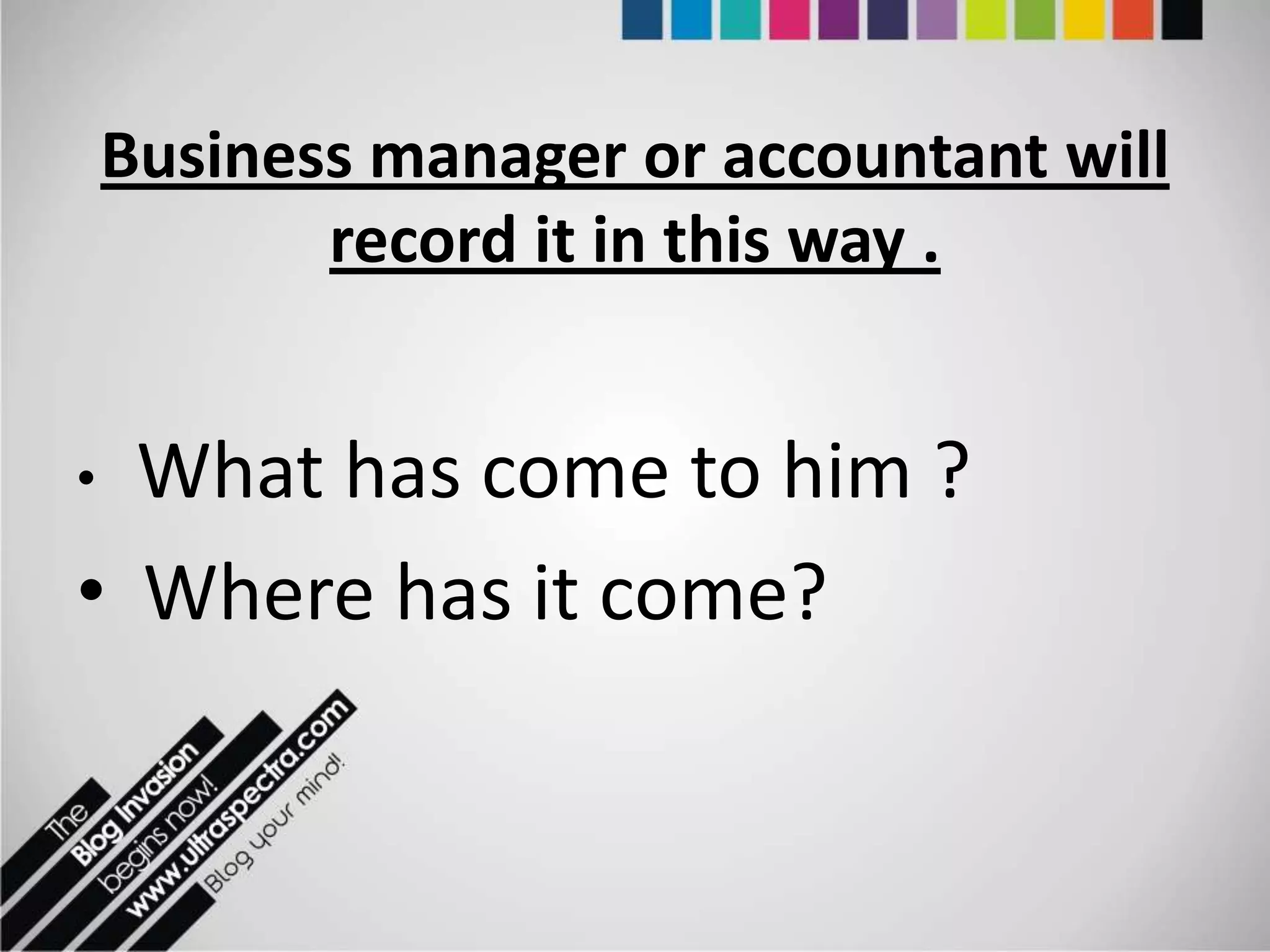

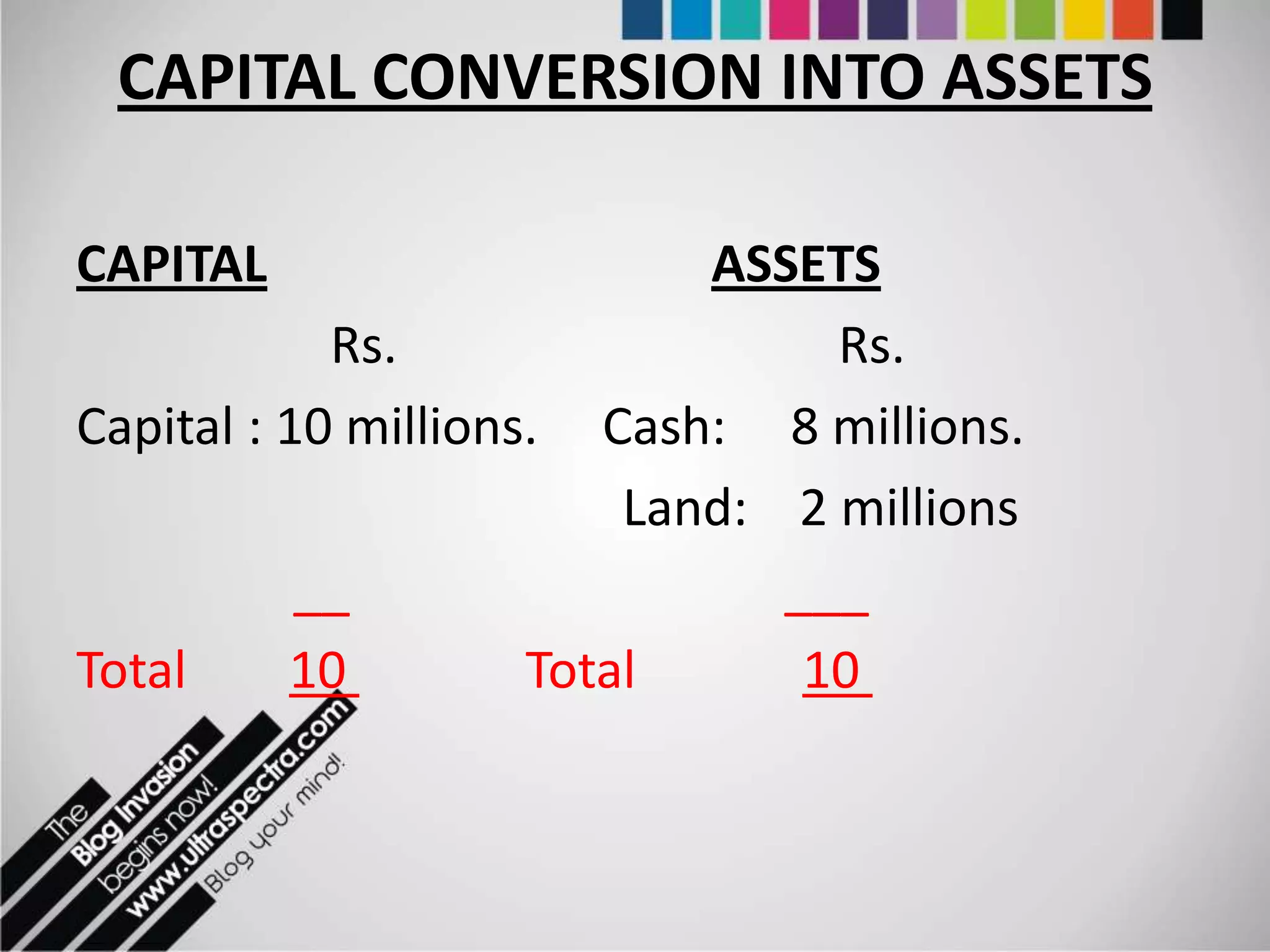

Capital or equity is the money an owner puts into a business to start operations. When the owner converts capital into assets like cash, land, buildings, or inventory to start a business activity, it is recorded through journal entries that debit the asset accounts and credit the capital/equity account. As the business operates, additional assets may be acquired through retained earnings or by taking on liabilities like loans which are recorded by debiting assets and crediting the liability accounts.

Overview of assets and liabilities, introducing key terms including assets, capital, and liabilities.

Defines assets as business conversions of money, highlighting cash as the primary asset. Lists various types of assets including land and machinery.

