Downloaded 129 times

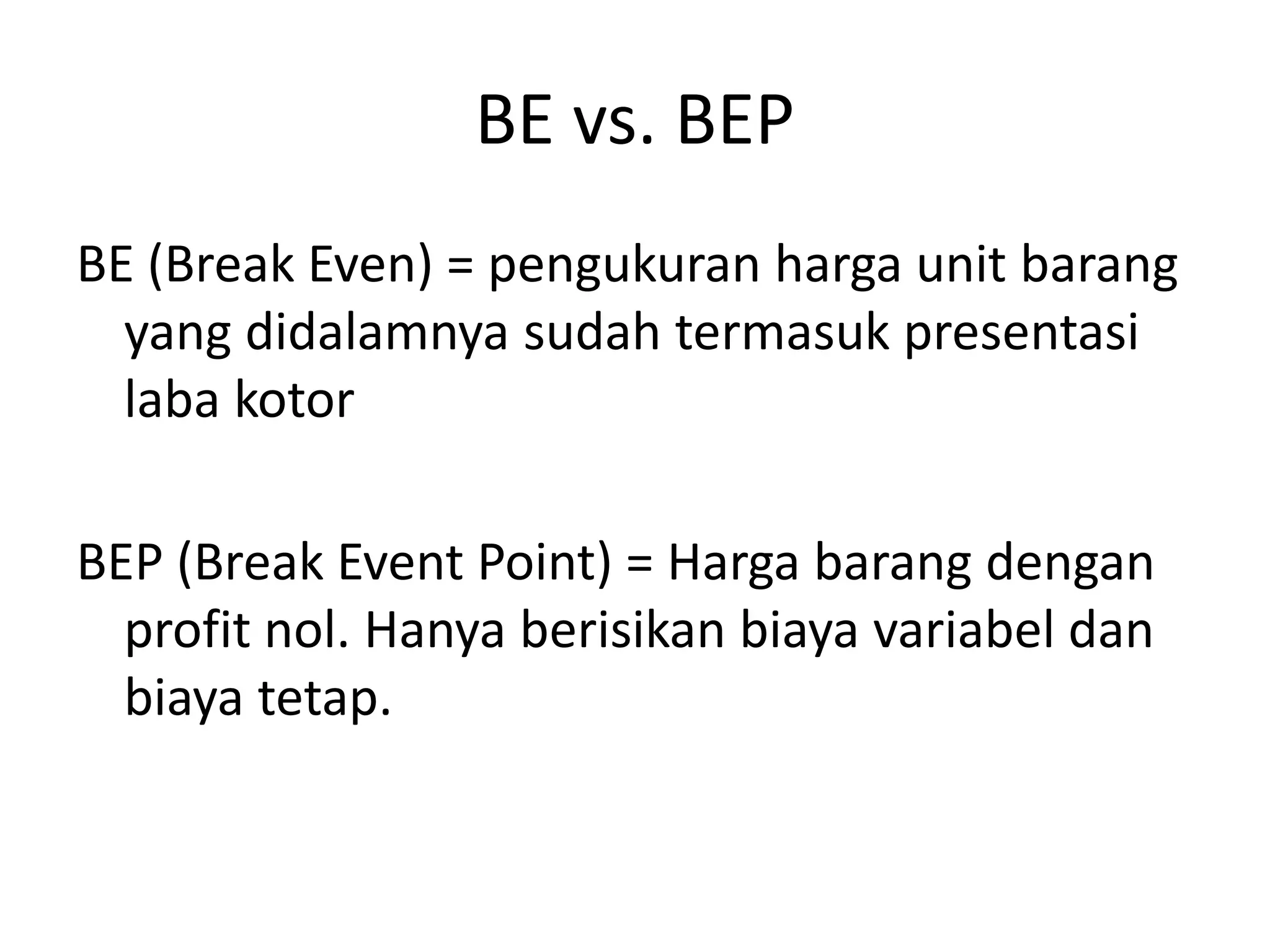

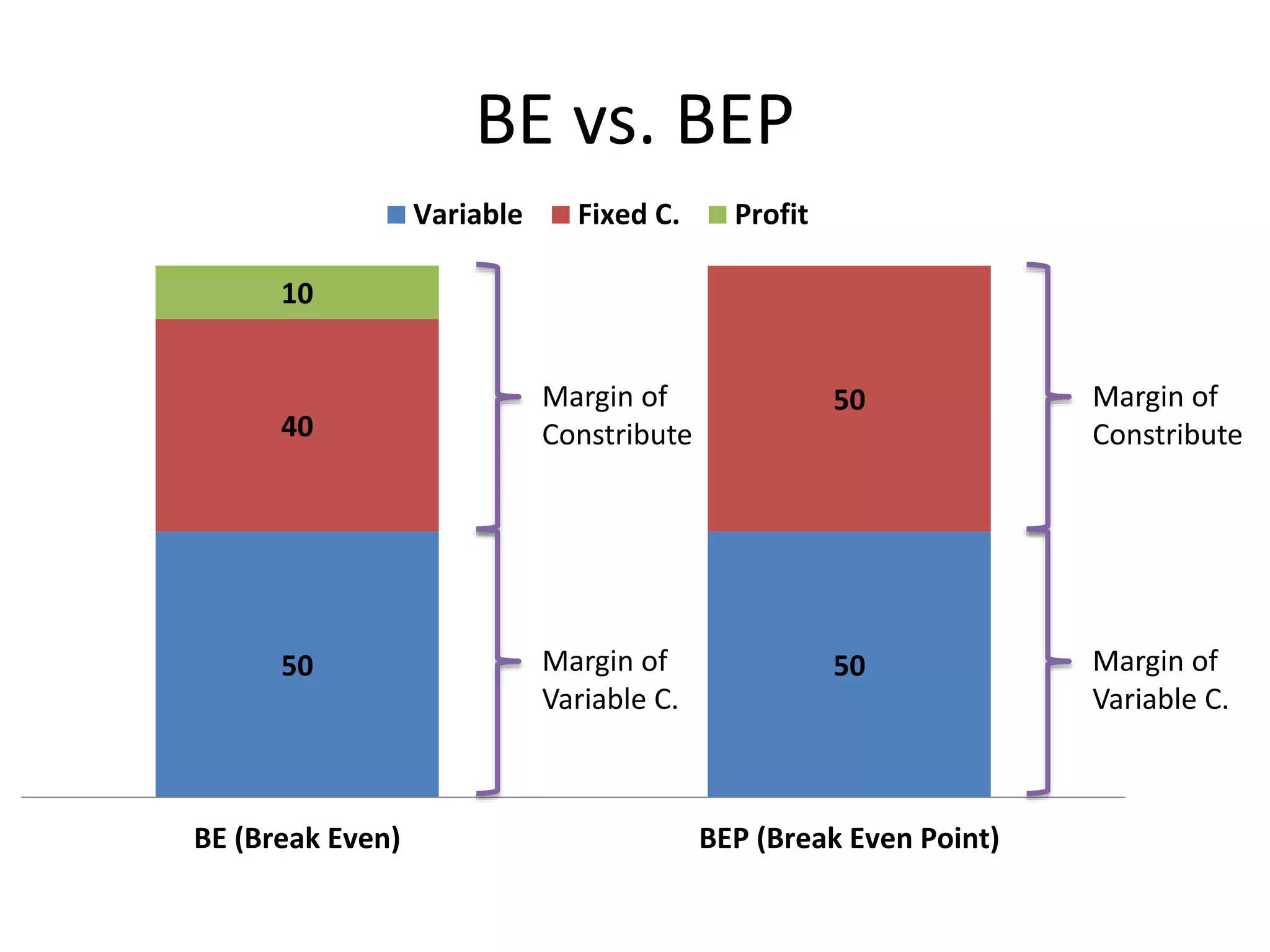

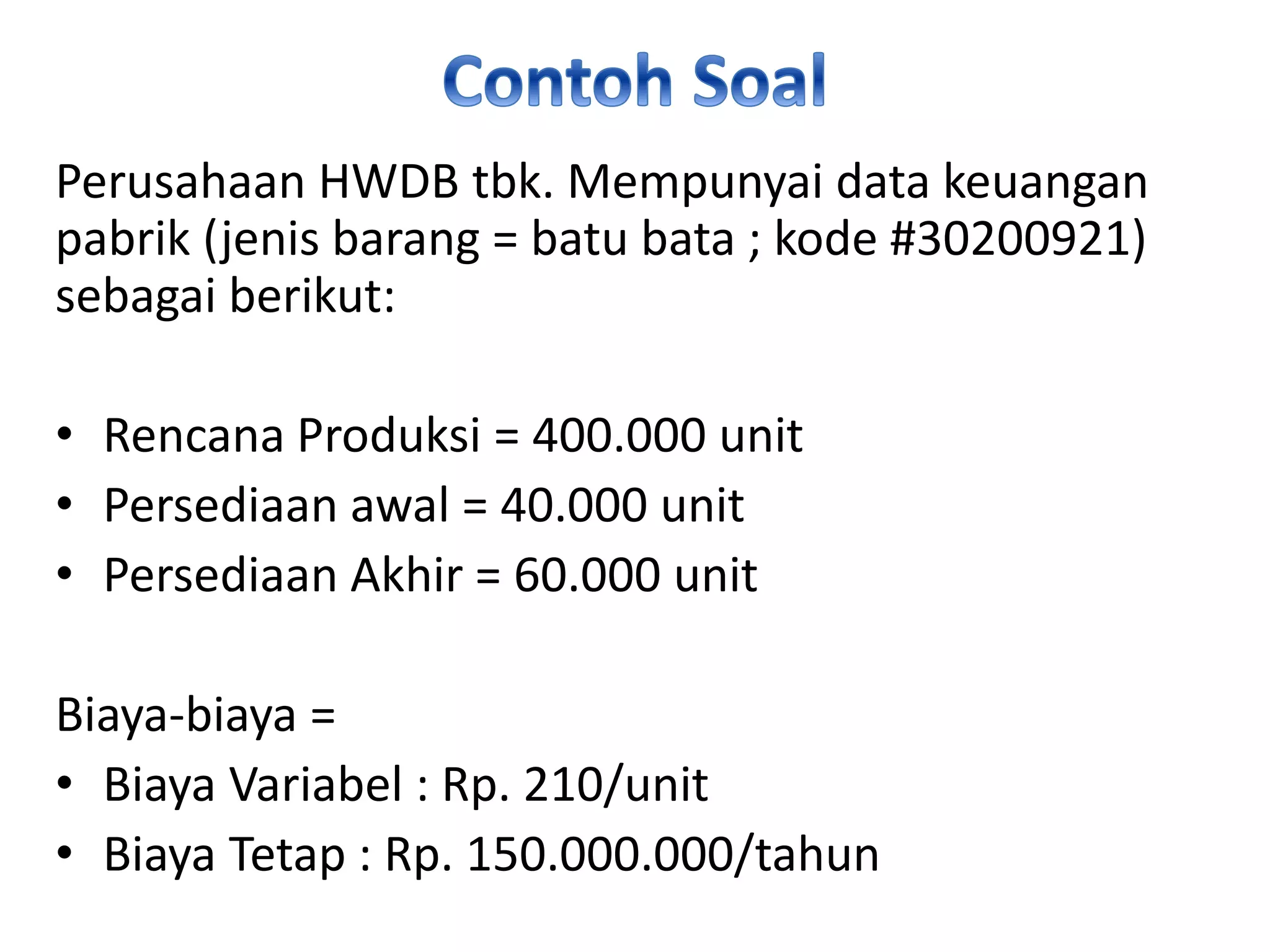

