1) The Reserve Bank of India (RBI) is India's central bank. It was established in 1935 and nationalized in 1949. RBI performs traditional central banking functions like issuing currency, acting as a banker to the government and banks, and maintaining foreign exchange reserves.

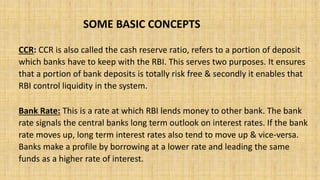

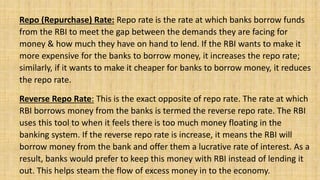

2) RBI also regulates the banking system through tools like the cash reserve ratio (CRR), which requires banks to hold a portion of deposits with RBI, the repo rate at which banks borrow from RBI, and the reverse repo rate at which RBI borrows from banks.

3) Other RBI functions include acting as a lender of last resort, controlling credit in the economy, collecting and publishing banking data, and