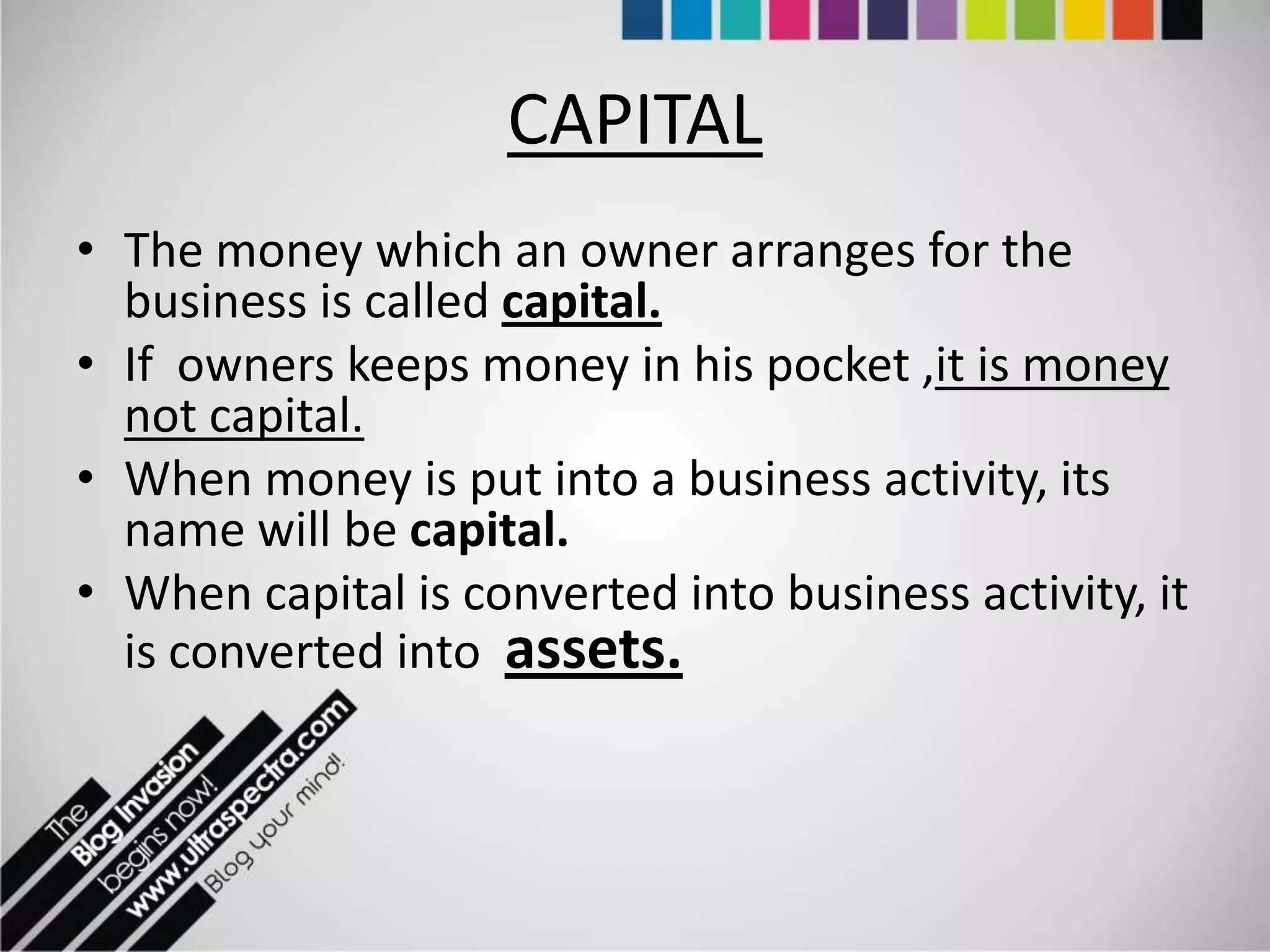

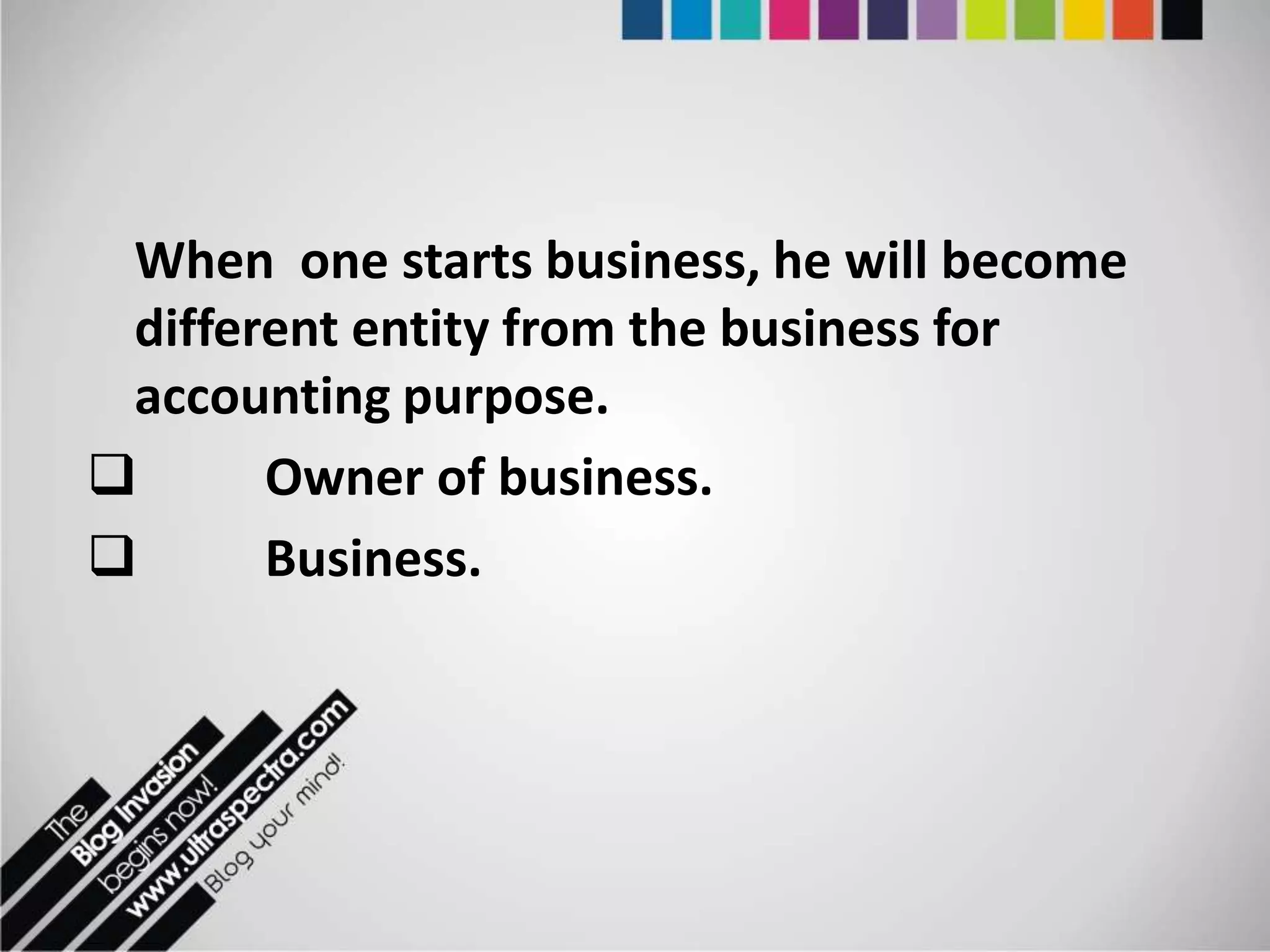

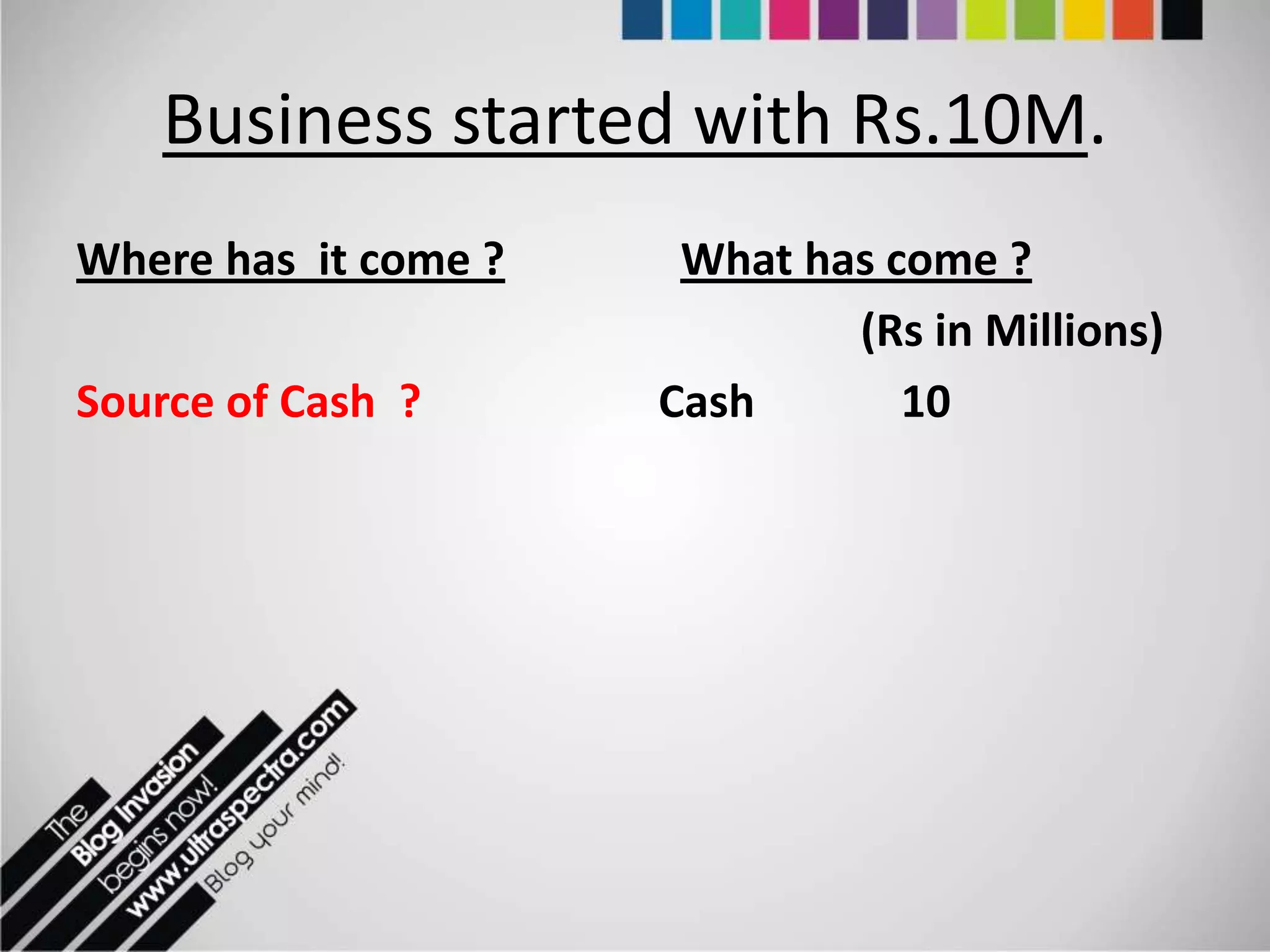

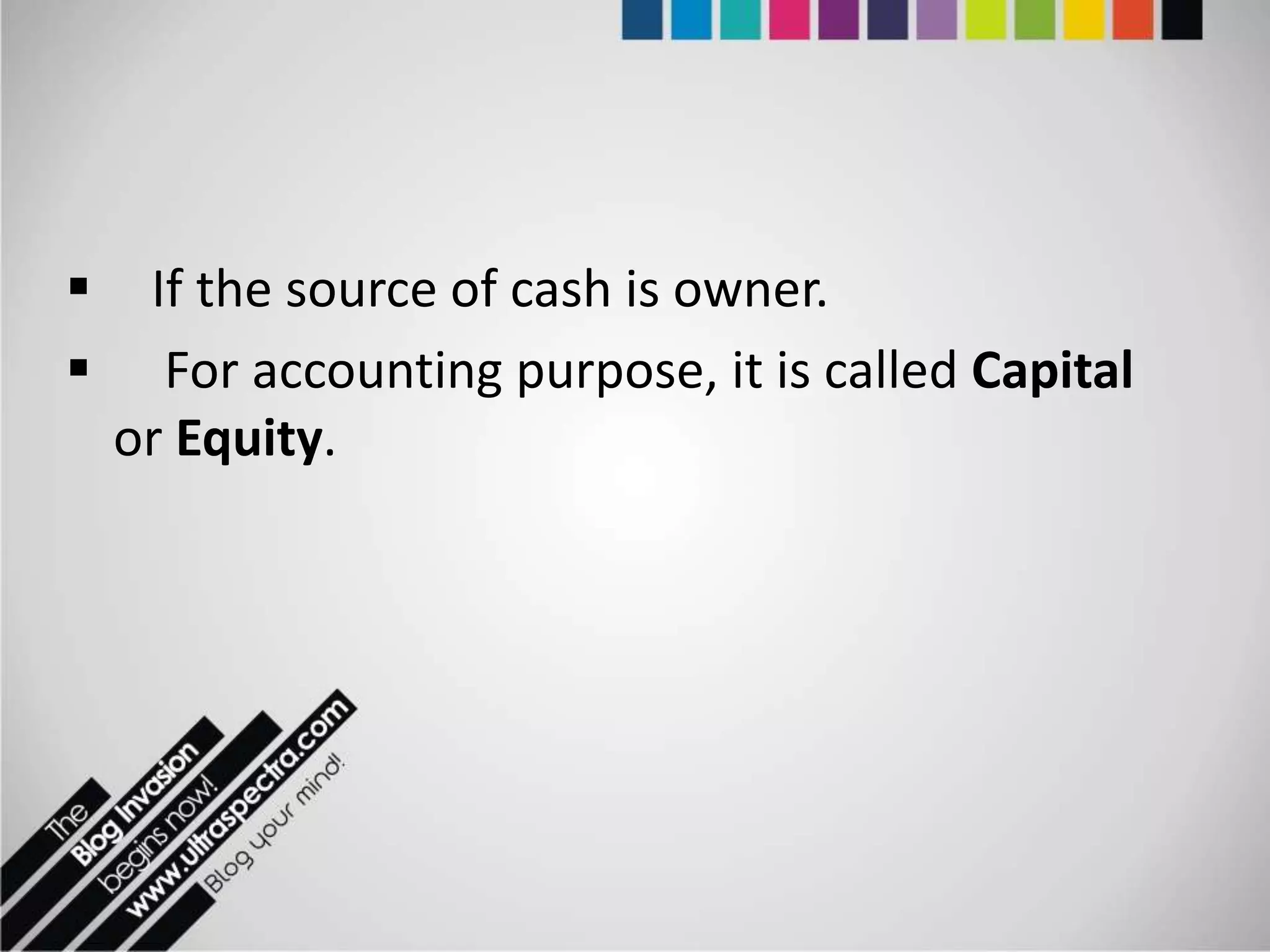

Explains capital as owner’s funds for business, distinguishing capital from money hoarding. Discusses accounting entries related to capital.

