Download as PDF, PPTX

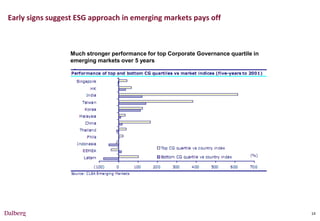

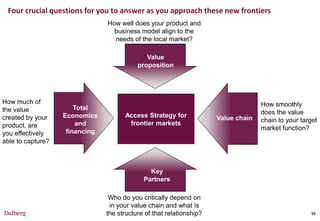

The document discusses opportunities for growth and investment in developing economies beyond the BRIC countries. It notes that: - Countries like Brazil, Russia, India and China have transformed rapidly in recent decades, reducing poverty and growing their economies. - A new wave of countries is following a similar path of steady growth above 3% annually with improving business conditions. - These emerging markets represent commercial opportunities in sectors like banking, agriculture, and renewable energy to serve their growing populations and economies. - Successfully capturing these opportunities requires understanding local needs and partnering with key local players, while navigating environmental, social and governance risks.

![Ge Final[1]](https://cdn.slidesharecdn.com/ss_thumbnails/ge-final11249-thumbnail.jpg?width=640&height=640&fit=bounds)