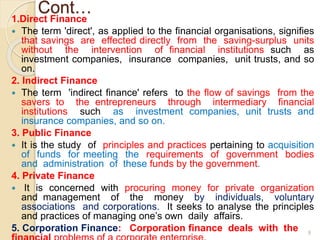

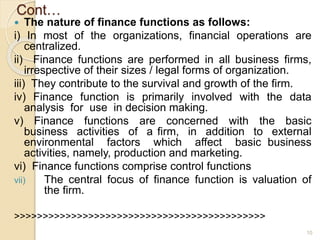

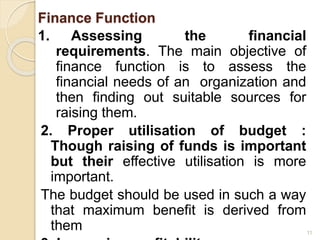

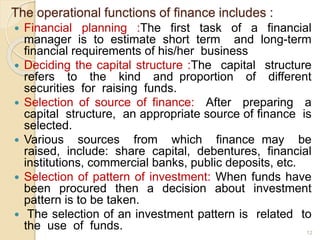

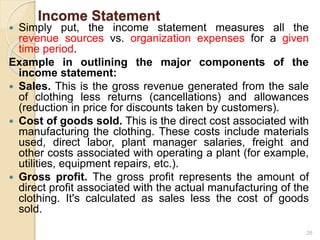

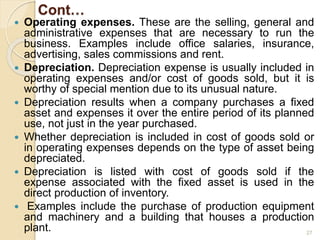

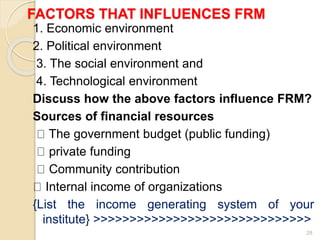

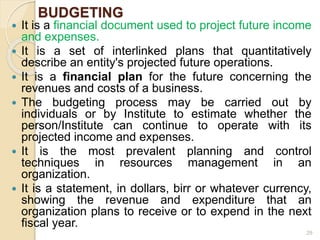

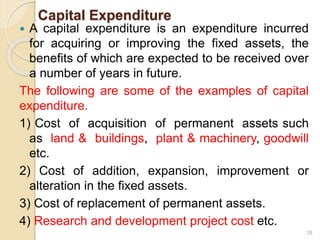

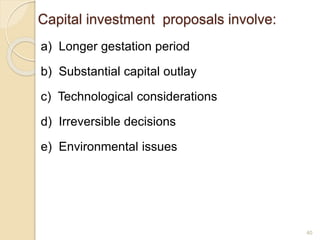

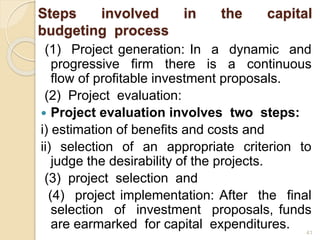

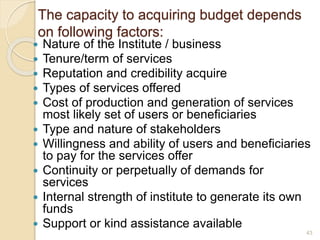

This document discusses resource management in technical and vocational education and training (TVET). It covers topics such as the definition of financial resource management, characteristics of financial management, types of finance, functions of a finance manager, factors influencing financial decisions, financial statements, budgeting, and sources of financial resources for TVET institutions. The key points are that financial resource management aims to efficiently allocate funds to achieve organizational goals, is influenced by internal and external factors, and involves financial planning, budgeting, and generating and utilizing various sources of income.

![Monitoring & evaluation presentation[1]](https://cdn.slidesharecdn.com/ss_thumbnails/monitoringevaluationpresentation1-110509033357-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)