Download as PDF, PPTX

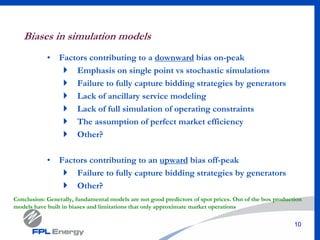

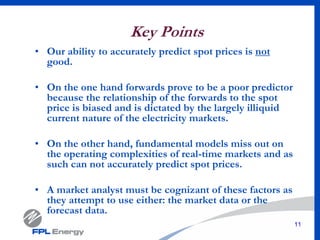

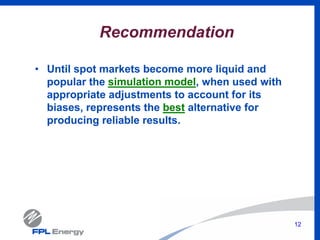

The document discusses the challenges of predicting spot prices in electricity markets, emphasizing that both forward price curves and forecast models fail to provide consistent predictability. It highlights that forwards are unreliable due to bias and market illiquidity, while forecast models suffer from inherent limitations and biases. The recommendation suggests using simulation models with necessary adjustments until market conditions improve.