The document outlines the principles of credit management, emphasizing the roles of the credit department in setting and monitoring customer credit limits and distinguishing between simple and automatic credit checks. It discusses the configuration steps for establishing credit control areas, risk categories, and credit groups within SAP, as well as the necessary parameters for managing credit exposure and limits effectively. It also highlights various system responses such as warning messages and order blocks depending on credit limit violations.

Introduction to credit management, roles of the credit department, credit limits, and types of credit checks.

Description of centralized and decentralized credit processing; integration of credit management with configuration.

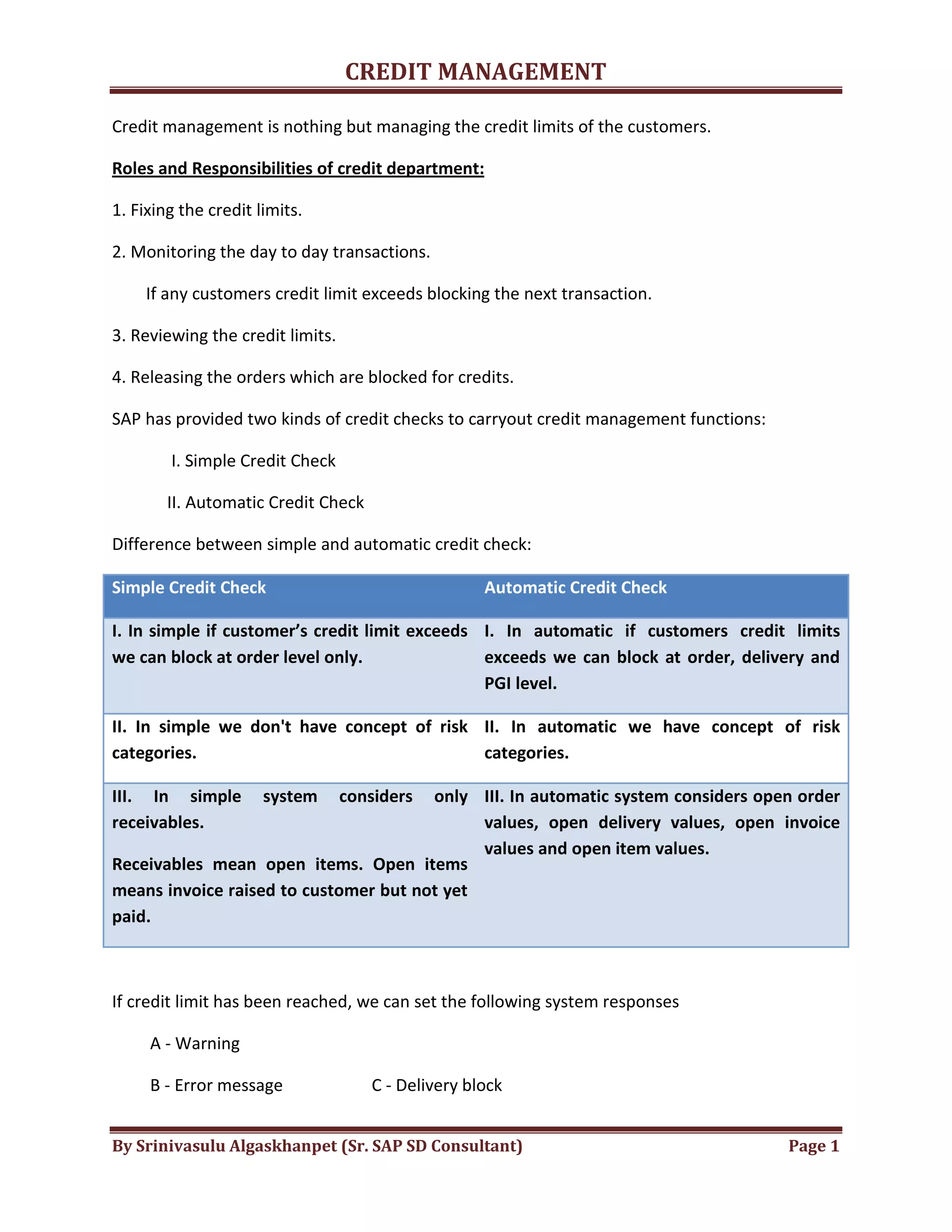

Steps to define the credit control area and update groups relevant for credit management.

