Downloaded 283 times

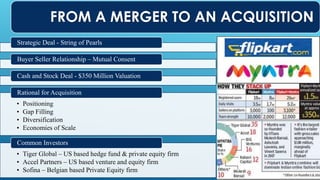

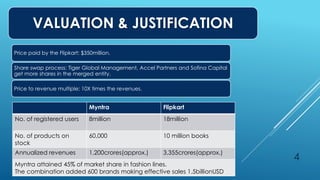

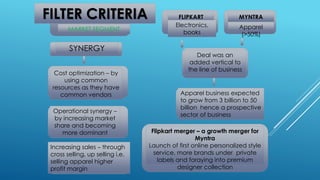

Tiger Global, Accel Partners, and Sofina Capital were common investors in Flipkart and Myntra. Flipkart acquired Myntra in a $350 million cash and stock deal in 2014. The acquisition provided strategic benefits like adding Myntra's apparel segment to Flipkart's electronics and books segments, and creating operational synergies through cost optimization and increased sales from cross-selling. Due diligence on the acquisition focused on profitability, integration costs and cultural fit to ensure synergies were realized. The acquisition was announced in January 2014 and closed in May 2014, with communication to customers, employees, and media emphasizing the complementary nature and strategic benefits of combining the two companies.