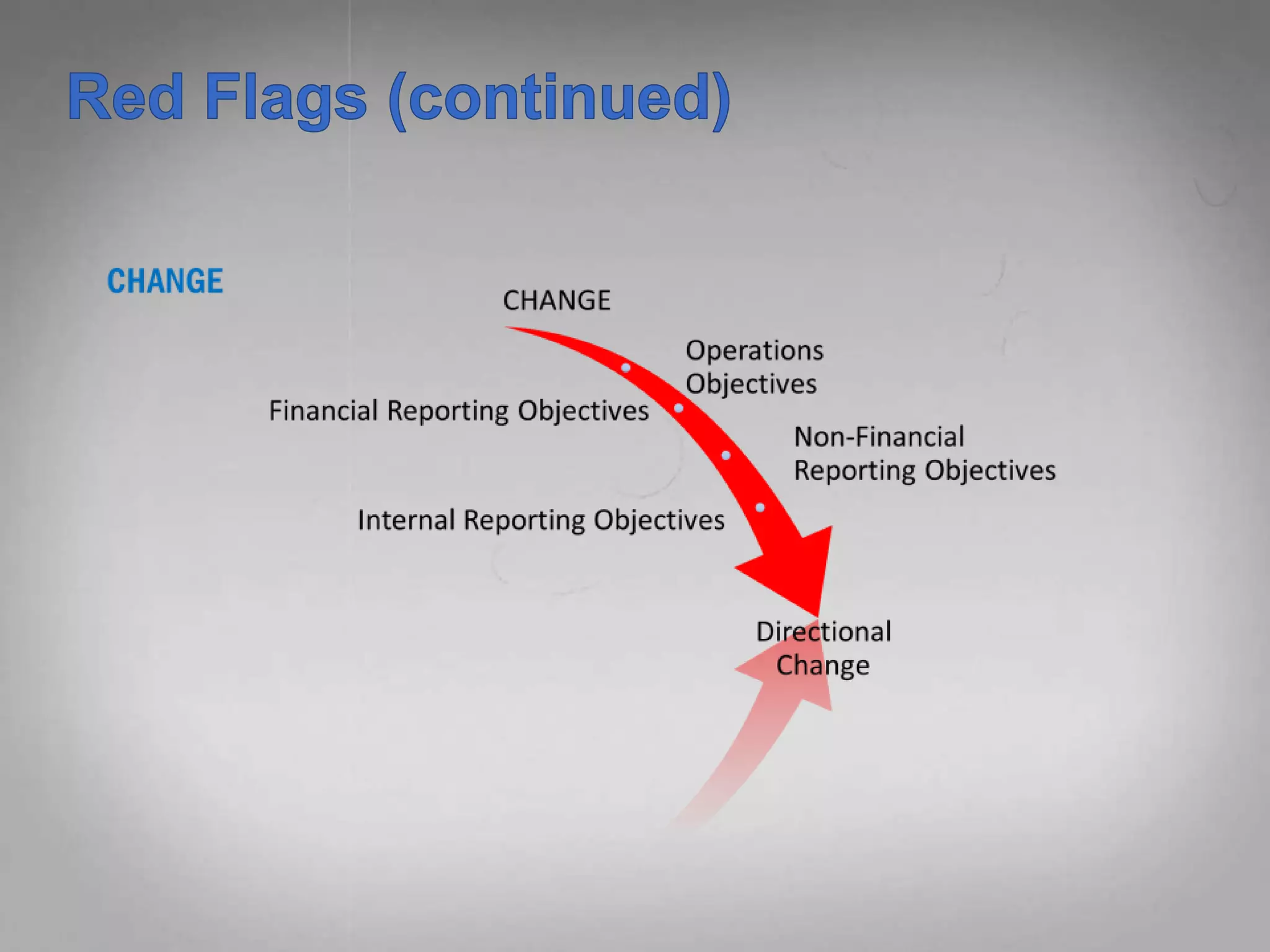

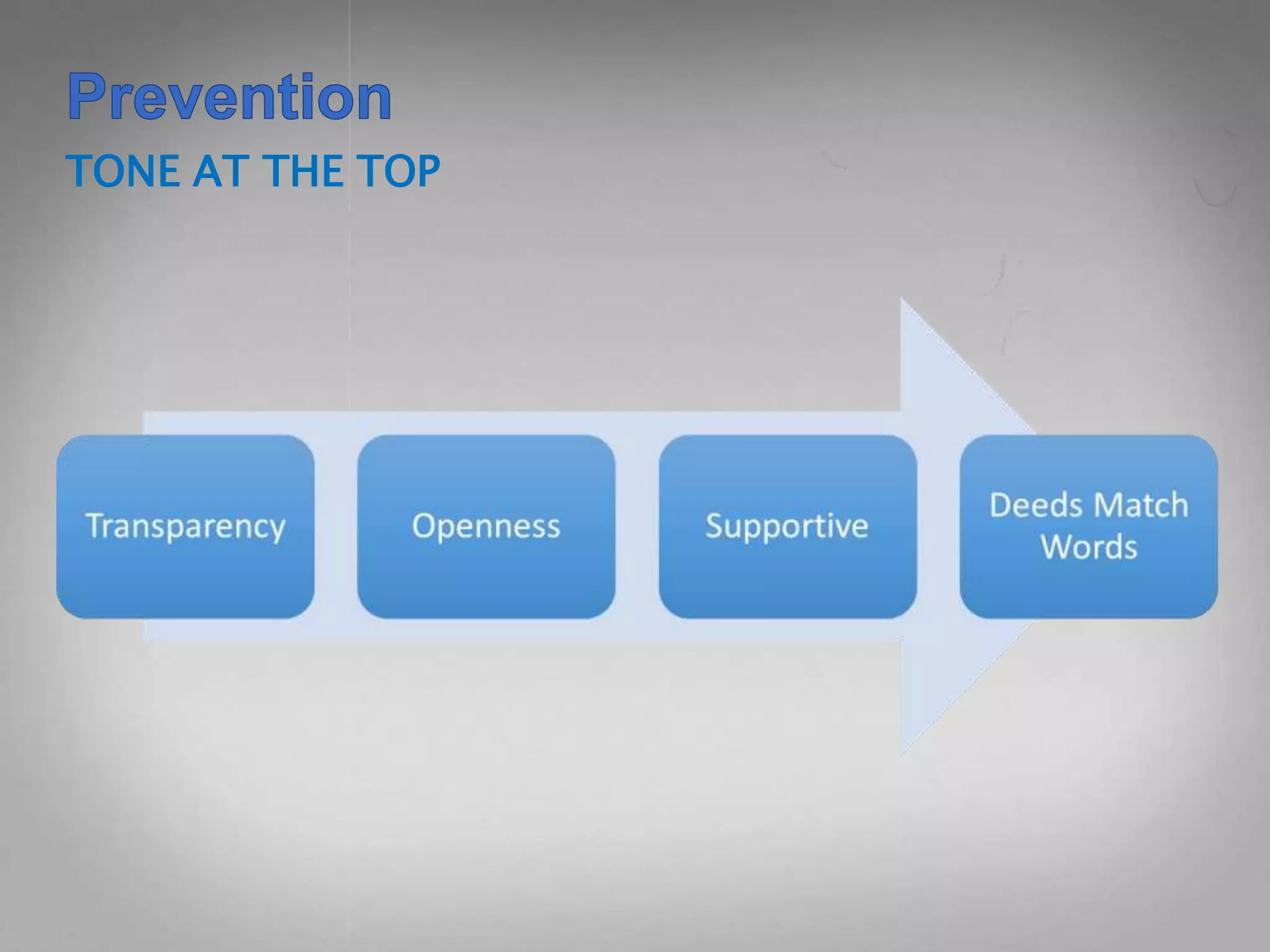

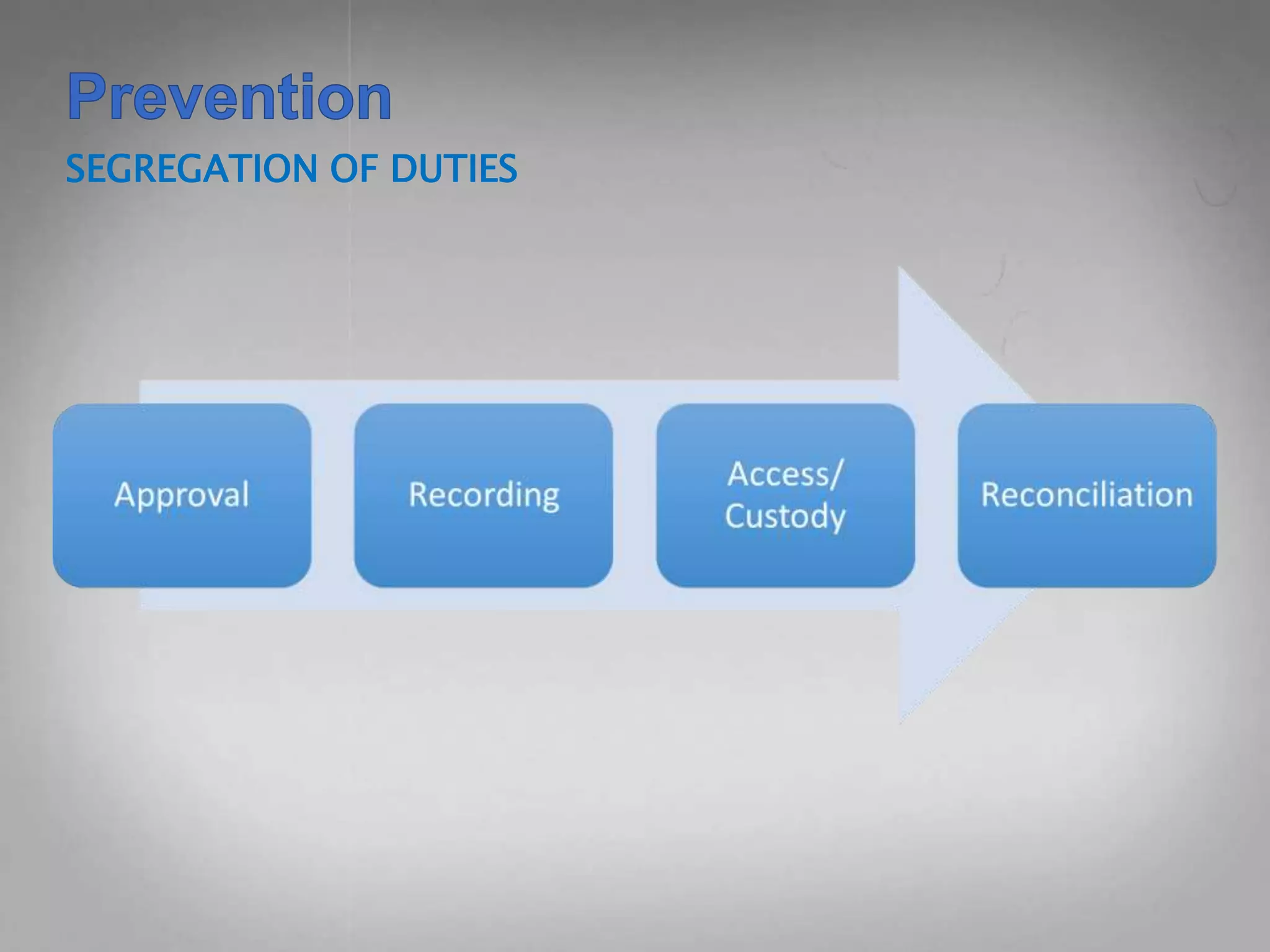

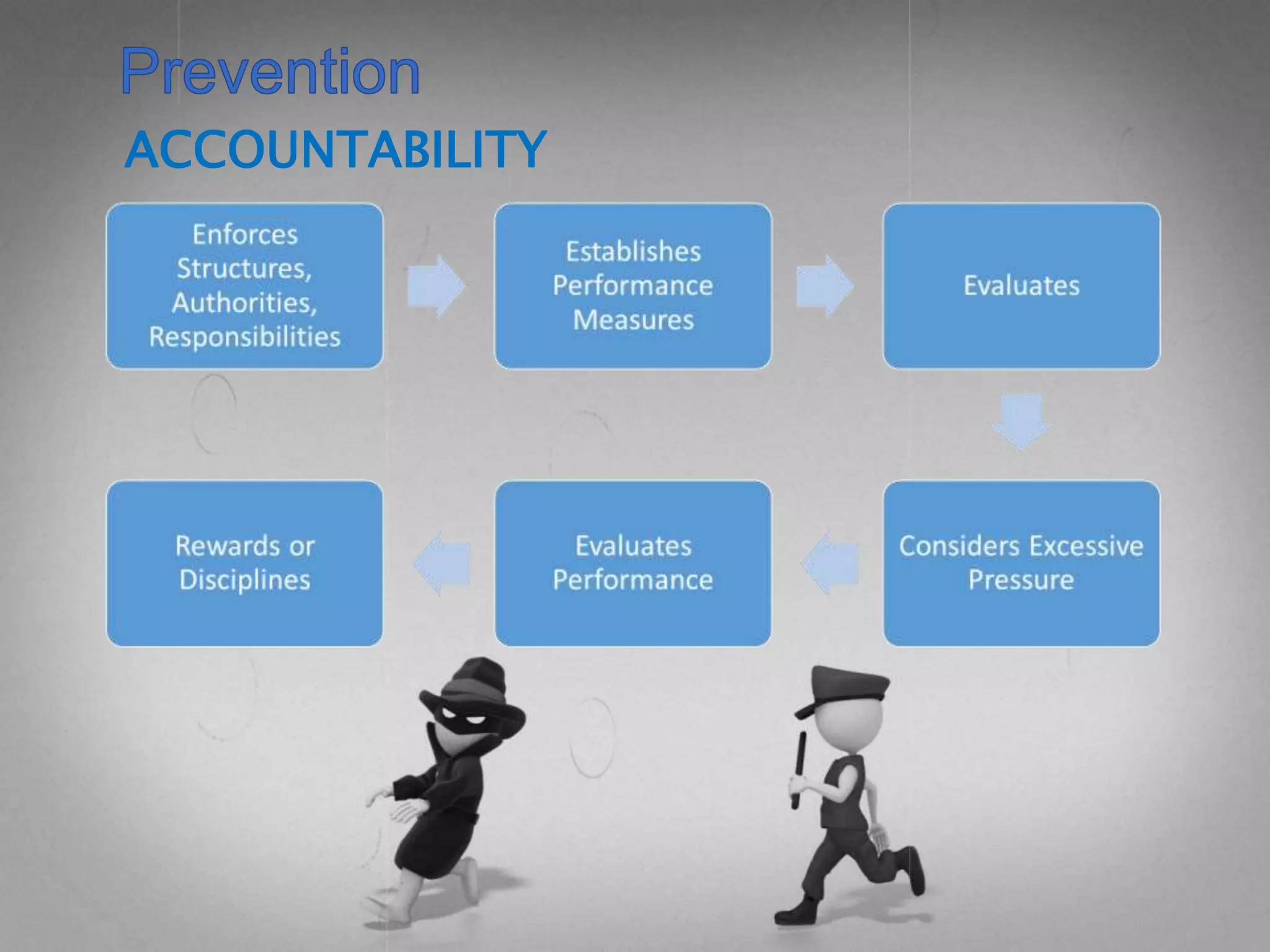

This document discusses fraud prevention. It identifies three types of fraudsters: those who always steal, never steal, and steal under perceived pressure. It then outlines the fraud triangle of pressure, opportunity, and rationalization. Several indicators of potential fraud are described, including lifestyle changes beyond one's means, certain personality traits, and behavioral changes like financial issues discussed at work. The document stresses establishing controls like segregating duties, implementing an escalation policy, and ensuring accountability and proper oversight to help prevent fraud.