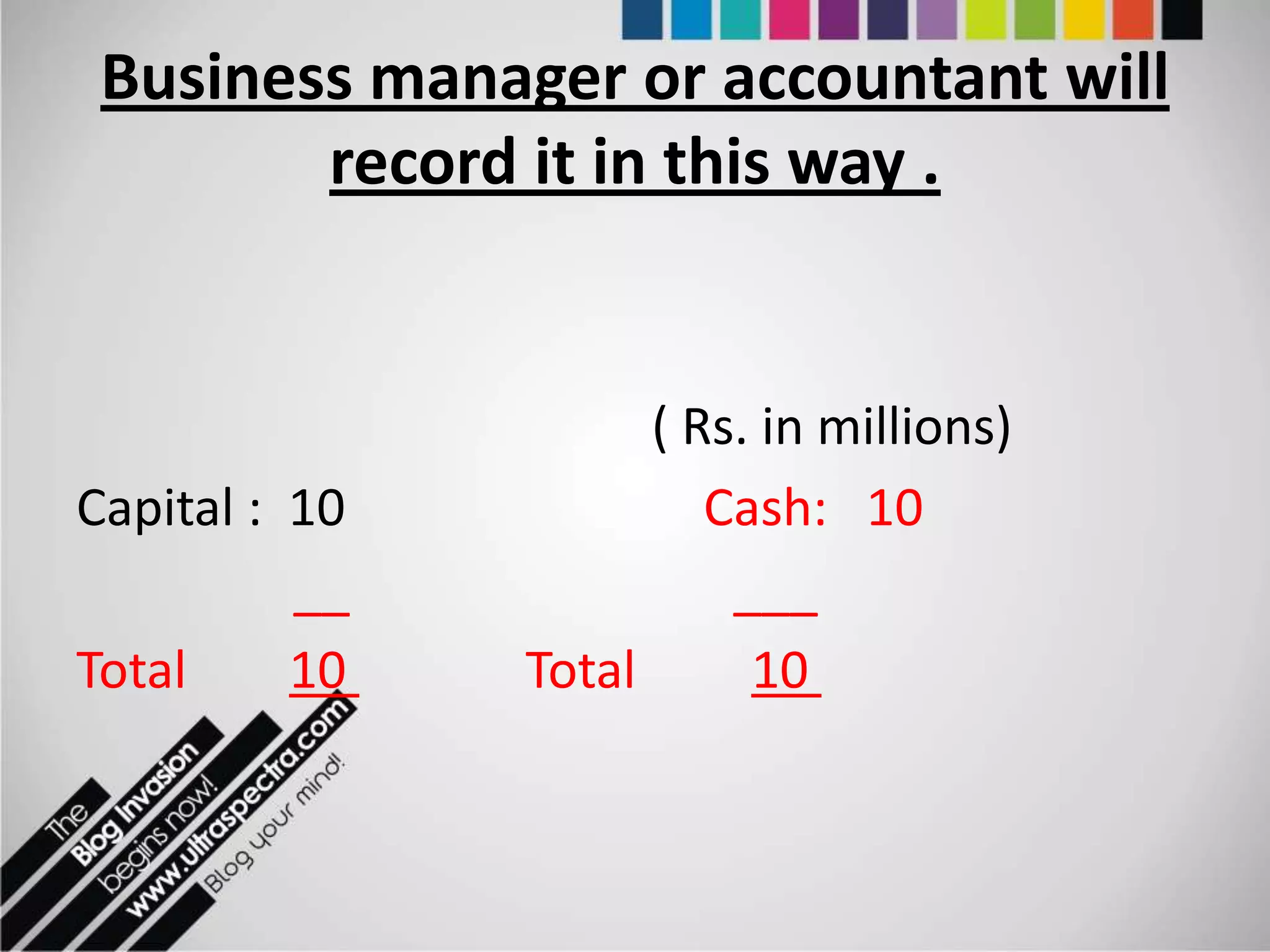

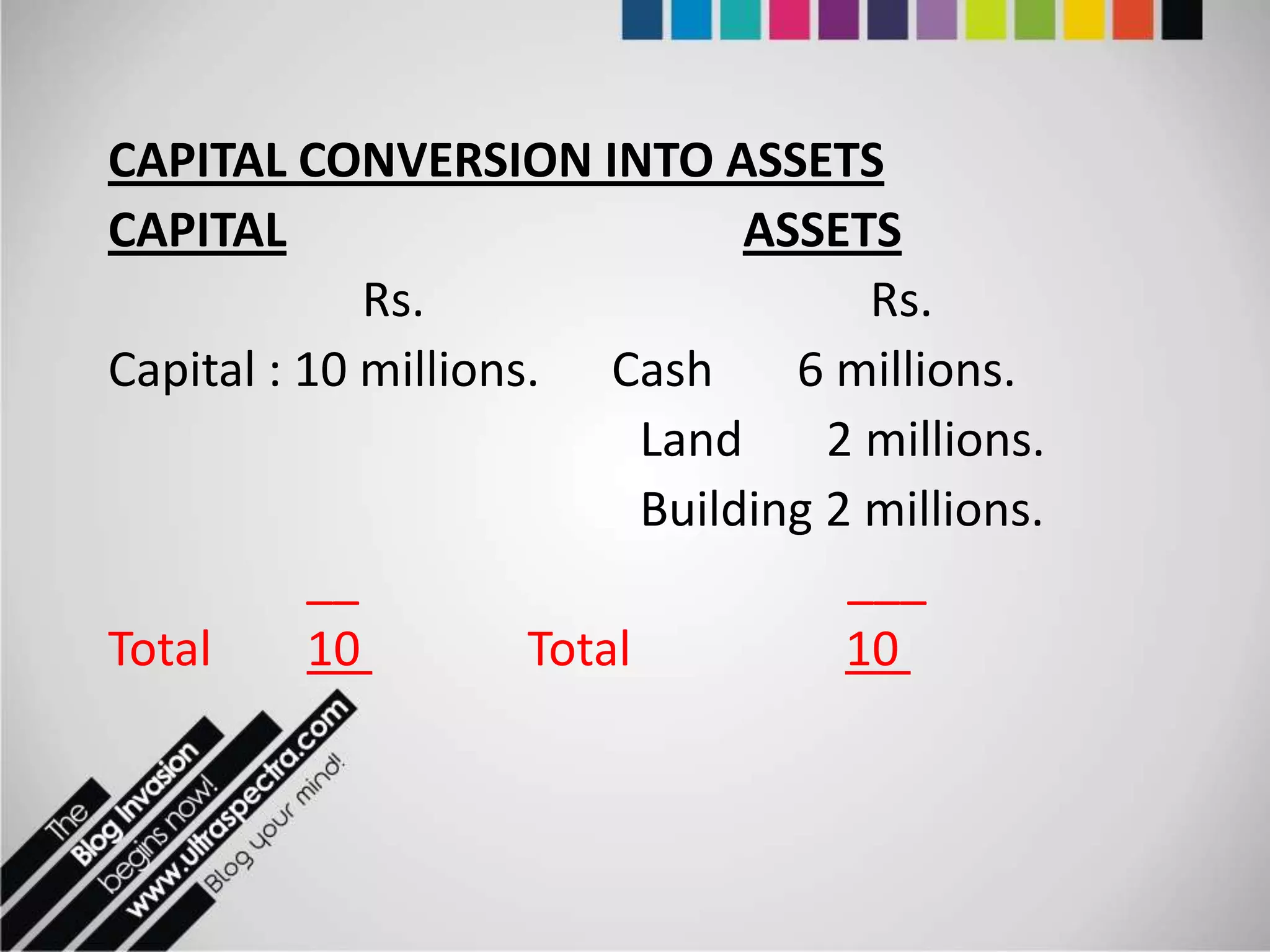

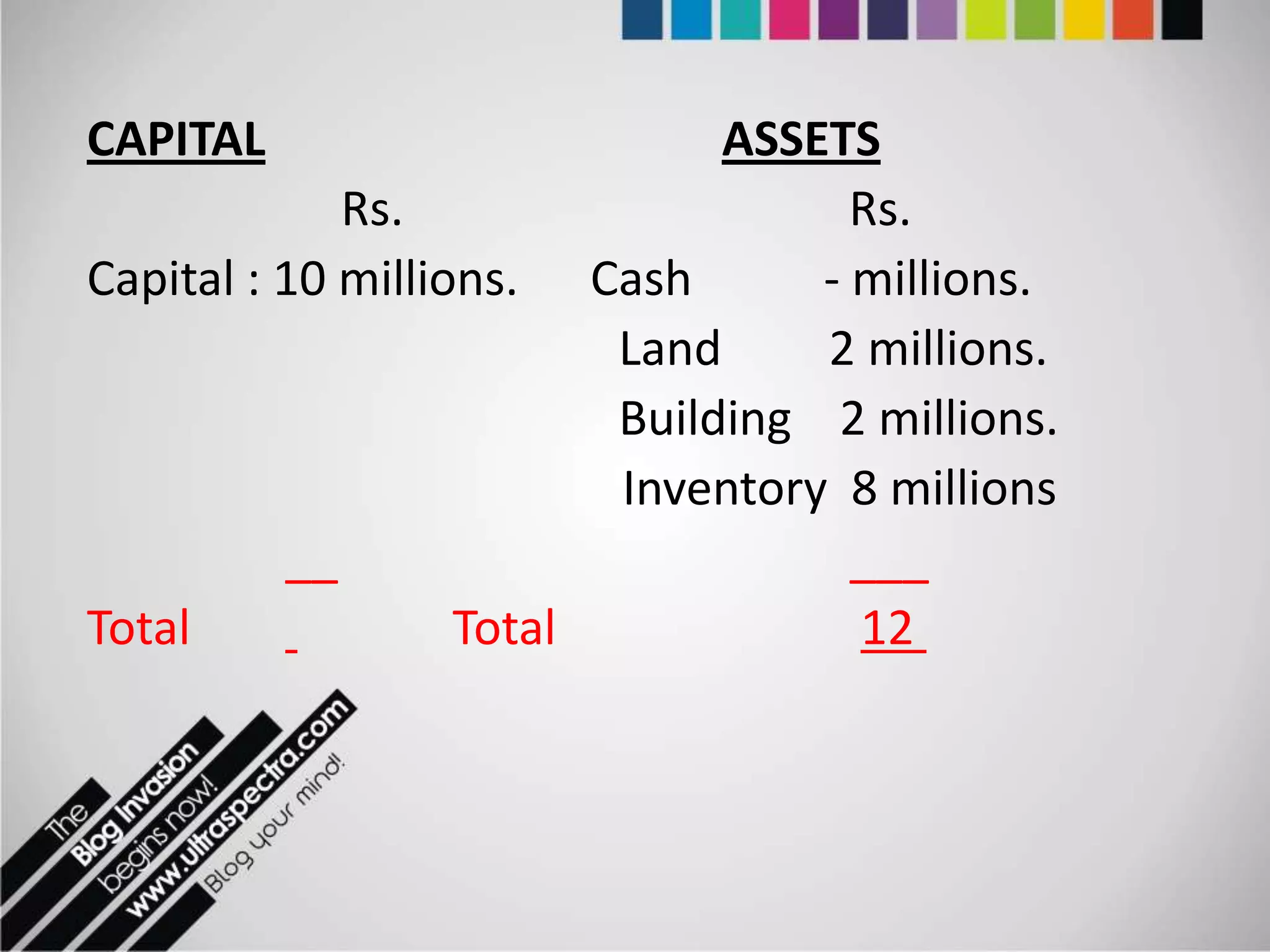

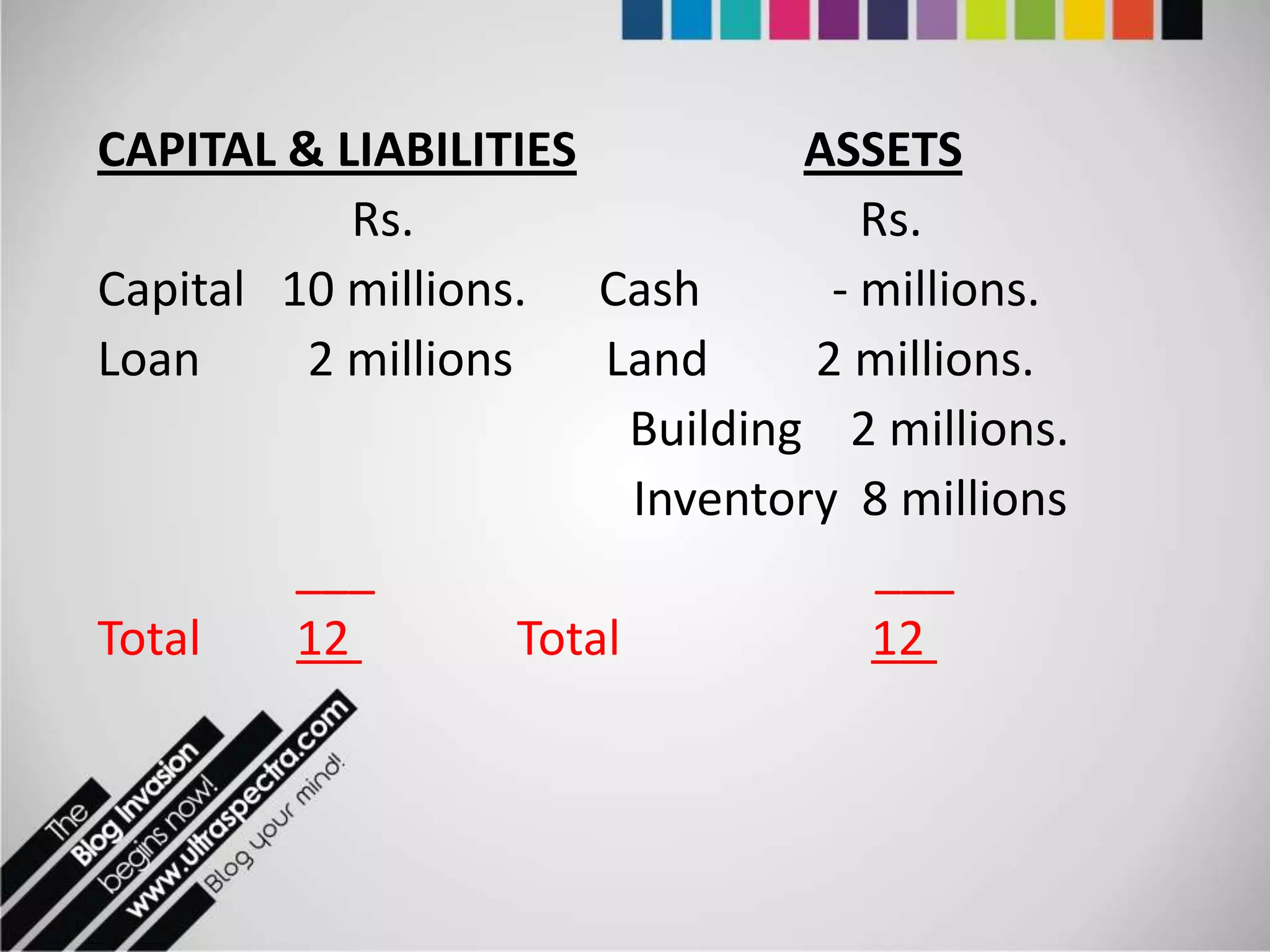

Demonstrates the accounting entries for business starting with Rs.10M, converting capital into assets, incorporating liabilities.

Classifies assets into fixed, current, tangible, and intangible. Describes each type with examples such as patents and goodwill.

