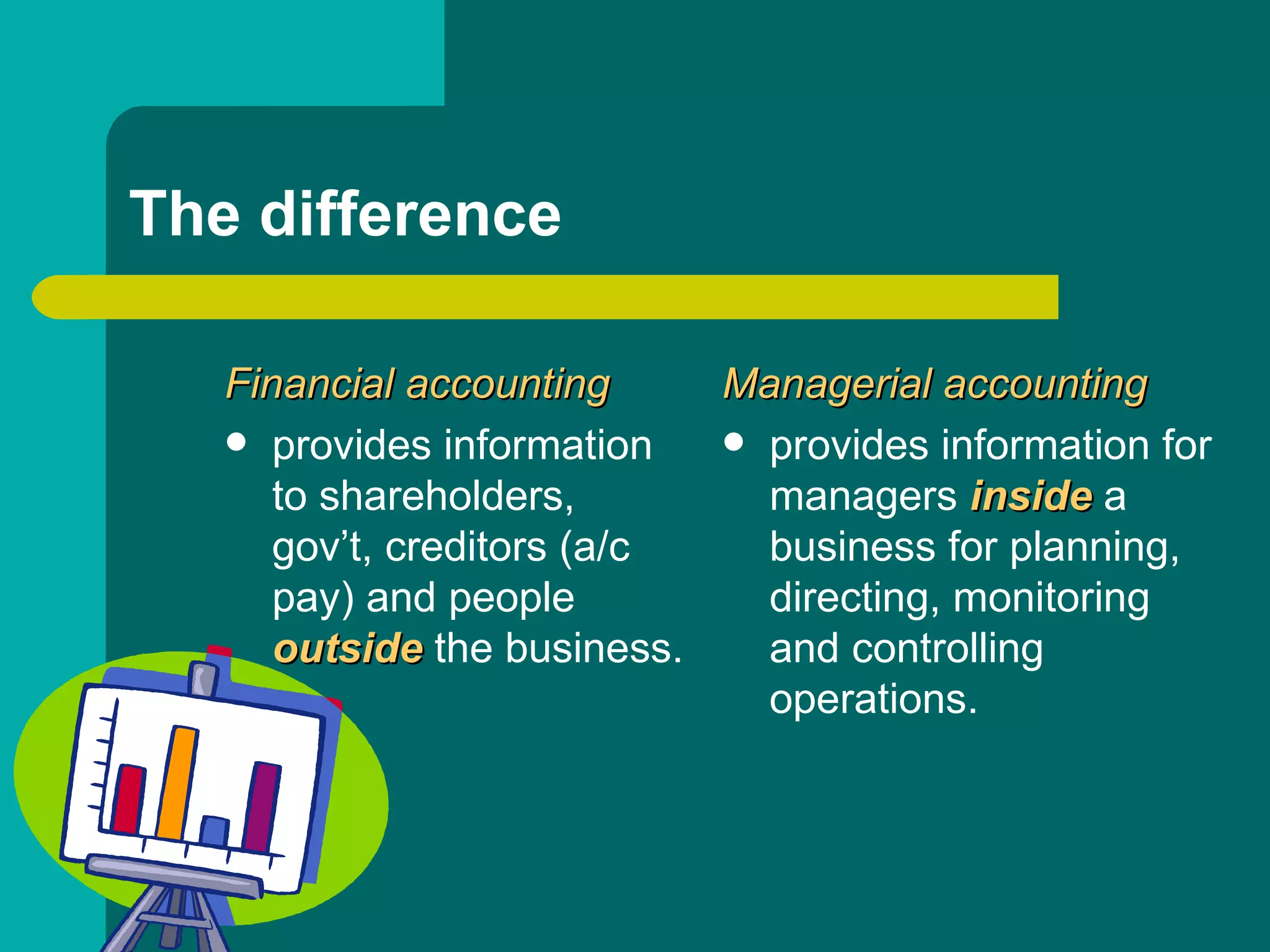