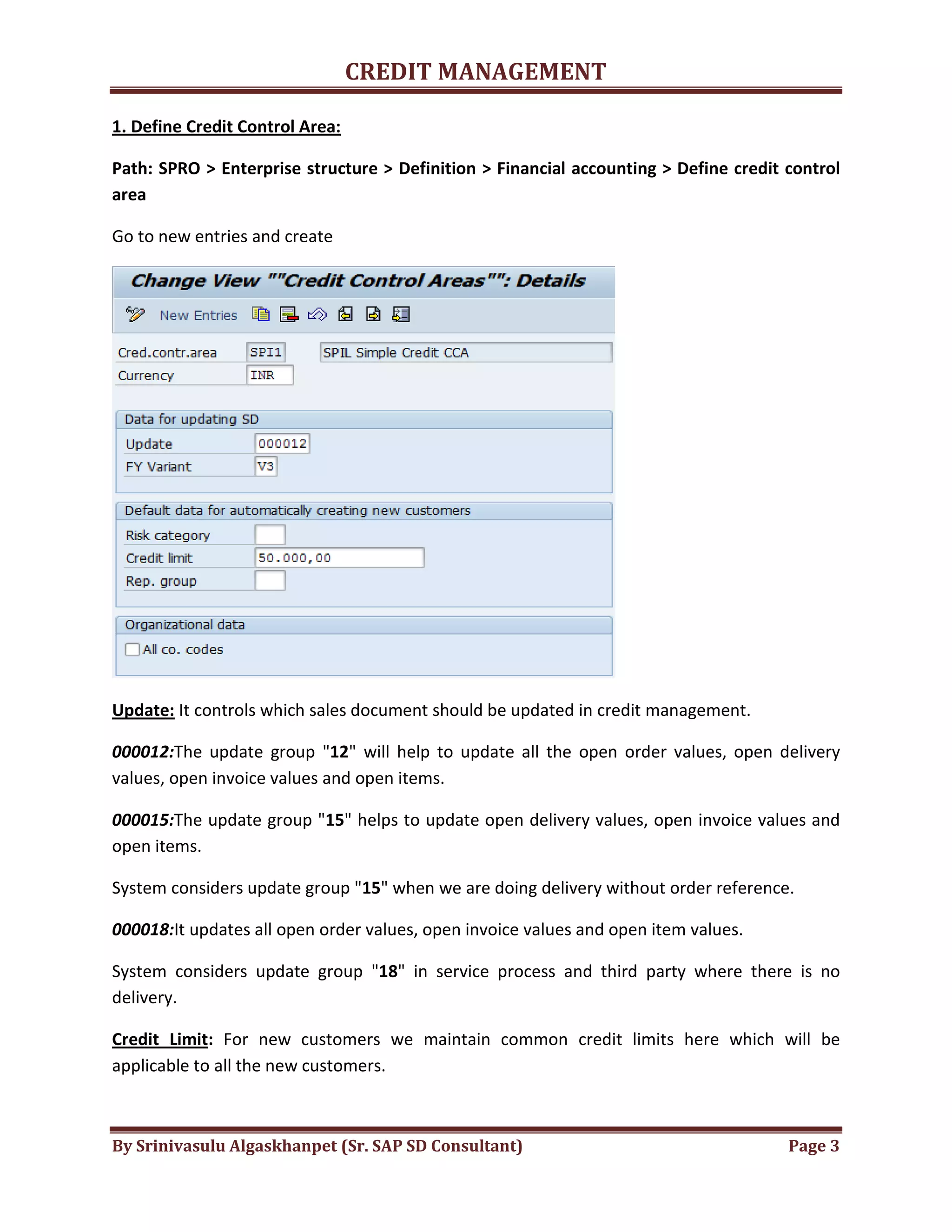

Configuration for assigning credit control areas to company codes and setting default indicators.

