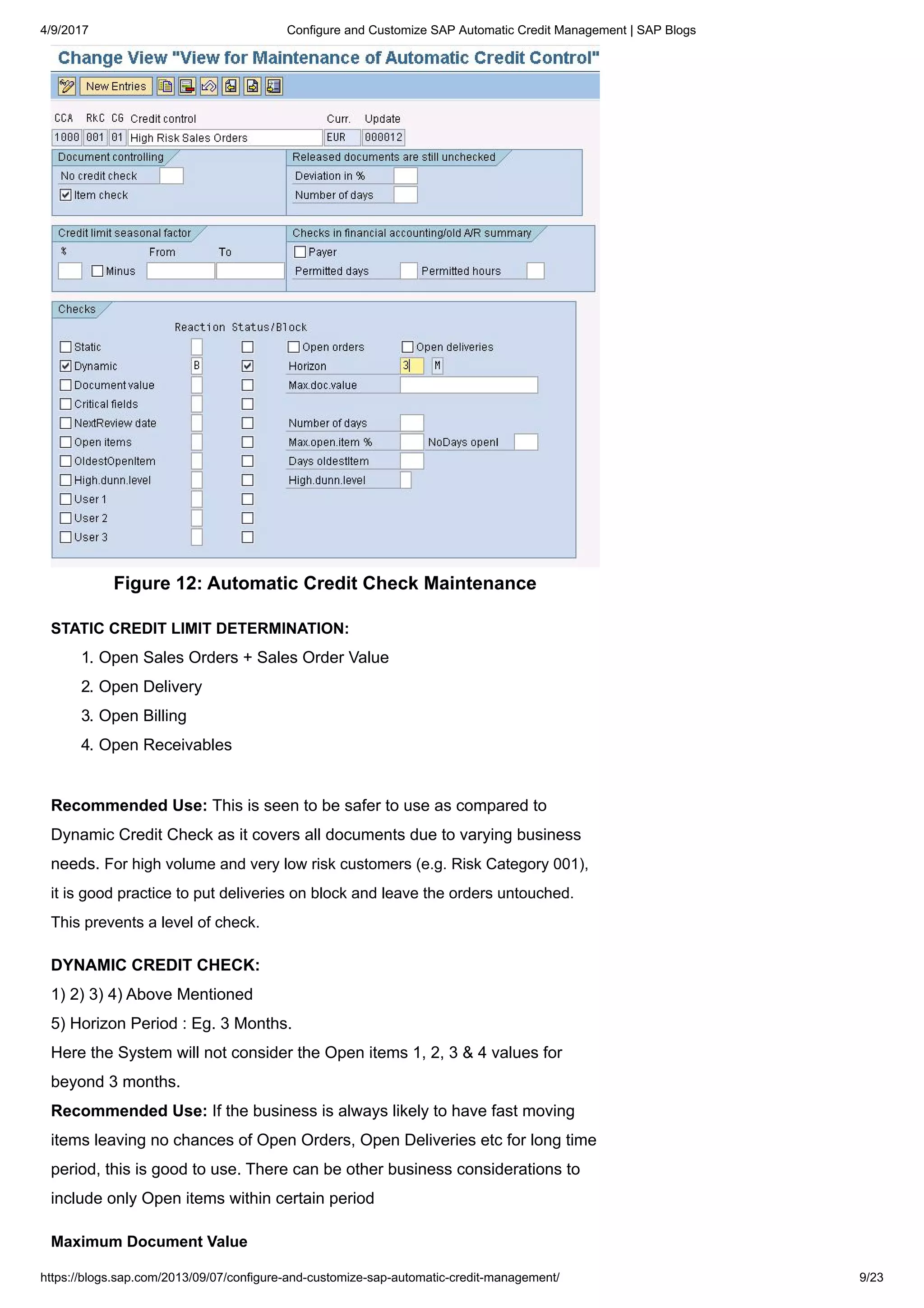

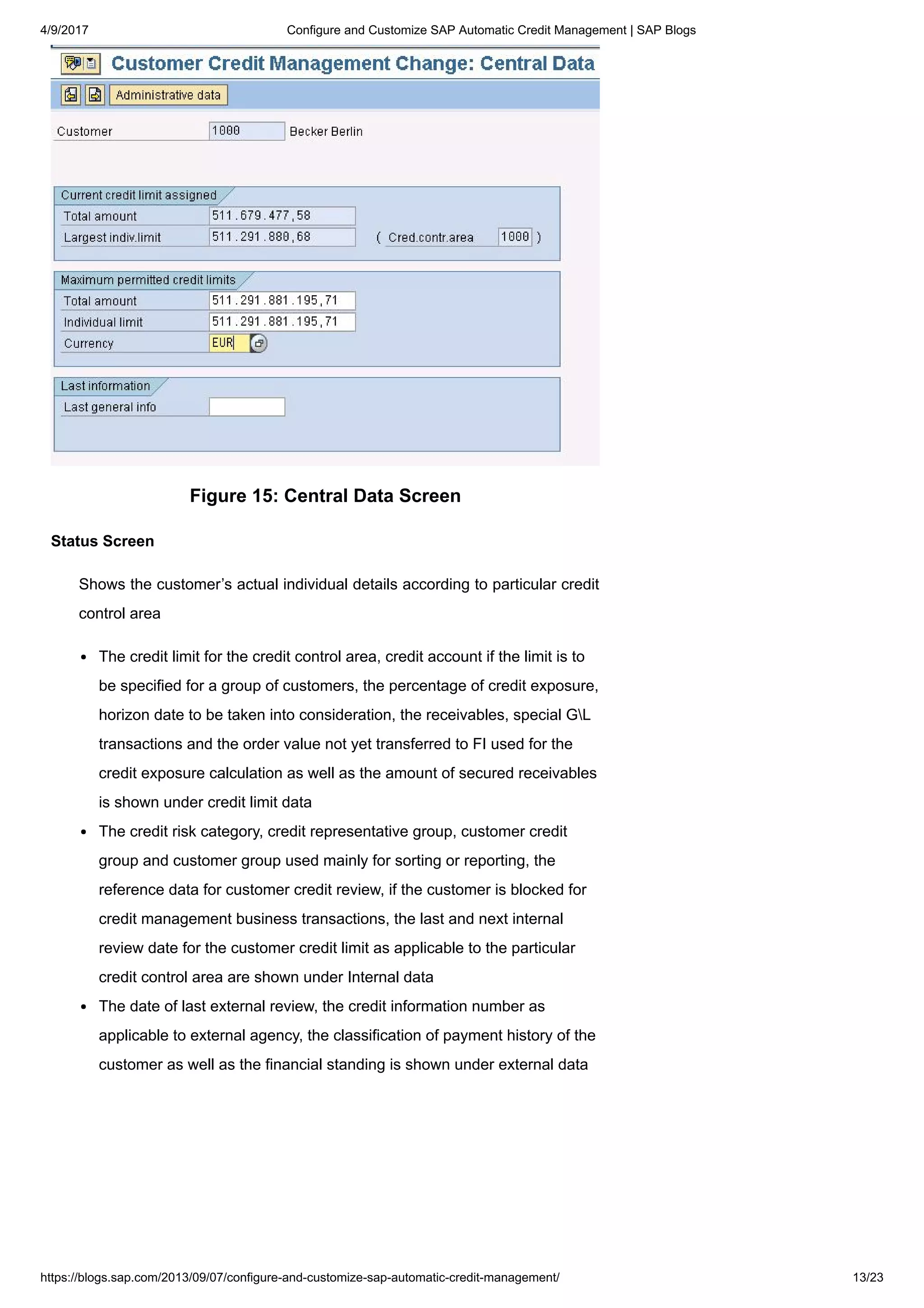

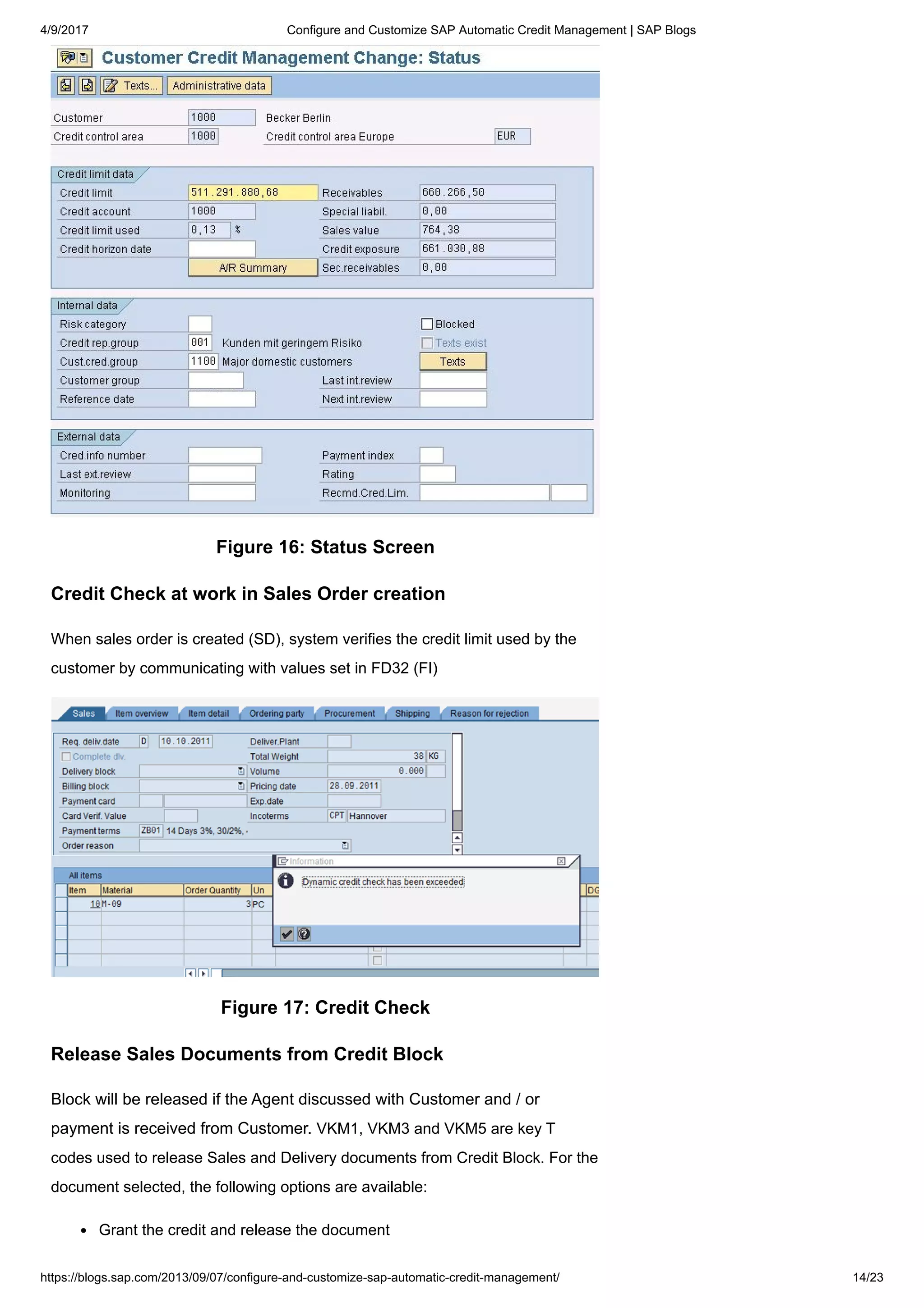

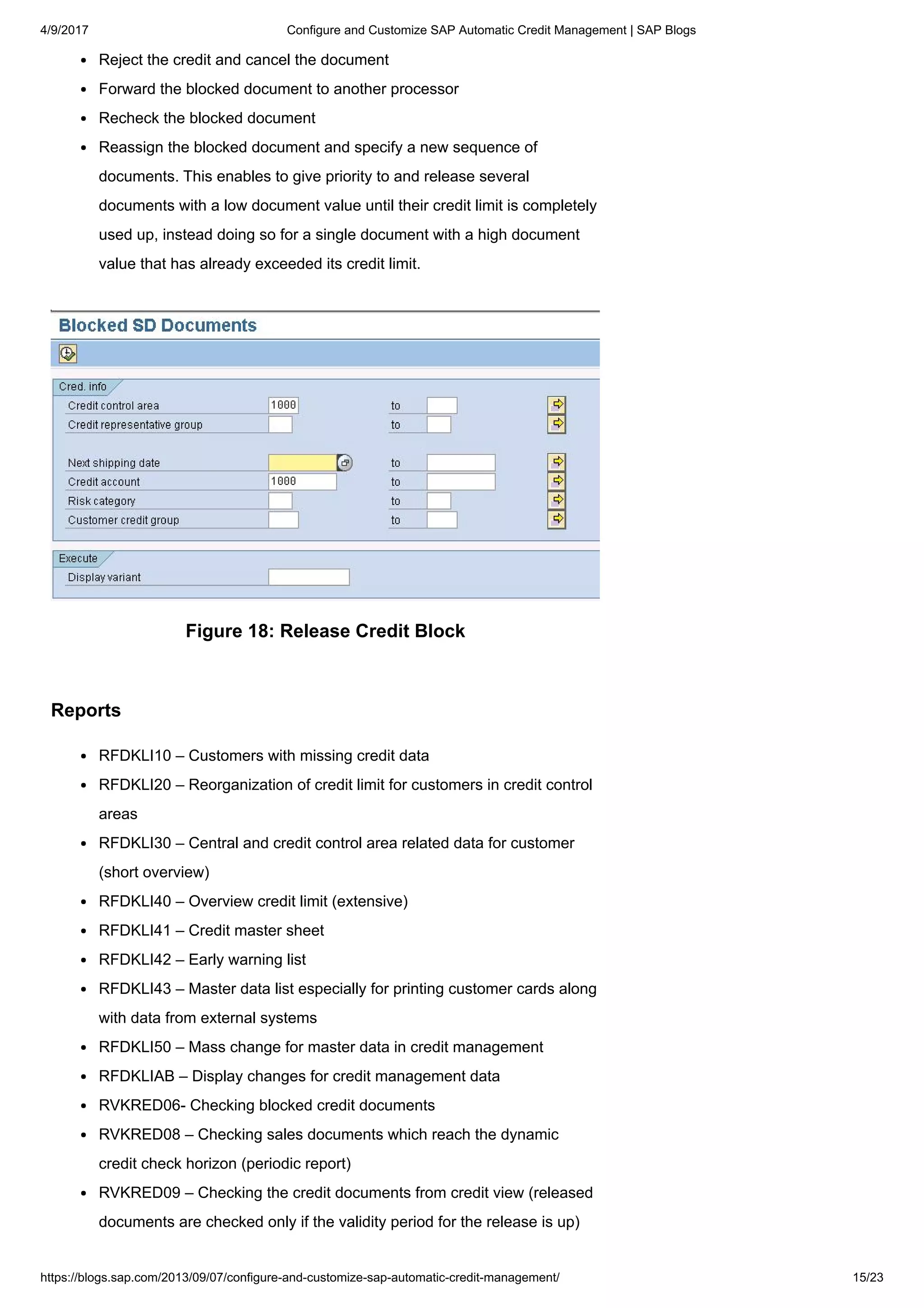

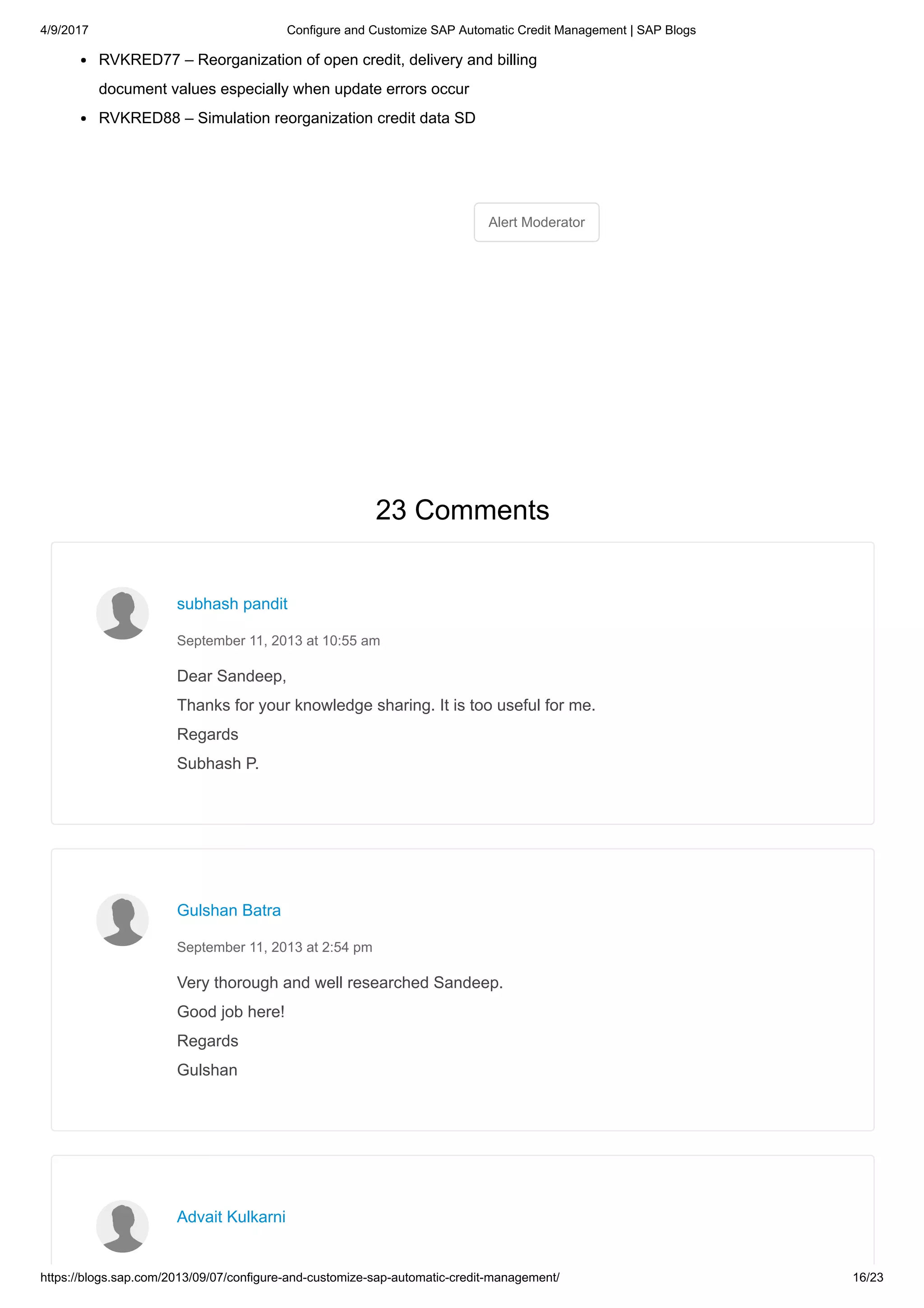

This document discusses how to configure and customize SAP's automatic credit management functionality. It covers defining risk categories and credit control areas, assigning company codes and sales areas, setting up credit groups, and