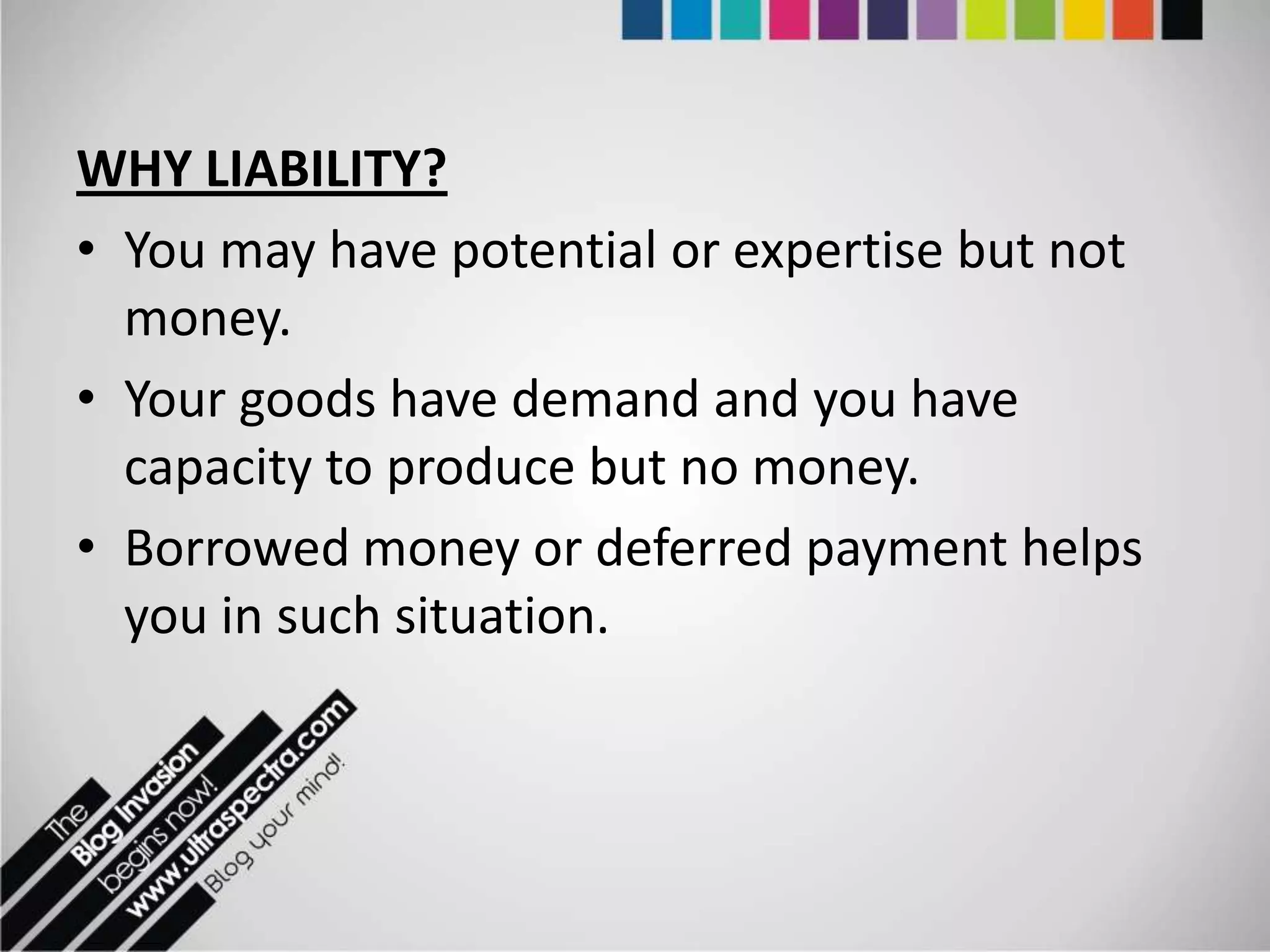

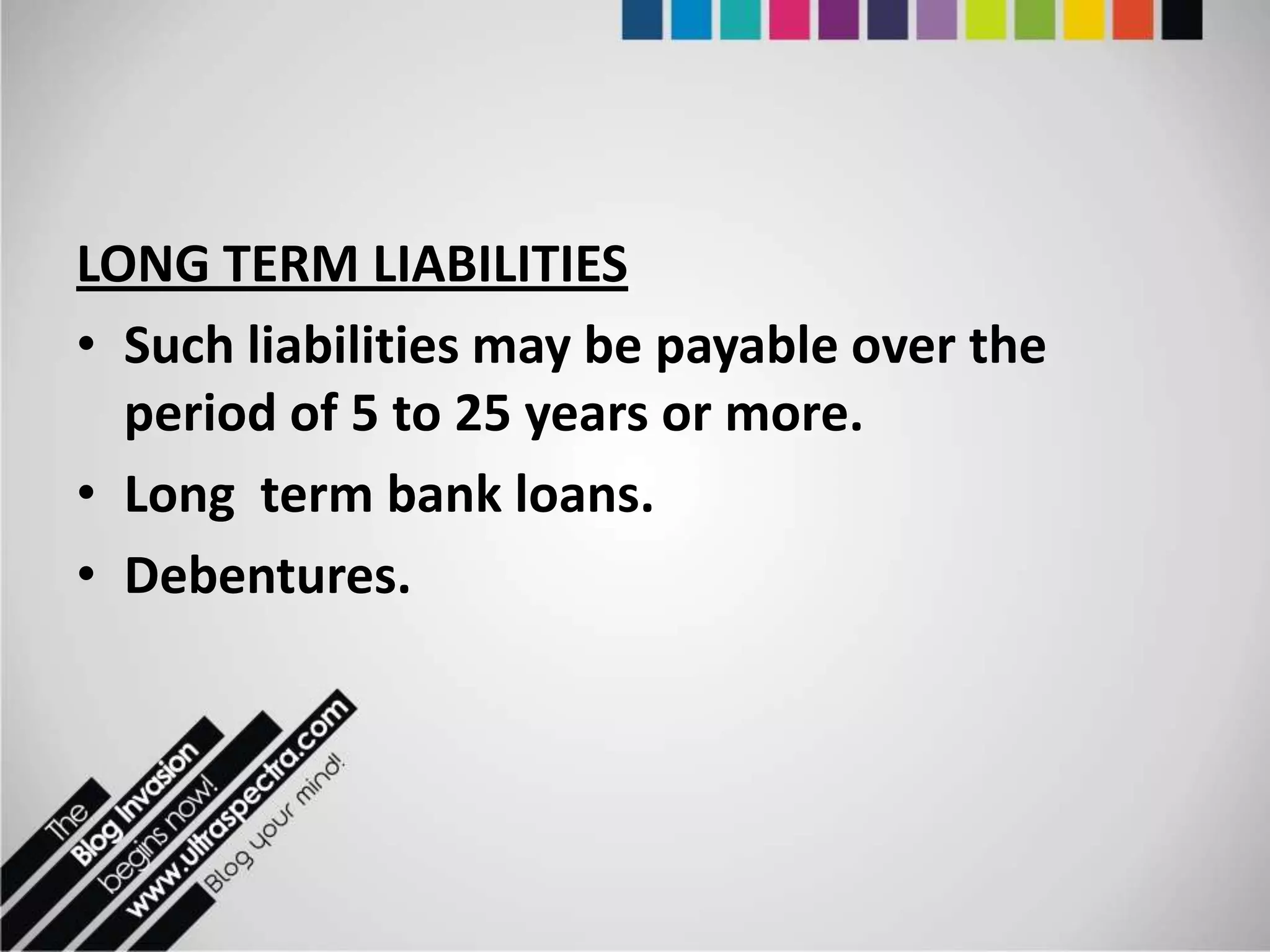

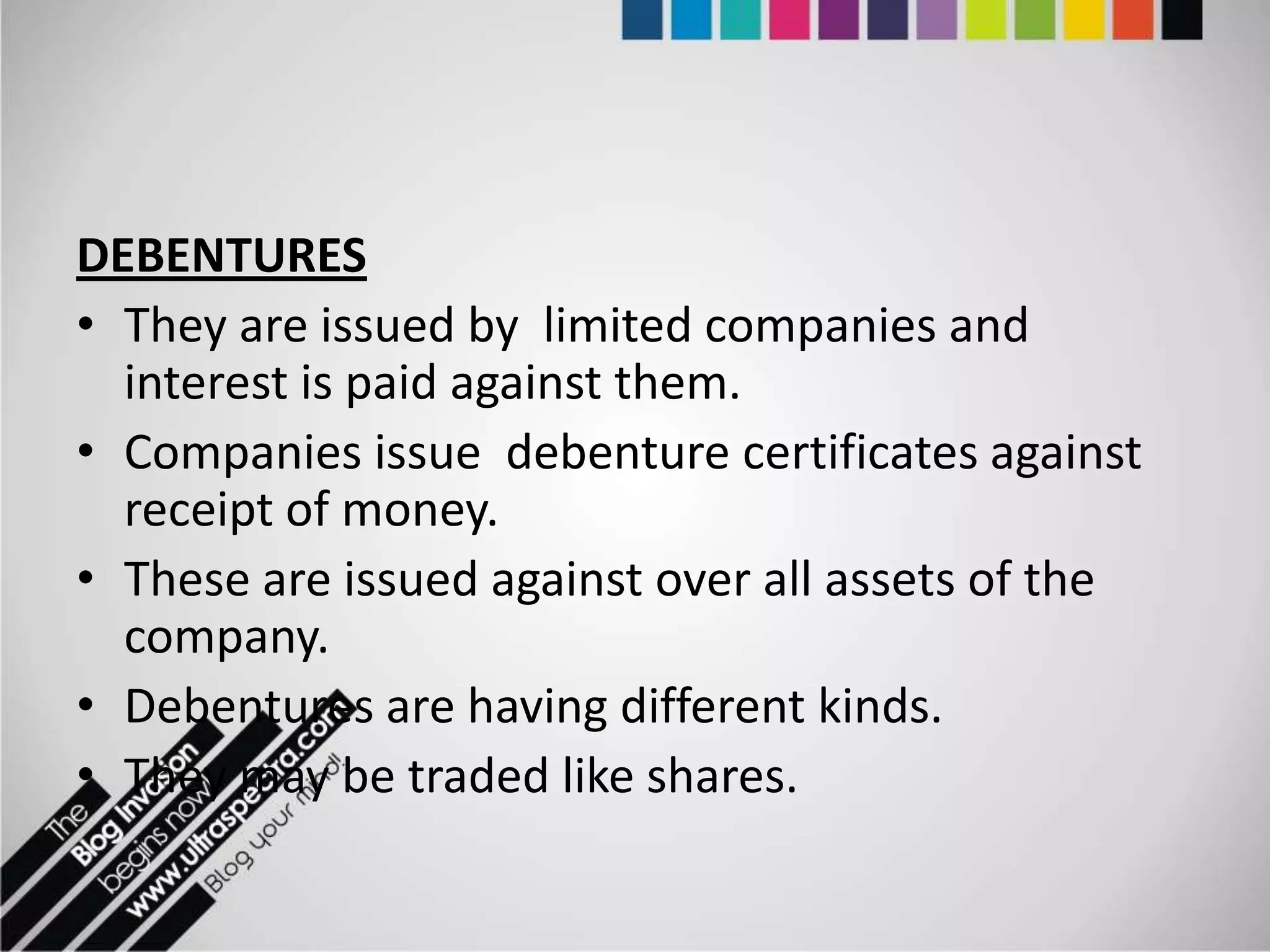

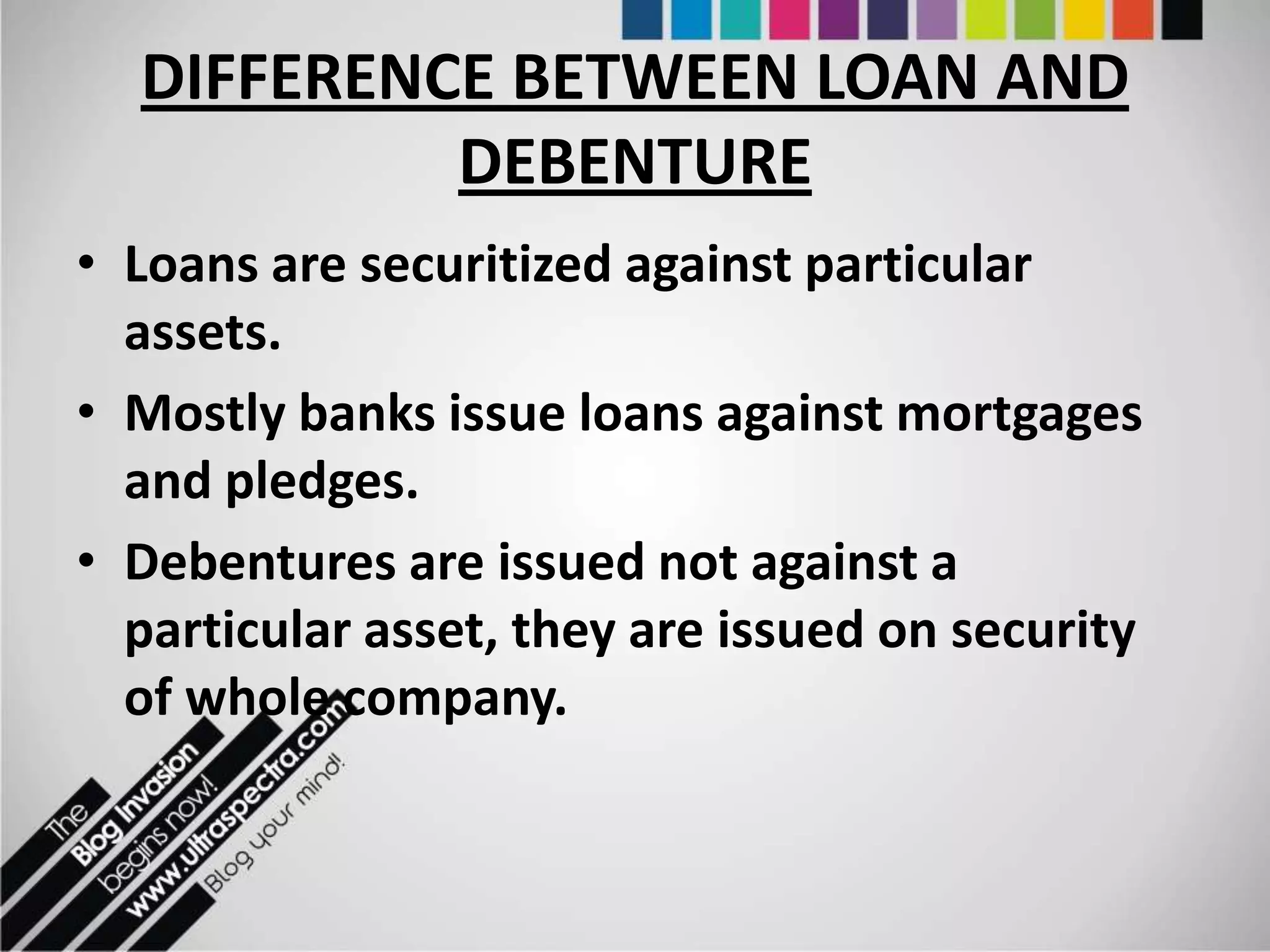

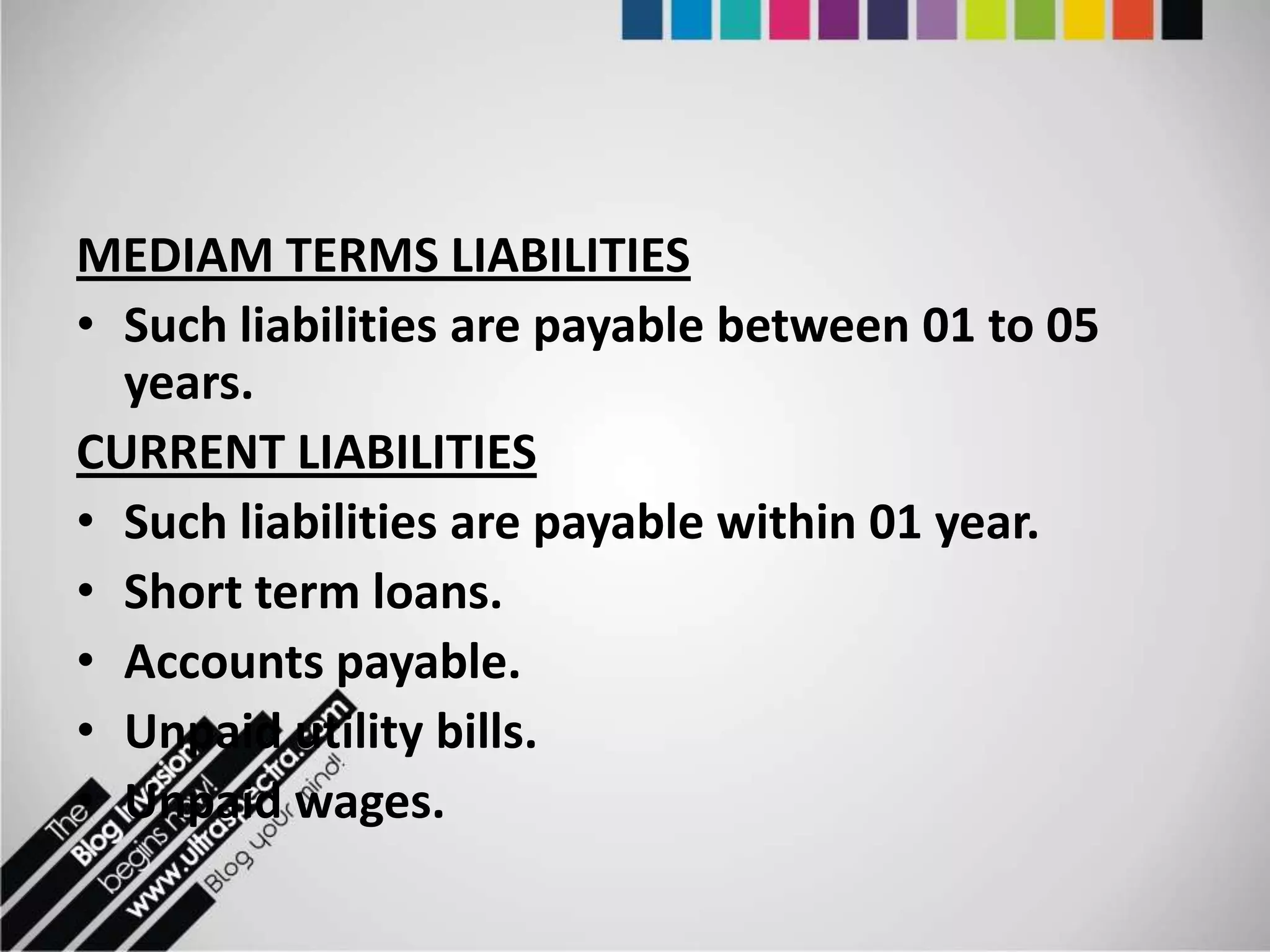