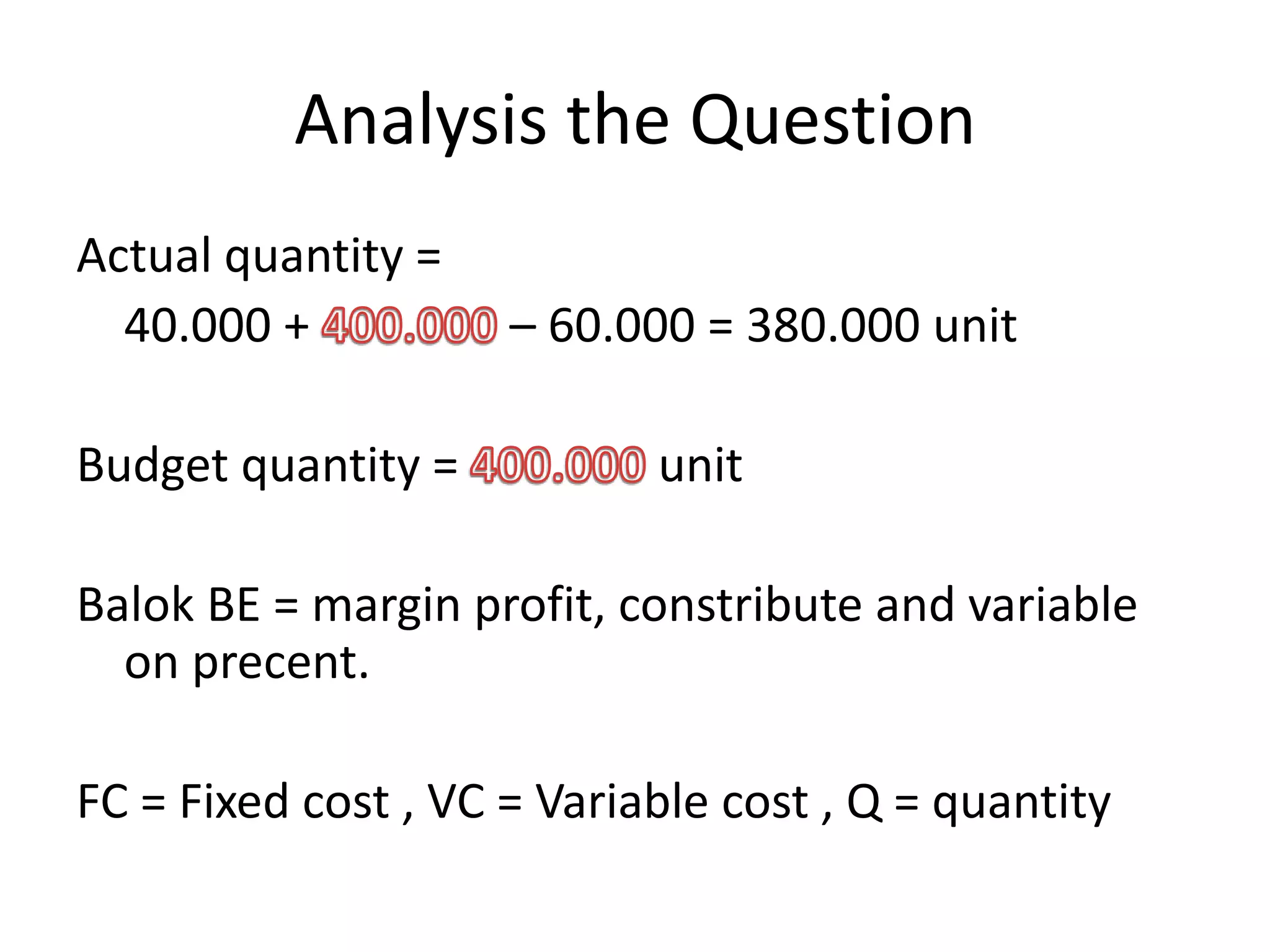

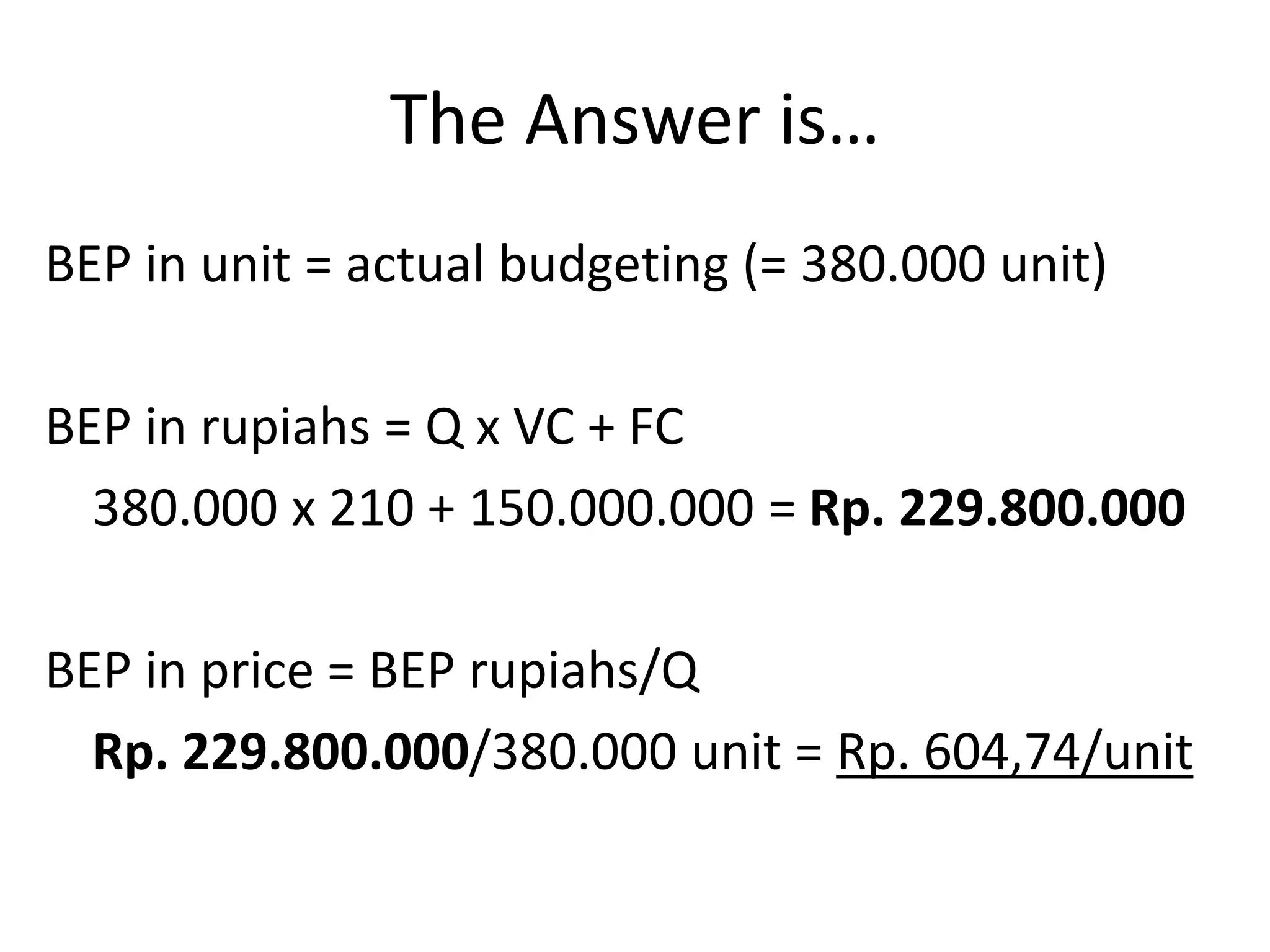

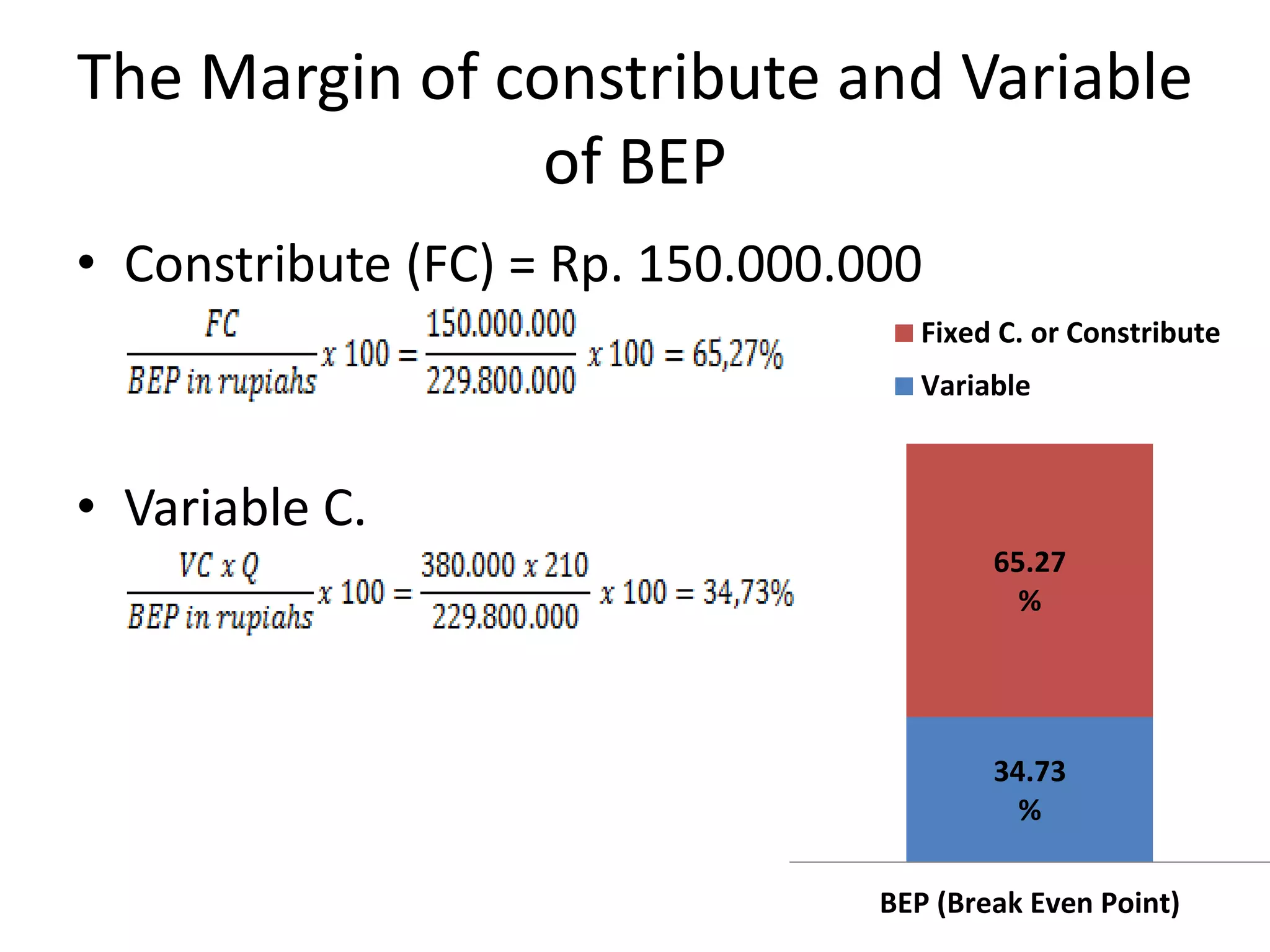

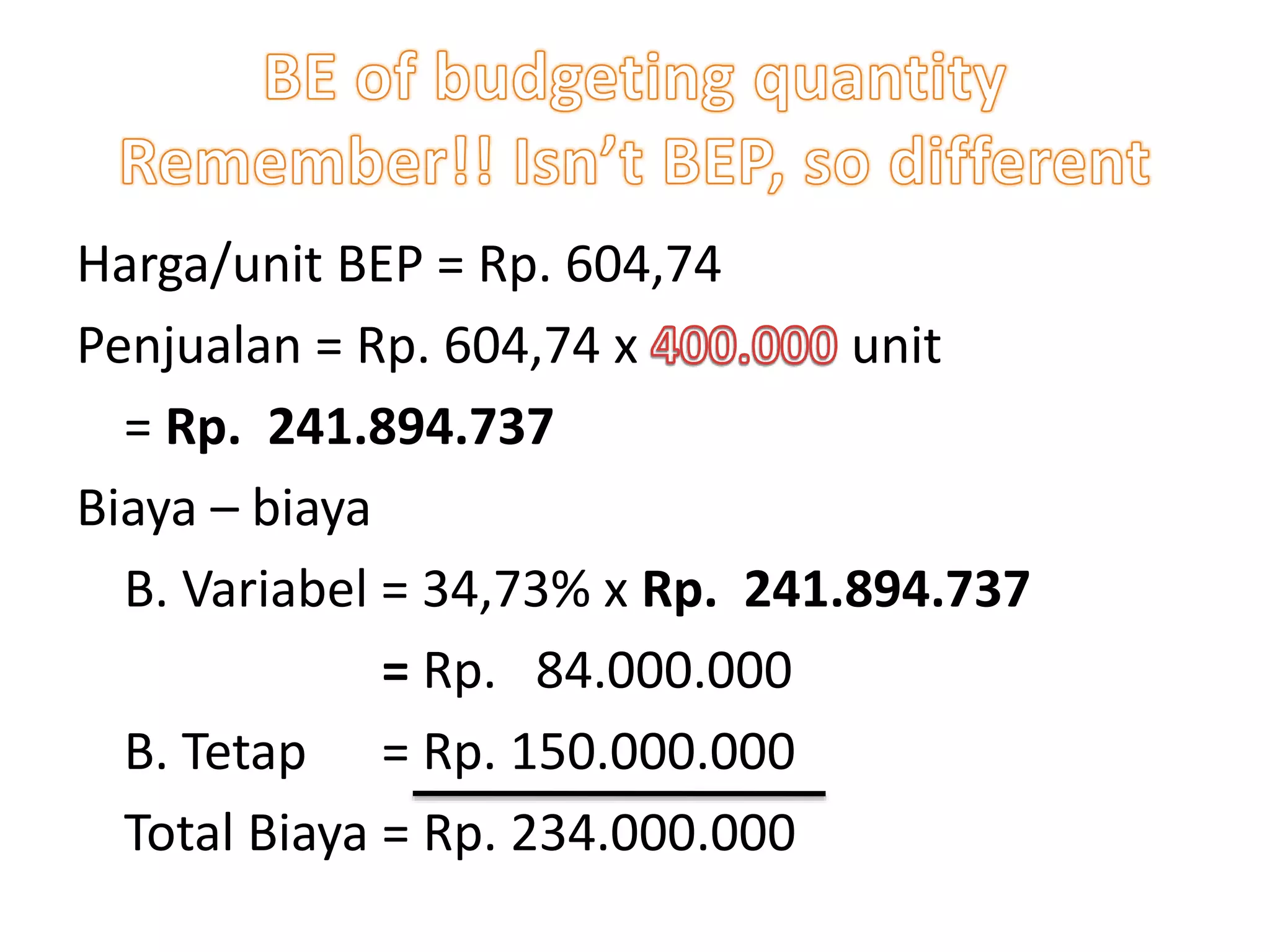

