Downloaded 234 times

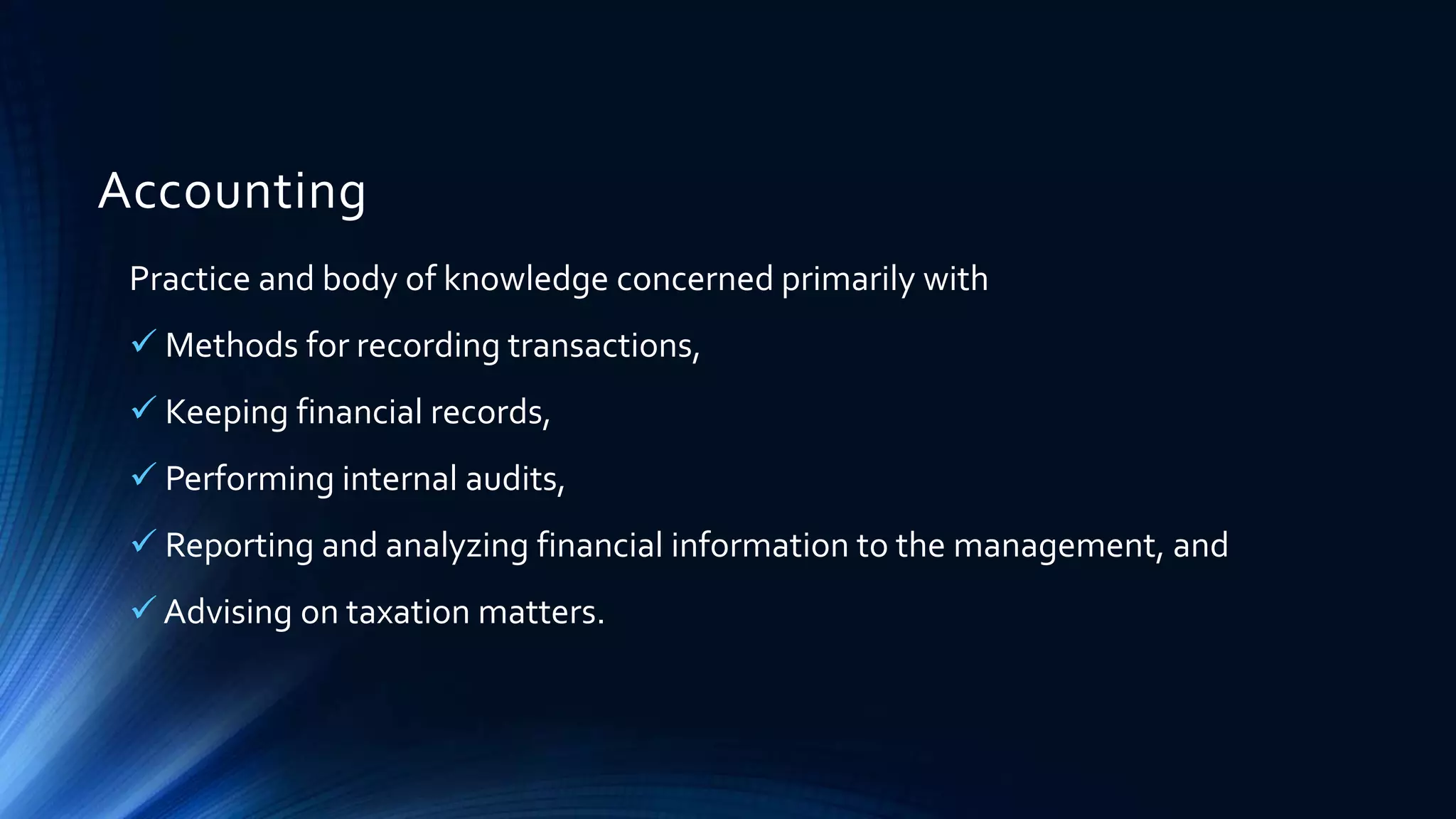

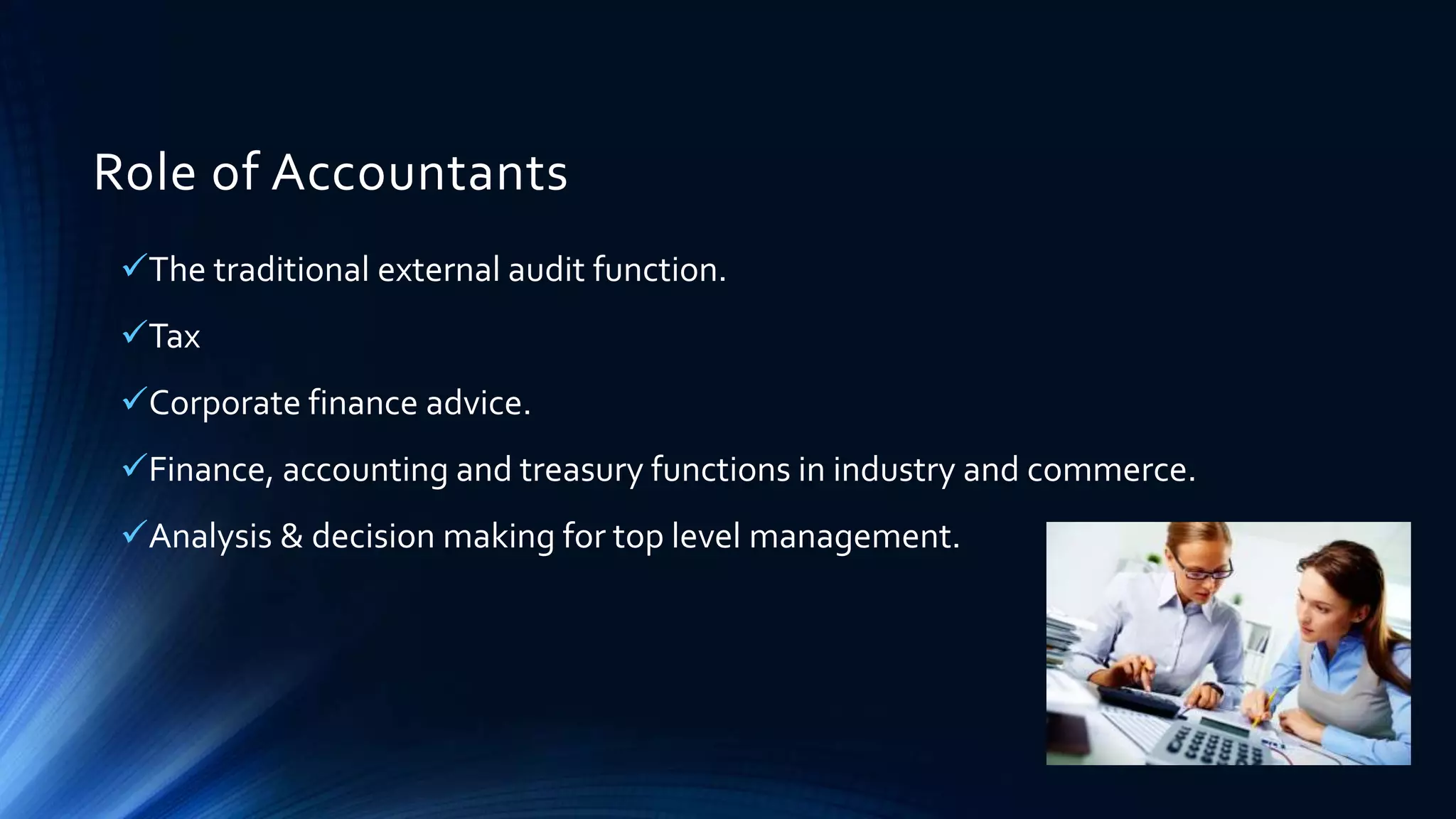

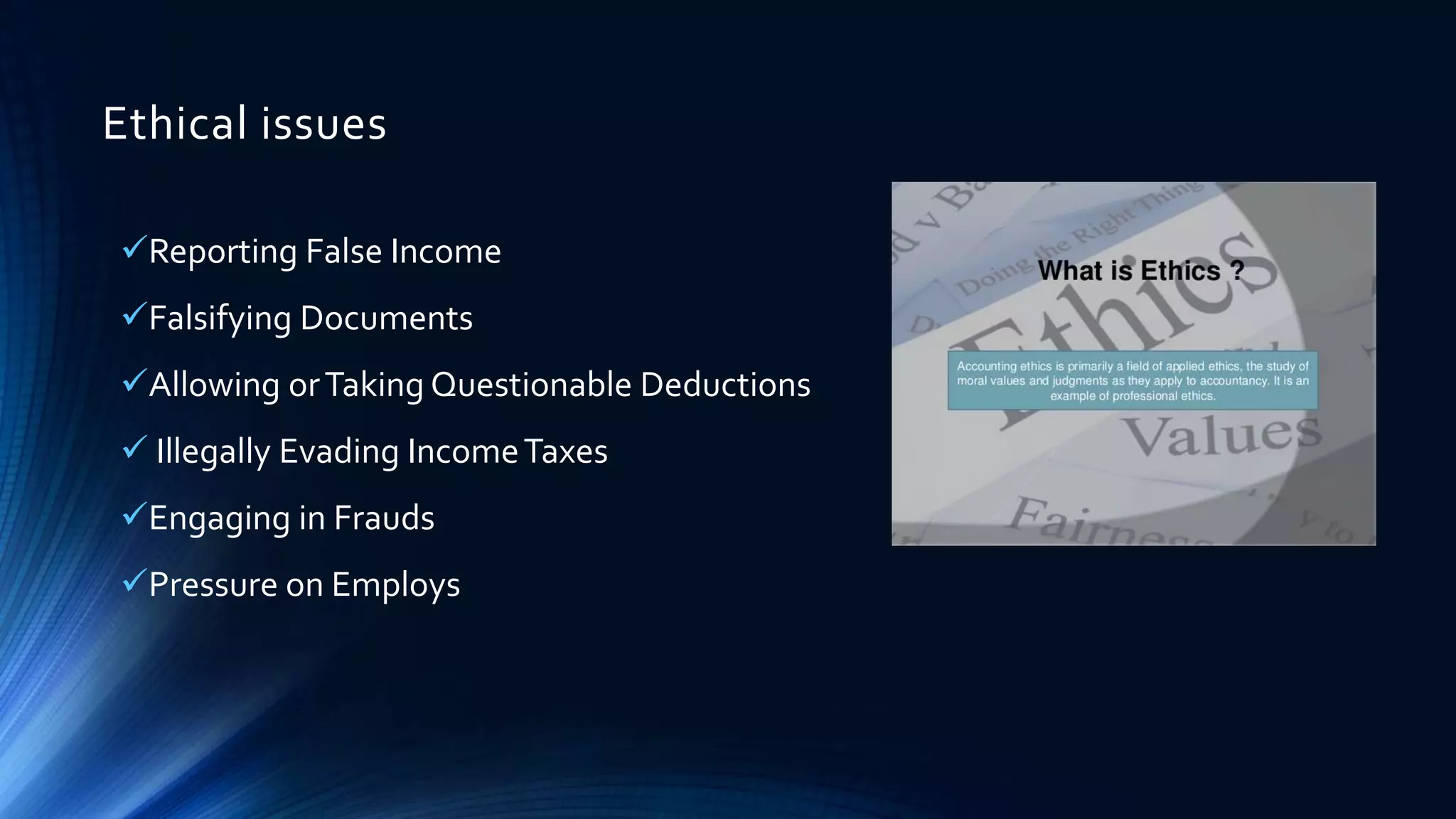

This document discusses ethics in accounting. It defines accounting as the practice of recording financial transactions and keeping financial records. Accountants play roles like auditing, taxation, and financial advising. Ethics refers to moral principles that govern behavior. Accounting ethics deals with what is morally right and wrong behavior for accountants. Unethical behavior can include fraud, falsifying documents, and tax evasion. Threats to ethical behavior include self-interest, self-review, advocacy, familiarity, and intimidation. Unethical environments can harm companies through loss of reputation and fines. To promote ethics, organizations can implement policies, training, oversight, and codes of conduct.