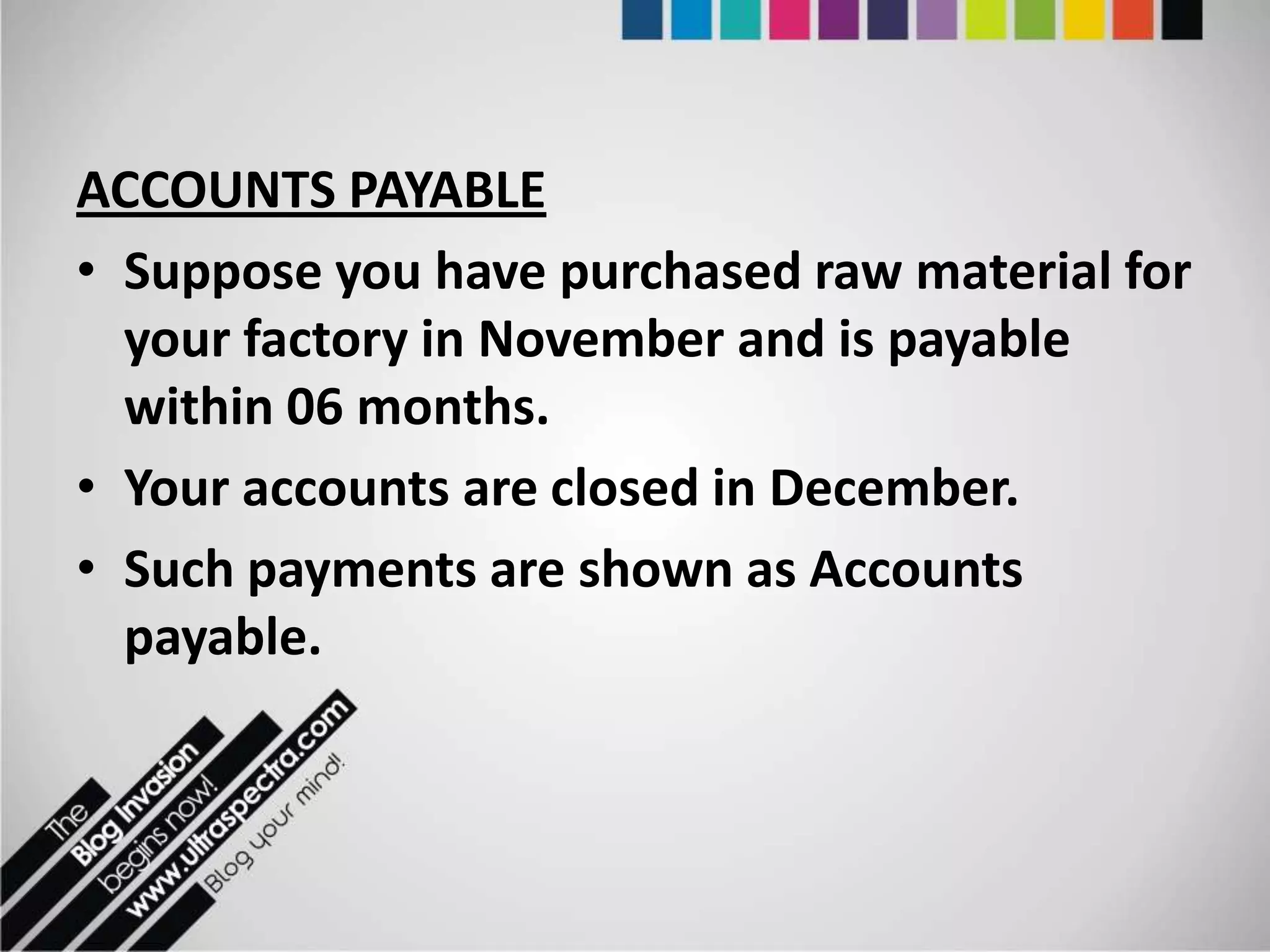

Explains liabilities, types including long-term, medium-term, and current liabilities, and provides examples.