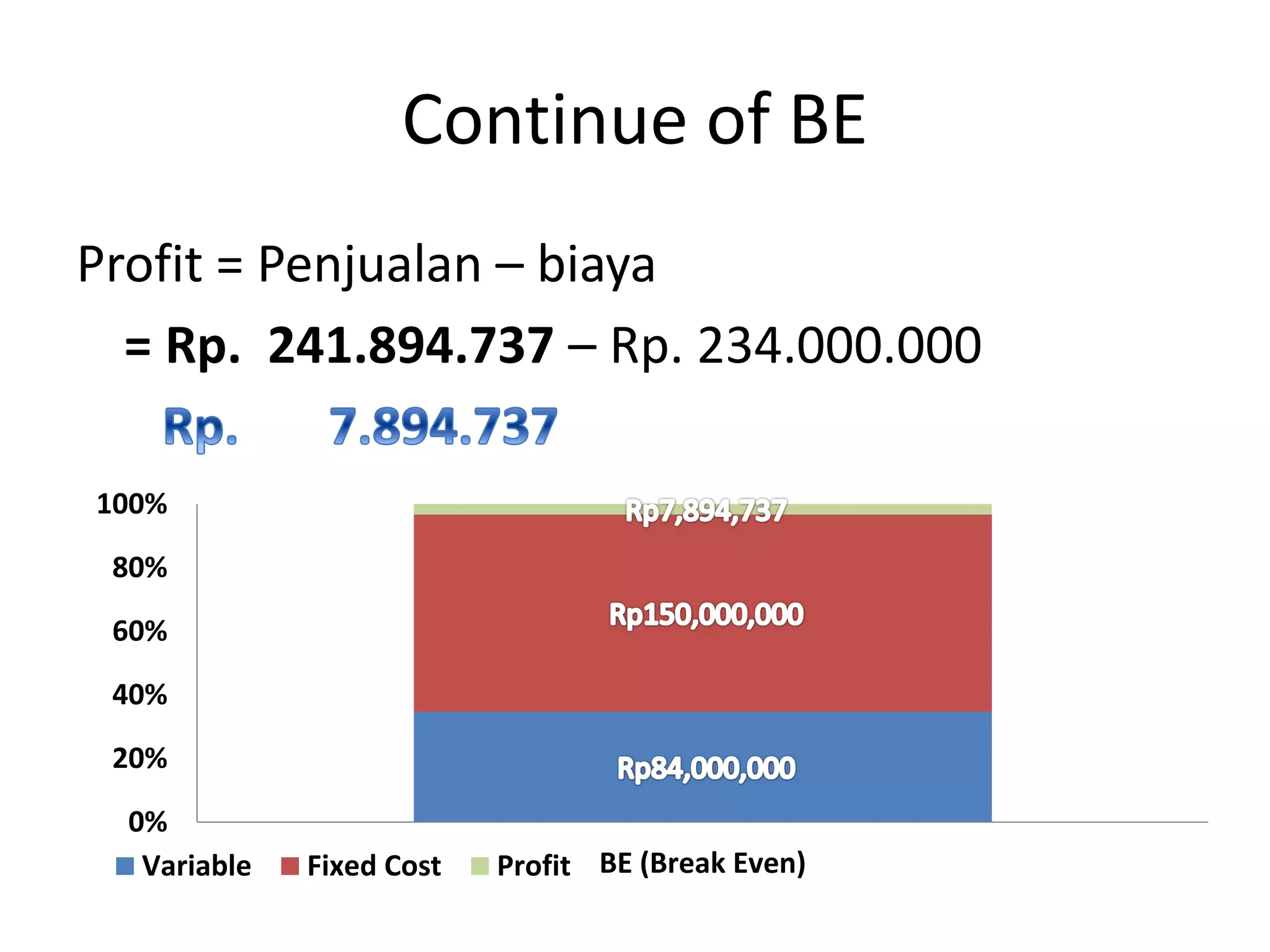

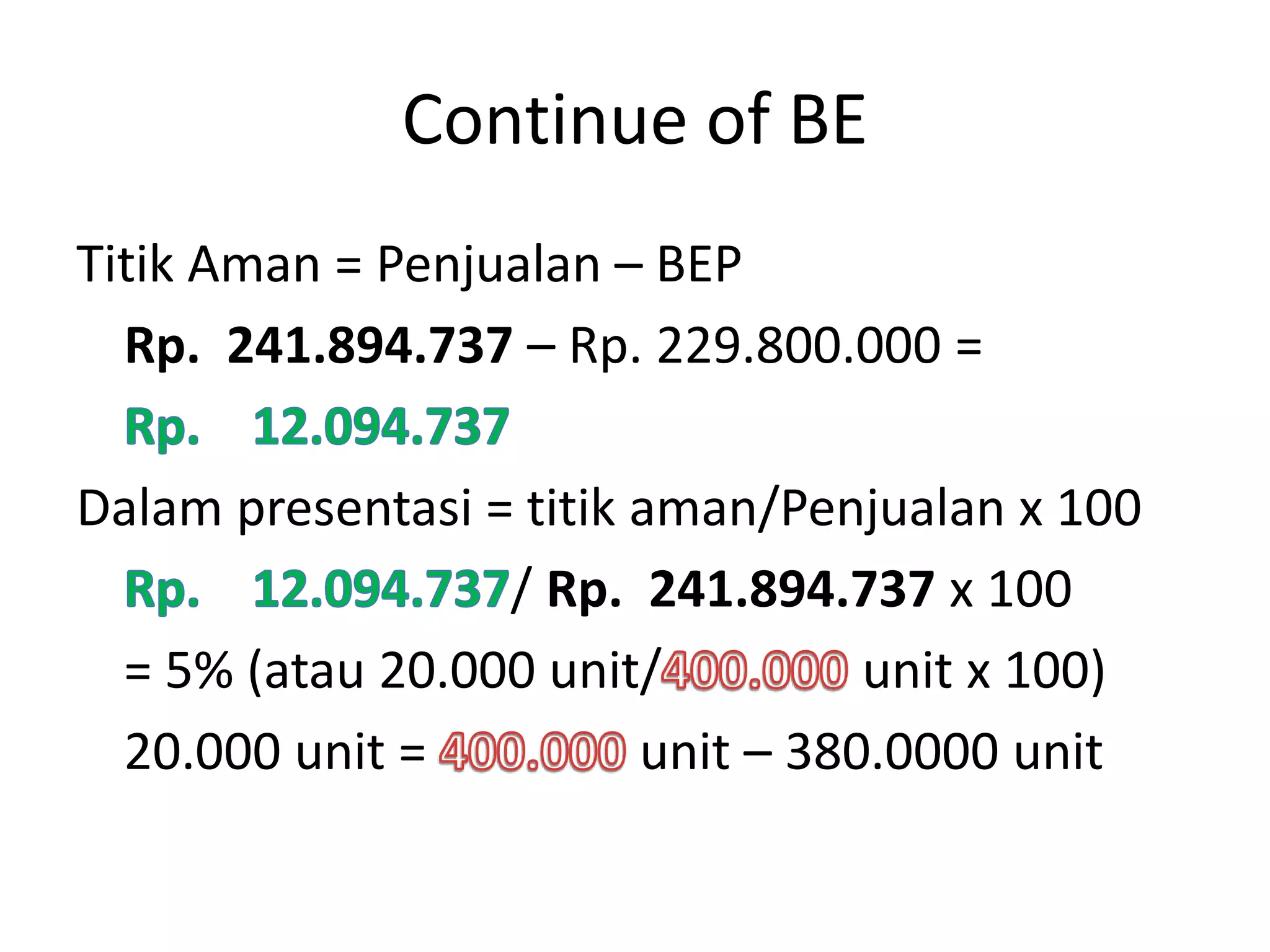

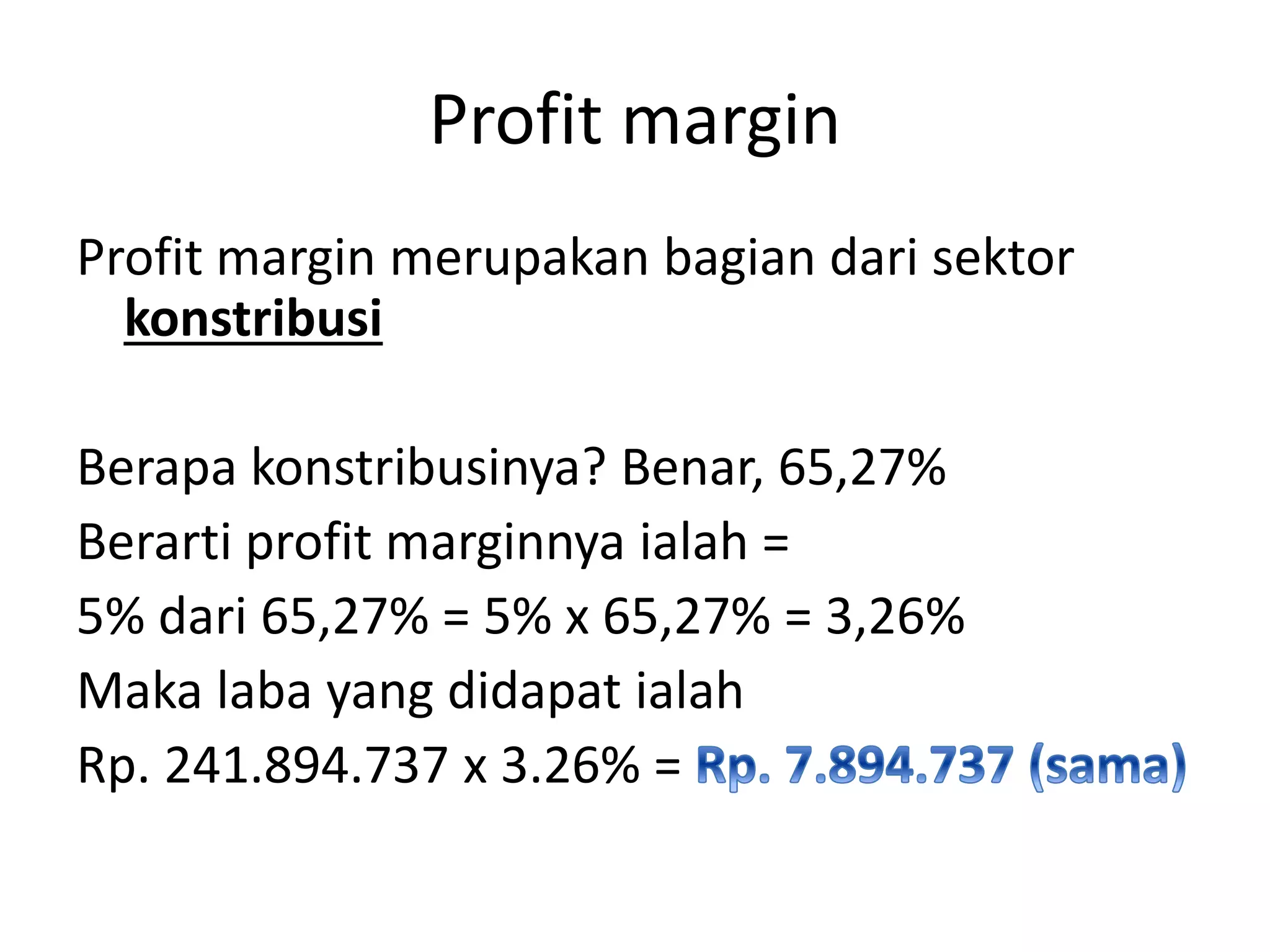

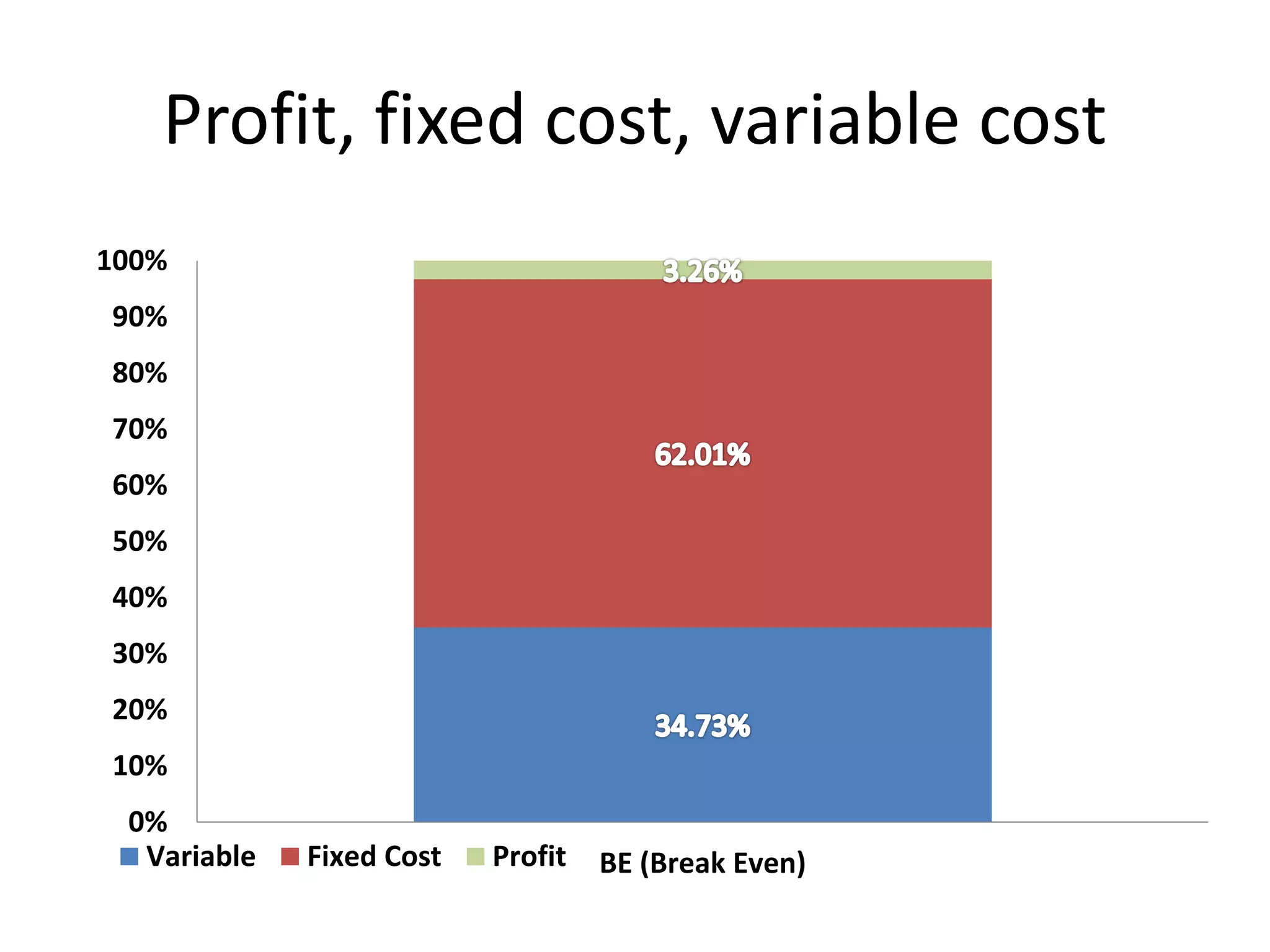

