Downloaded 33 times

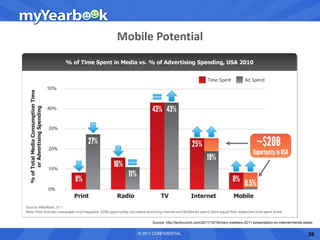

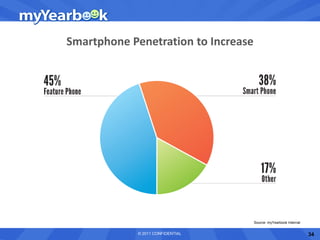

This document discusses trends in mobile monetization from 2011. It notes that mobile usage is growing rapidly and will soon surpass web usage. While mobile users are highly engaged, monetization lags behind the web due to limitations of mobile advertising and payment systems. The document outlines strategies that mobile game companies are using successfully, such as in-app purchases and advertising. It predicts that monetization will improve as smartphone adoption increases, payment systems become more seamless, and new ad formats and locations-based capabilities develop. Mobile will become the primary way that users engage with brands and content.

![Getting Started with Apache Spark: Big Data Made Simple [Free Meetup]](https://cdn.slidesharecdn.com/ss_thumbnails/apachesparkgettingstarted-260203175547-8361bcc3-thumbnail.jpg?width=640&height=640&fit=bounds)