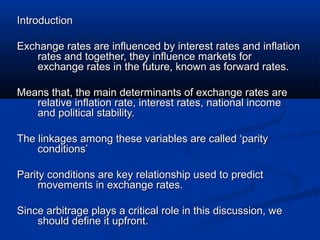

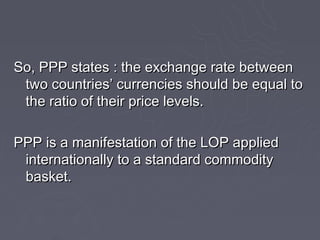

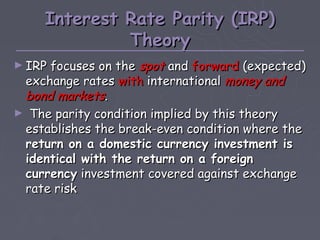

![EXAMPLE IFE

► Malaysia interest rate for 6-month 4%

► Australia interest rate for 6 month 8%

► Current spot rate is MYR2.8735/AUD

► What is forecast future spot rate of the MYR/AUD if the

interest rate in Australia were rise to 10% p.a?

► Future spot rate = 2.8735 [ 1 + 0.04/20] / [1 + (0.1/2)] =

2.7914](https://image.slidesharecdn.com/international-parity-conditions-9-feb-2010-120903101833-phpapp01/85/International-parity-conditions-9-feb-2010-17-320.jpg)

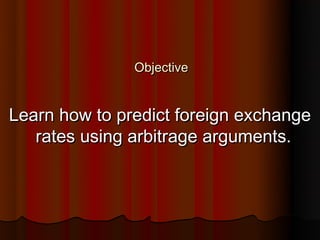

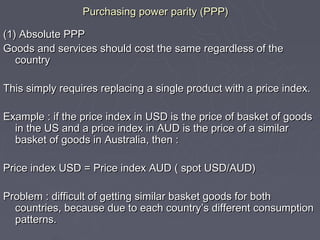

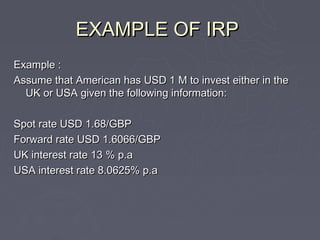

![UNCOVERED INTEREST RATE PARITY

Example :

Suppose that the current one year interest

rate in the US is 9.4% and the UK interest

rate is 11%. The spot rate is USD1.5 per

GBP.

► What is expected one year forward rate for

USD/GBP?

► [ 1 + 0.094] / [1 + 0.11] = f / s

► [ 1 + 0.094] / [1 + 0.11] = f / 1.5

► So one year USD/GBP = 1.478](https://image.slidesharecdn.com/international-parity-conditions-9-feb-2010-120903101833-phpapp01/85/International-parity-conditions-9-feb-2010-23-320.jpg)

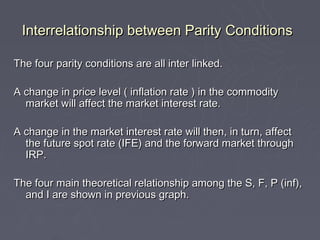

This document discusses several international parity conditions that can be used to predict foreign exchange rates: 1. Purchasing power parity (PPP) states that exchange rates should equalize price levels between countries based on a basket of goods. 2. The international Fisher effect (IFE) states that exchange rates adjust to equalize interest rate differentials between countries. 3. Interest rate parity (IRP) focuses on spot and forward exchange rates between countries' money and bond markets and establishes a break-even condition for returns. 4. Forward rates are expected to be an unbiased predictor of future spot rates according to the expectations theory of exchange rates. These parity conditions are interrelated

![ch04[1].ppt](https://cdn.slidesharecdn.com/ss_thumbnails/ch041-240114135454-79dcc99a-thumbnail.jpg?width=640&height=640&fit=bounds)

![Ch04[1]parity](https://cdn.slidesharecdn.com/ss_thumbnails/ch041parity-140310222946-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)