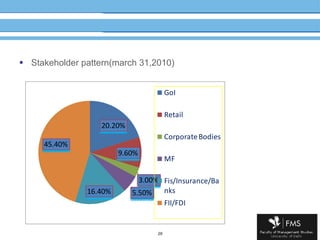

Downloaded 26 times

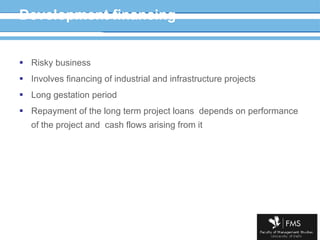

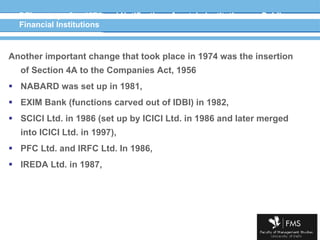

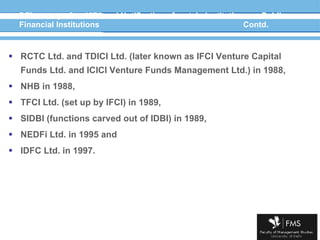

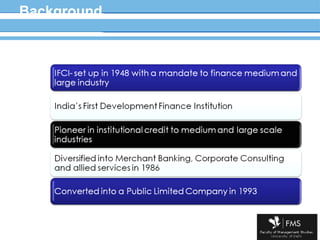

- Development Financial Institutions (DFIs) were established by governments to provide long-term financing for industrial and infrastructure projects due to the risky and long-gestation nature of such projects. - Over time, as financial systems became more sophisticated in risk management, banks and bond markets became better able to finance such projects, reducing the need for DFIs with government support. - In India, the first DFI was established in 1948 and many more were set up over the subsequent decades to promote development across various sectors, with some focused on long-term lending and others on refinancing.

![Working and functions_of_rbi[1]](https://cdn.slidesharecdn.com/ss_thumbnails/workingandfunctionsofrbi1-110522002449-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![Csac10[1].p](https://cdn.slidesharecdn.com/ss_thumbnails/csac101-p-110520054545-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![Csac08[1].p](https://cdn.slidesharecdn.com/ss_thumbnails/csac081-p-110520054521-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![Csac05[1].p](https://cdn.slidesharecdn.com/ss_thumbnails/csac051-p-110520054504-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![Csac14[1].p](https://cdn.slidesharecdn.com/ss_thumbnails/csac141-p-110520054443-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)

![Csac06[1].p](https://cdn.slidesharecdn.com/ss_thumbnails/csac061-p-110520054419-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![Csac05[1].p](https://cdn.slidesharecdn.com/ss_thumbnails/csac051-p-110520053904-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![Csac06[1].p](https://cdn.slidesharecdn.com/ss_thumbnails/csac061-p-110520053834-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![Csaa01[1].p](https://cdn.slidesharecdn.com/ss_thumbnails/csaa011-p-110520053804-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![Csac02[1].p](https://cdn.slidesharecdn.com/ss_thumbnails/csac021-p-110520053749-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)

![Csac16[1].p](https://cdn.slidesharecdn.com/ss_thumbnails/csac161-p-110520053725-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)

![Csac14[1].p](https://cdn.slidesharecdn.com/ss_thumbnails/csac141-p-110520053710-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![Csac06[1].p](https://cdn.slidesharecdn.com/ss_thumbnails/csac061-p-110520053659-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![Csac12[1].p](https://cdn.slidesharecdn.com/ss_thumbnails/csac121-p-110520053625-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)