configuring credit limit checks for orders and deliveries. The document also compares simple versus automatic credit checks, noting that automatic checks provide more parameters and are better for high-volume, low-value transactions, while simple checks are preferable for low-volume, high-value situations. Key steps outlined include setting up organizational units, credit limits, and rules for blocking transactions when limits are exceeded.

![4/9/2017 Configure and Customize SAP Automatic Credit Management | SAP Blogs

https://blogs.sap.com/2013/09/07/configure-and-customize-sap-automatic-credit-management/ 8/23

Simple Credit Check Vs Automatic Credit Check

a. High-volume, low-value requires automation and efficient handling

through grouping, with as little personal handling as possible (refuse

orders as much as possible)

b. Low-volume, high-value requires individualization with emphasis on

reporting and blocked orders or deliveries that can be checked and

unblocked.

Figure 11: Simple Credit Check Vs Automatic Credit Check

Simple Credit Check

The simple credit check compares the payer customer master record’s

credit limit to the net document value plus the value of all open items.

In case the value of the document and open items is more than the credit

limit:

System may respond with a warning message in the sales order [OR]

Warning message and a delivery block [OR]

Error message, which will cause the document not to be saved.

Automatic Credit Check Variations & Recommended Use

Automatic Credit Check – Gives extra parameters to define credit checks

like Credit Control Area, Risk Category and…](https://image.slidesharecdn.com/configureandcustomizeautomaticcreditmanagement-190717144901/75/Configure-and-customize-automatic-credit-management-8-2048.jpg)