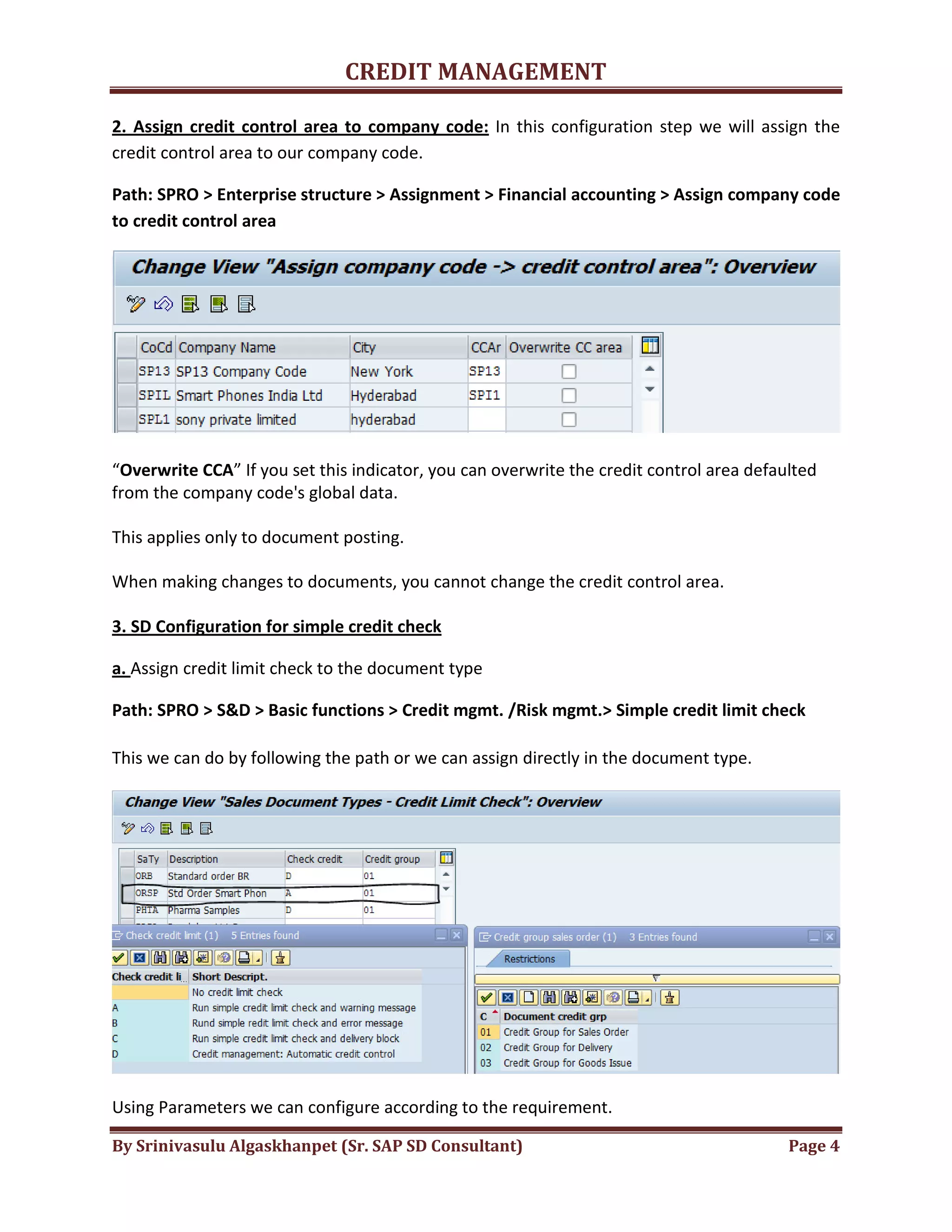

Steps to maintain pricing procedures and credit management updates using simple credit control.

Procedure for maintaining customer credit limits using T. Code FD32 and updating system messages.