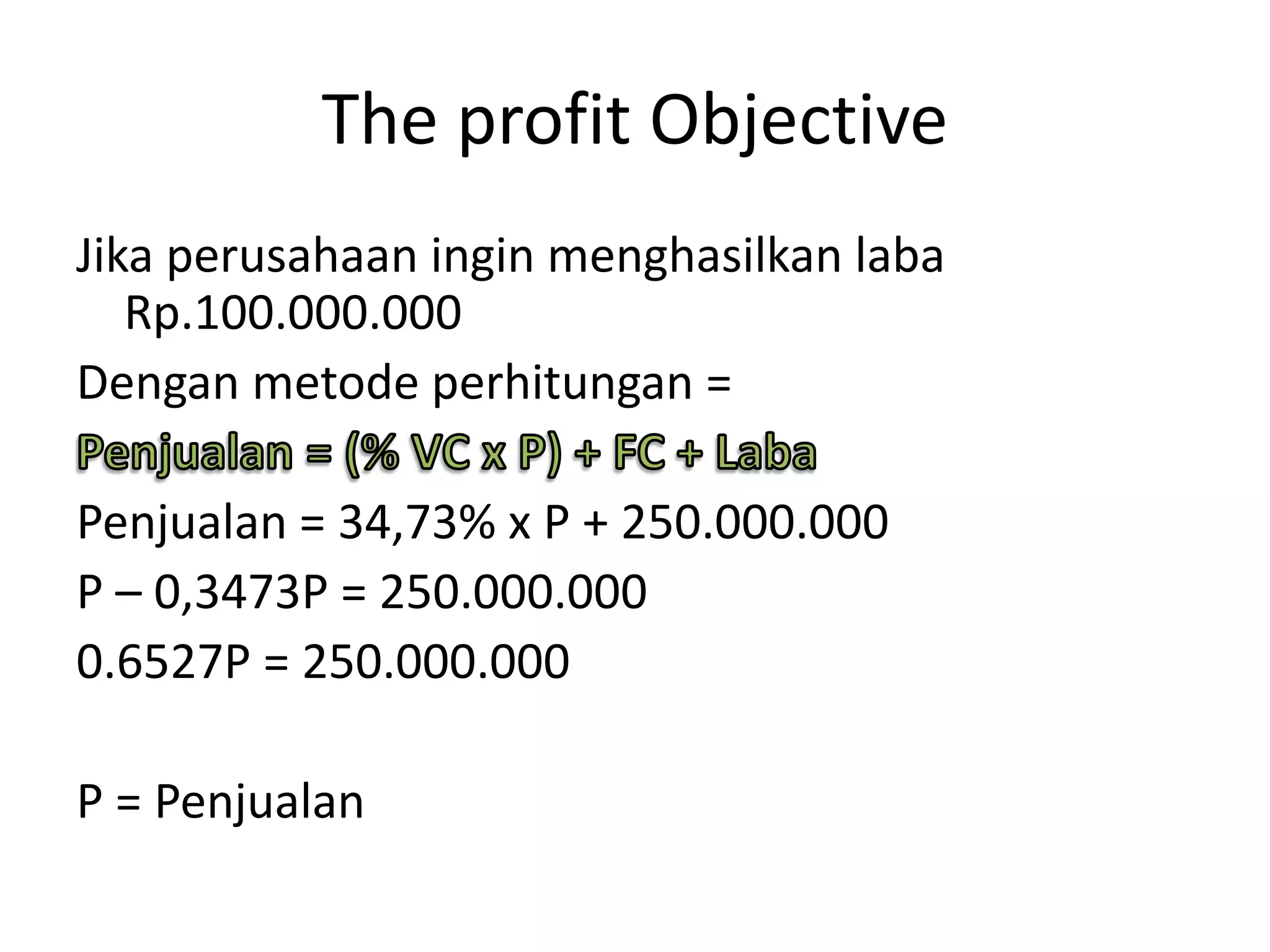

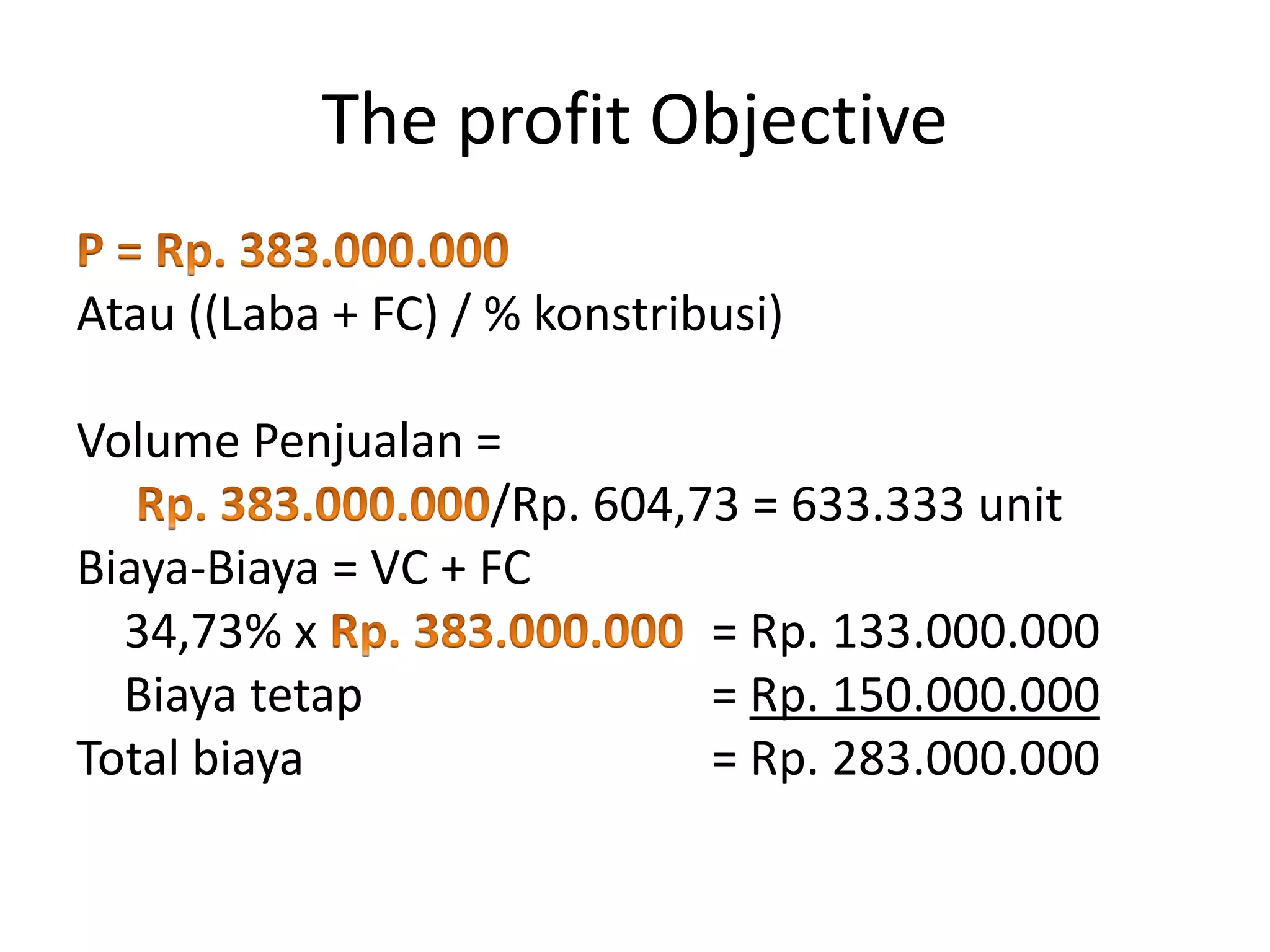

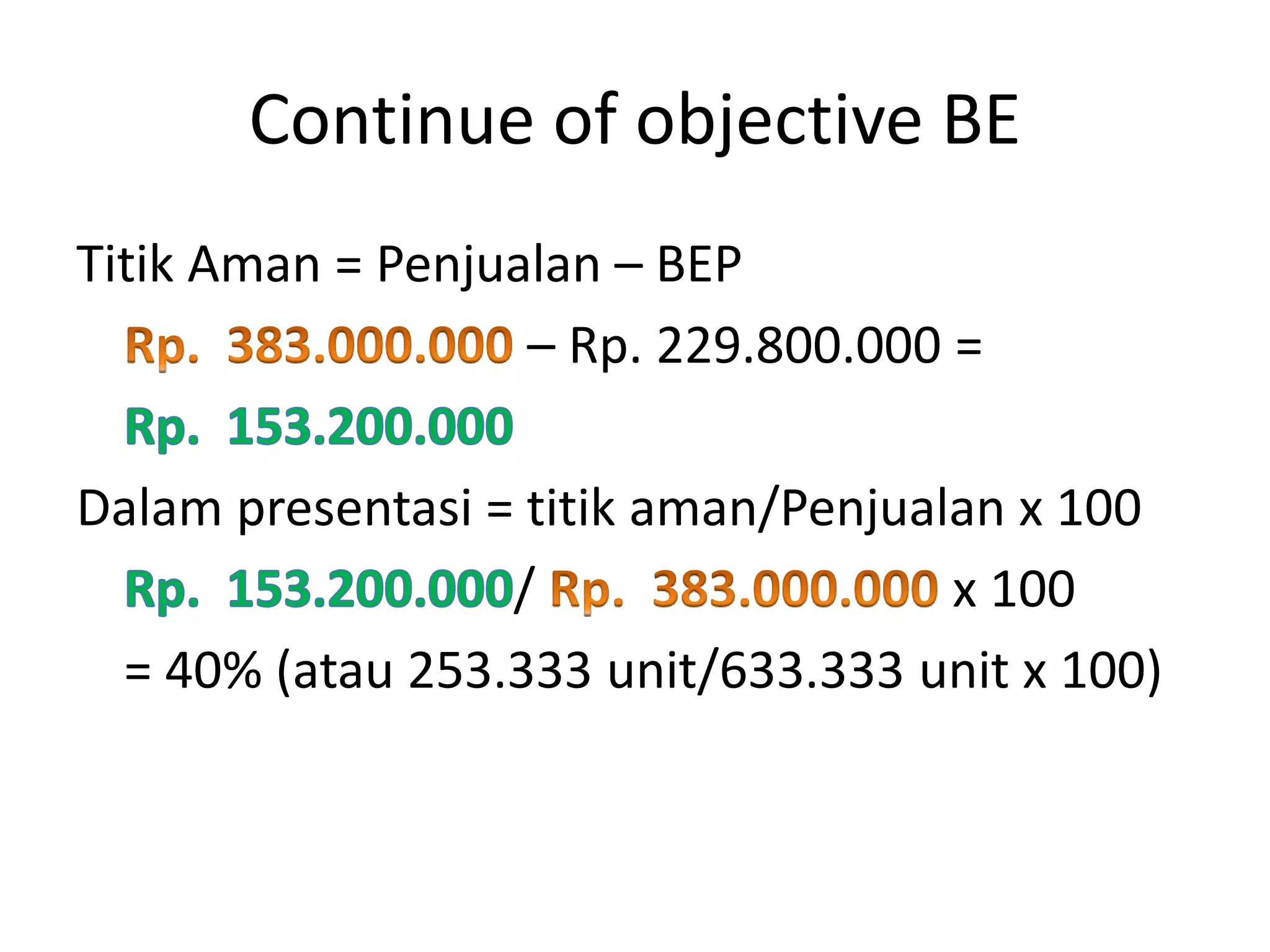

