Downloaded 10 times

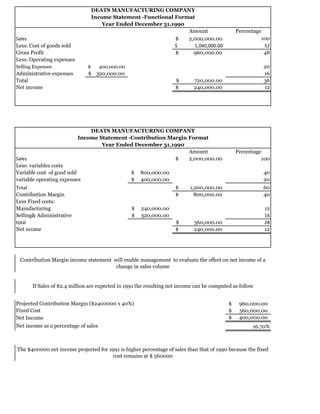

The document presents a detailed financial analysis of Deats Manufacturing Company and Irvin Company over several years, covering income statements, cost structures, and the implications of different costing methods (absorption vs variable costing) on net income. It emphasizes how fixed and variable costs interact with sales volumes and inventories, affecting financial outcomes and decision-making. Additionally, it explores cost estimation techniques such as linear regression and the high-low method for determining cost behavior in manufacturing settings.