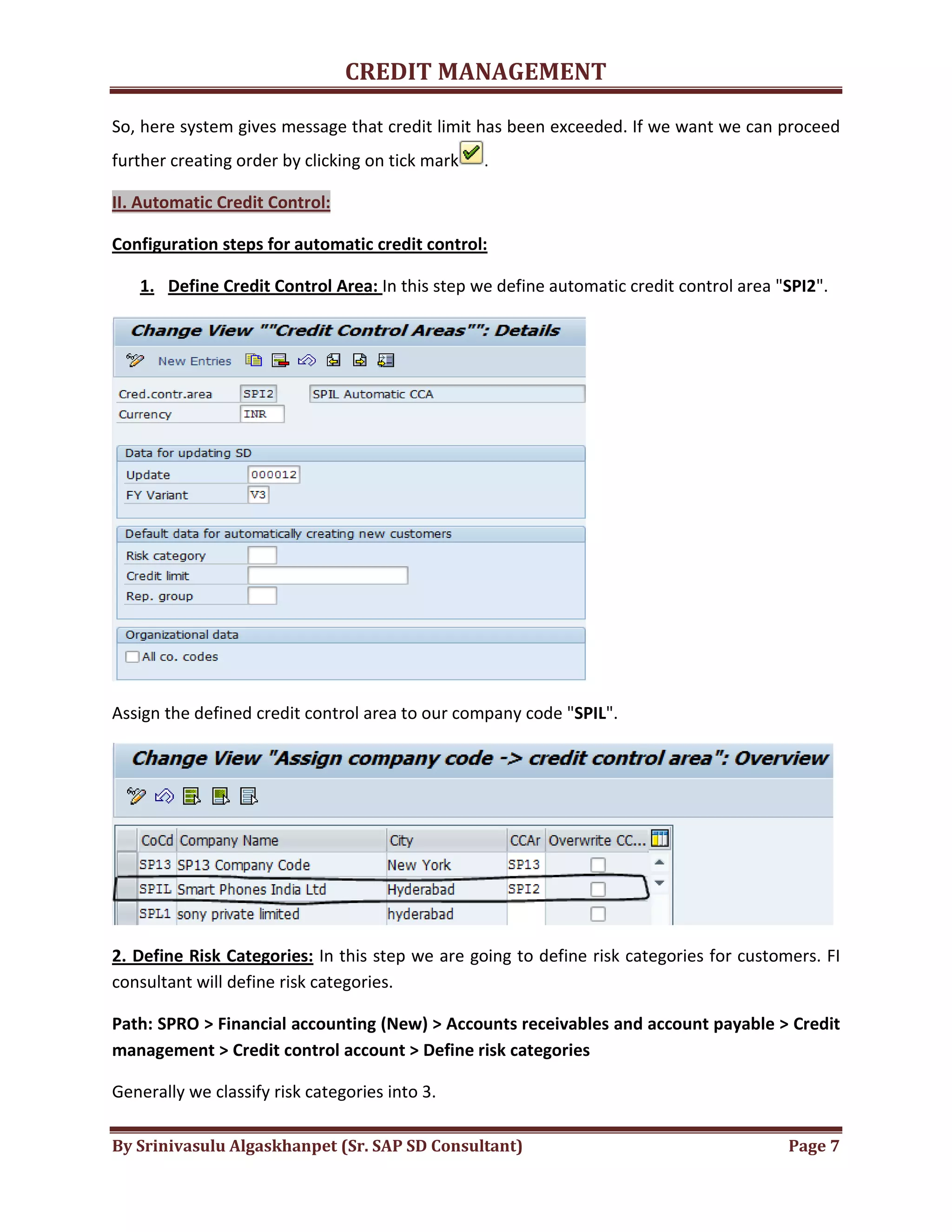

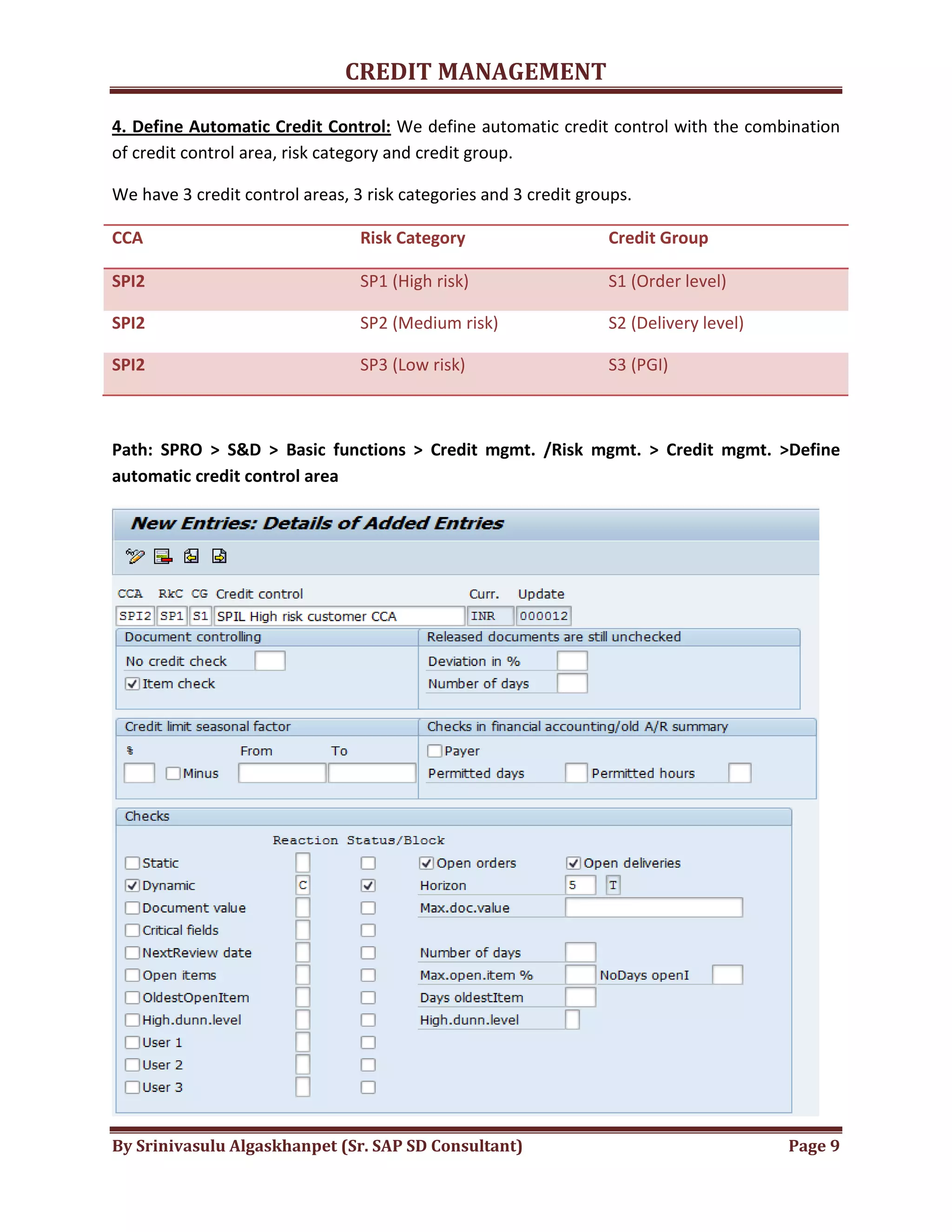

Initial configuration for automatic credit control, defining risk categories, and their impact.

Classification of risk categories (high, medium, low) and defining credit groups for different transactions.

Integration of credit control area, risk category, and credit group in automatic credit control settings.

Configurations available in automatic credit control, including item checks, deviations, and seasonal adjustments.

Detailed advanced fields in automatic credit control, such as maximum document value and oldest open items.

Management of multiple payers, user exits for customization, and conditions under which credit may be blocked.

Various T/Codes used for releasing credit blocks and managing delivery documents in credit management.

![The Credit Management Analysis Of Customers Traffic Flows And Pattern[1].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/thecreditmanagementanalysisofcustomerstrafficflowsandpattern1-240208055940-f5f40610-thumbnail.jpg?width=640&height=640&fit=bounds)