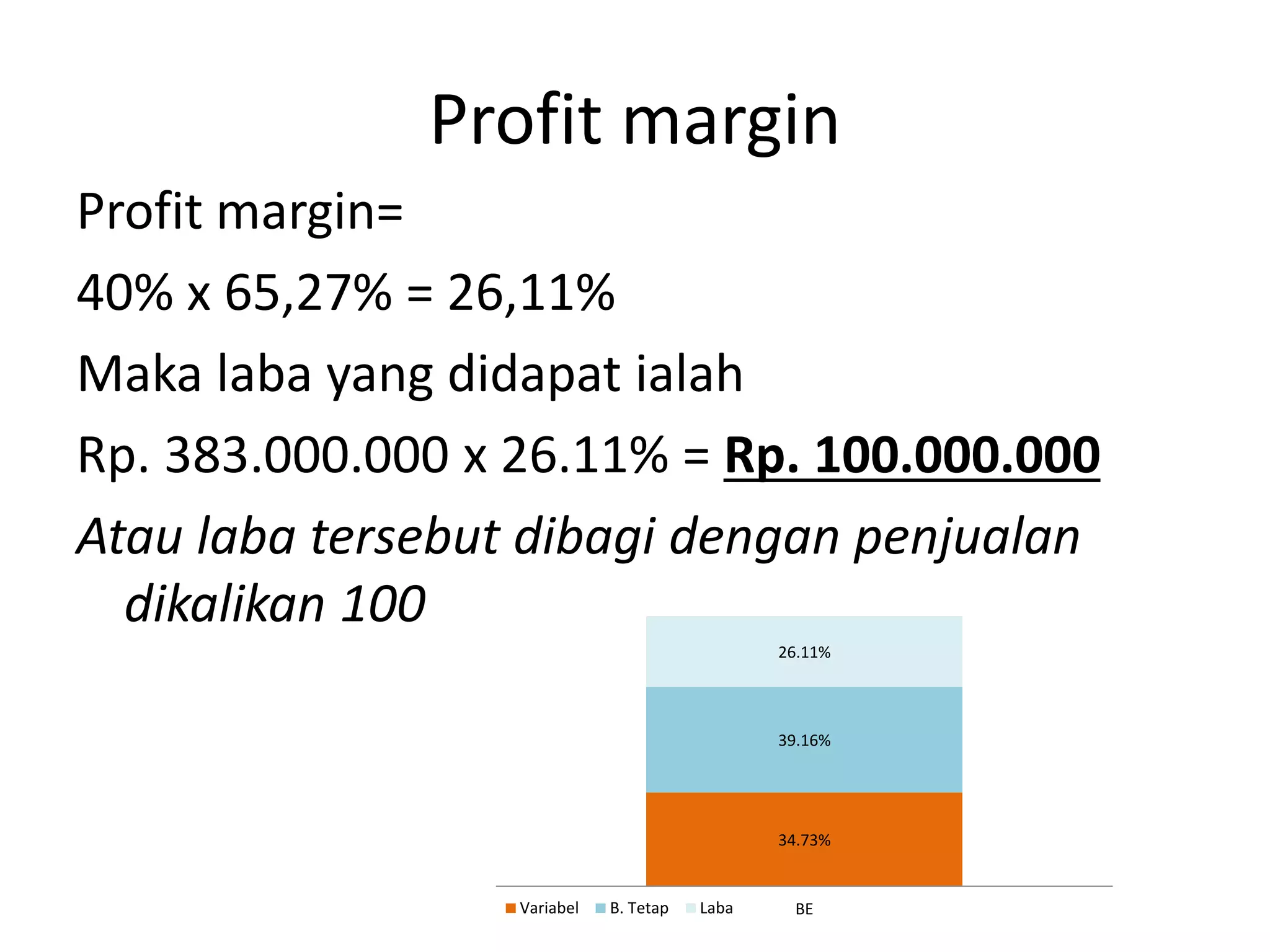

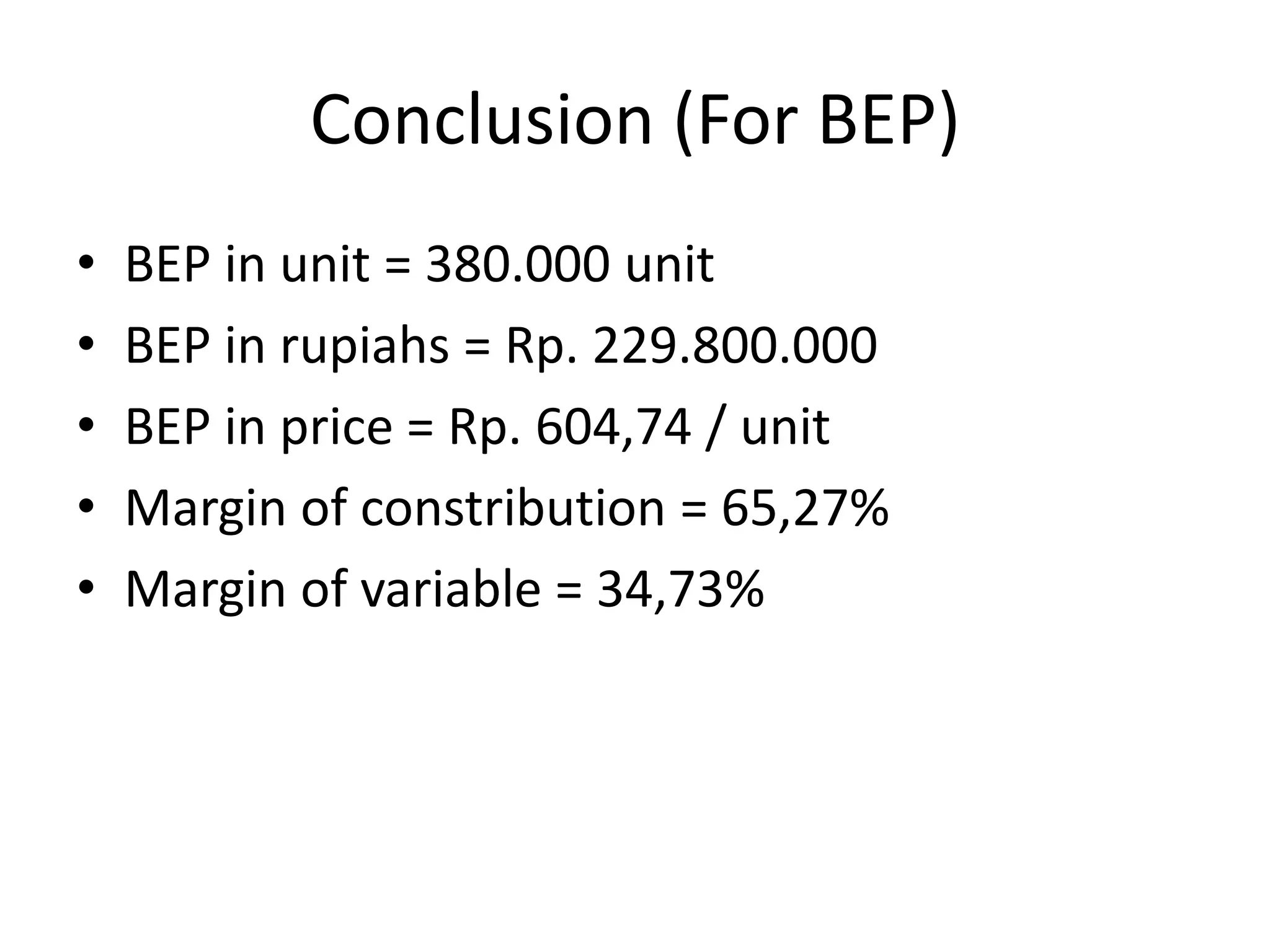

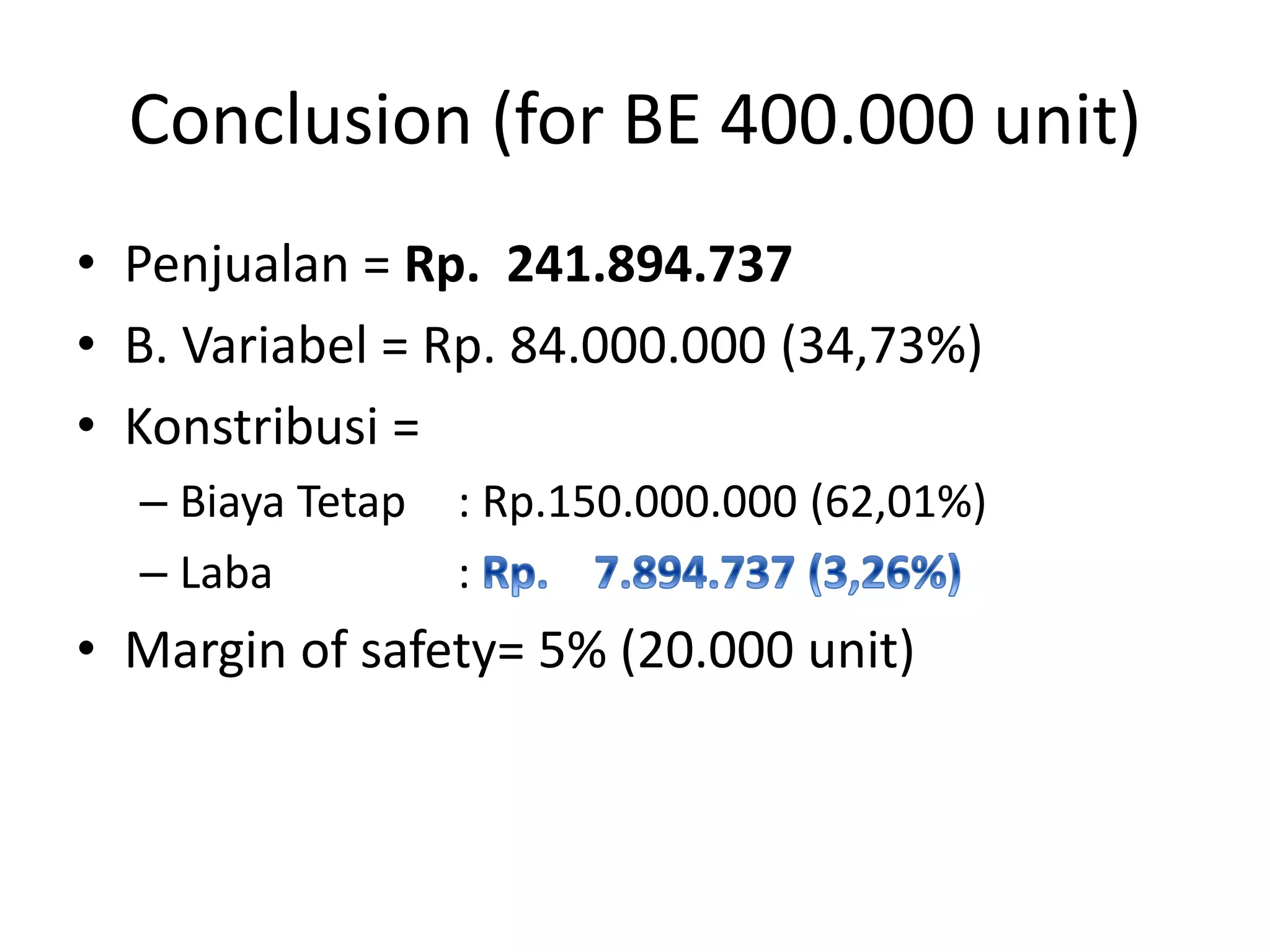

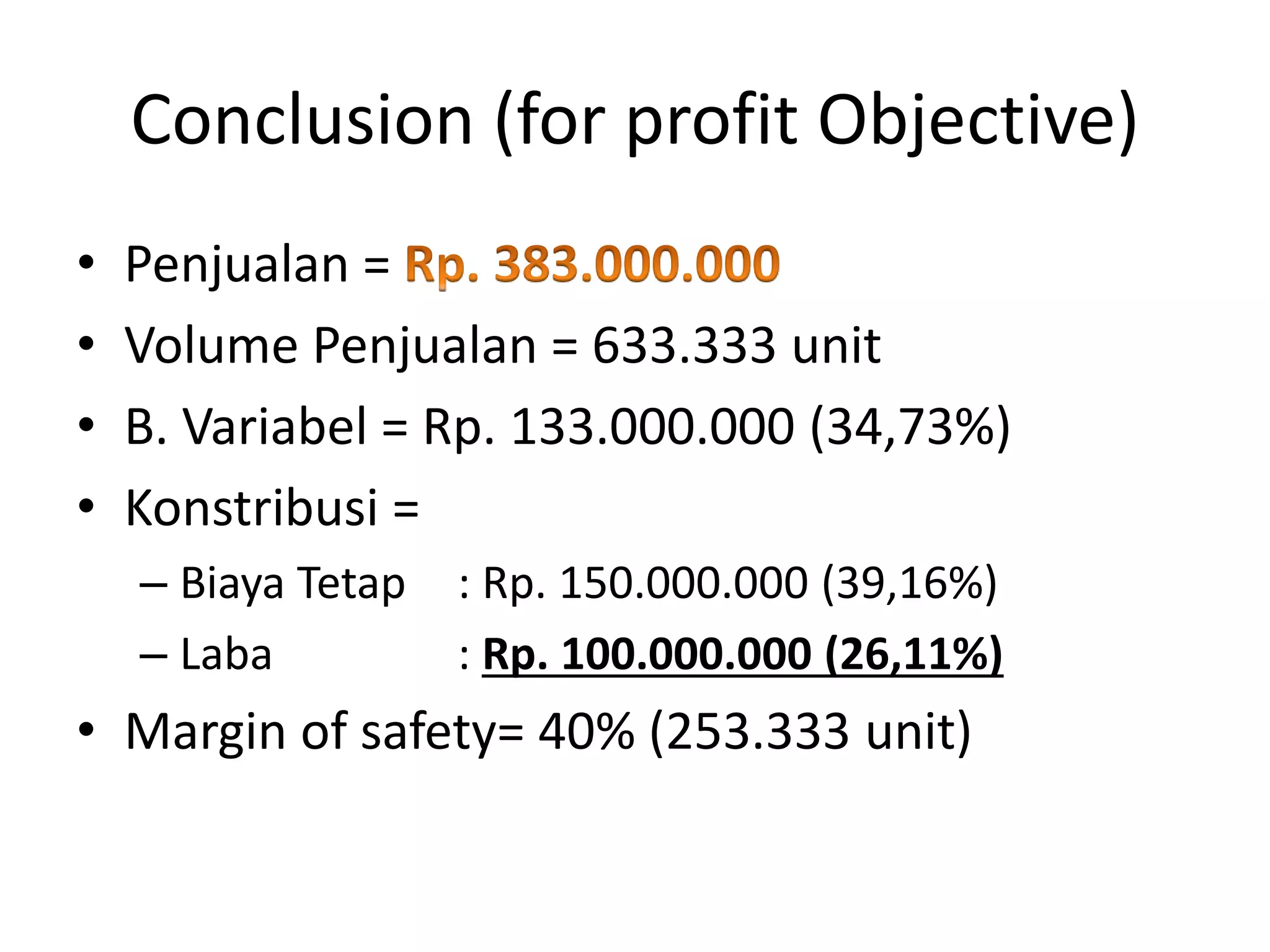

The document provides a detailed analysis of break-even points (BEP) and profit calculations for a manufacturing company producing bricks. Key metrics include BEP in units (380,000), BEP in rupiah (Rp. 229,800,000), and BEP price per unit (Rp. 604.74), along with variable and fixed costs. It also outlines a profit objective aiming for Rp. 100,000,000 with a sales volume of 633,333 units, demonstrating the relationships between costs, profits, and margins.