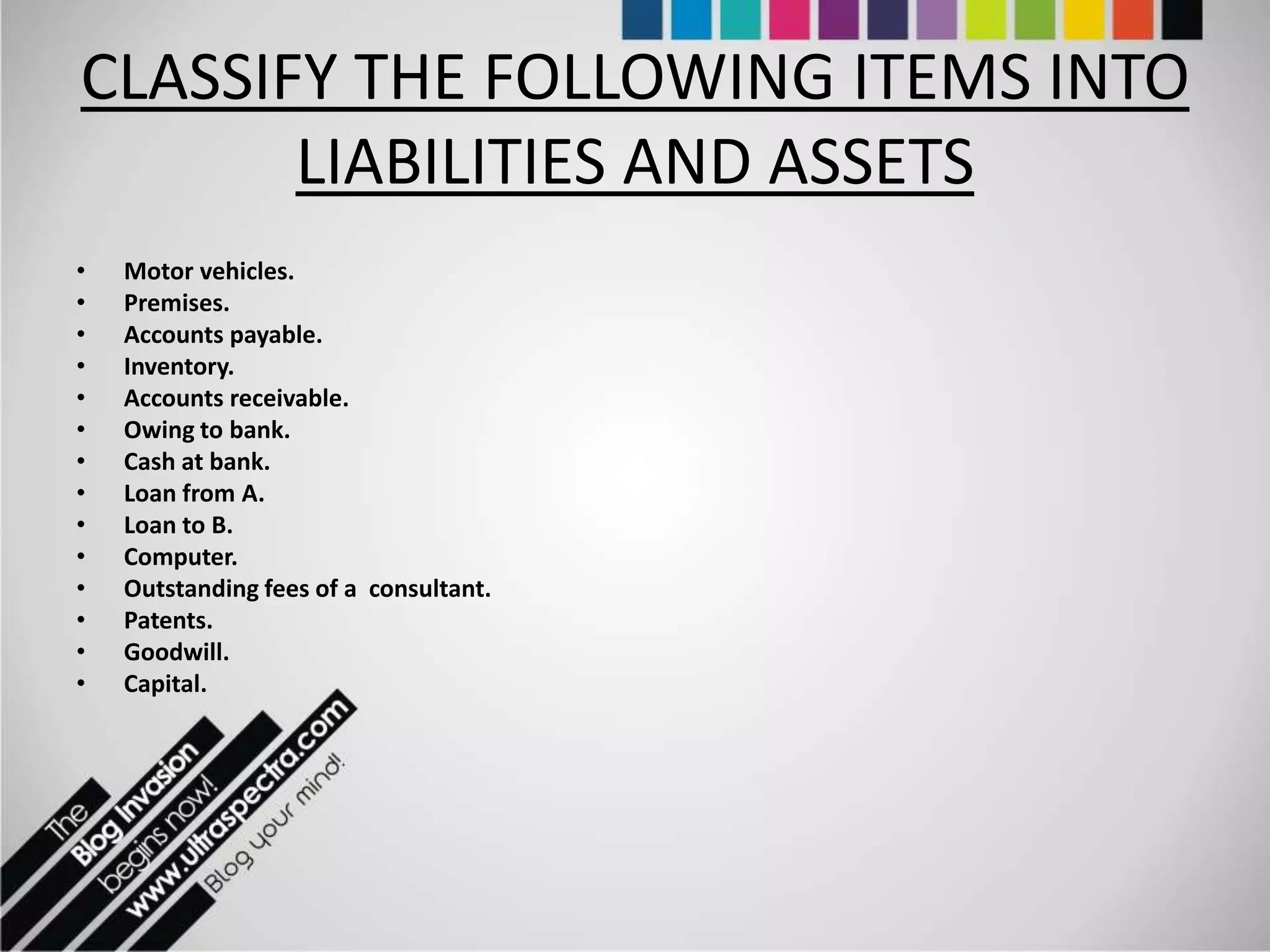

Activity on classifying items into liabilities and assets for practical understanding.

Shows contact information for Ultraspectra and Open Academy for further engagement.