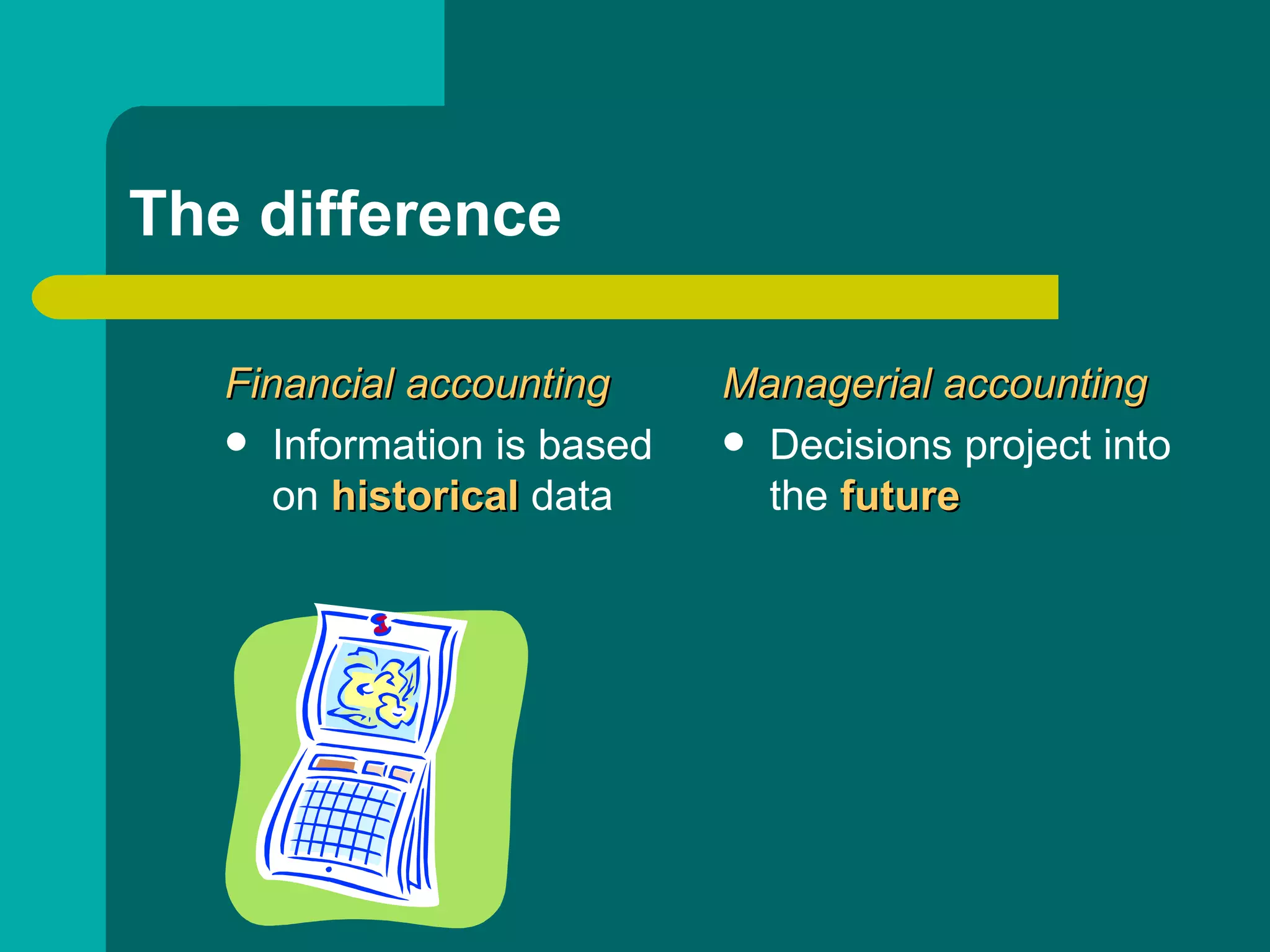

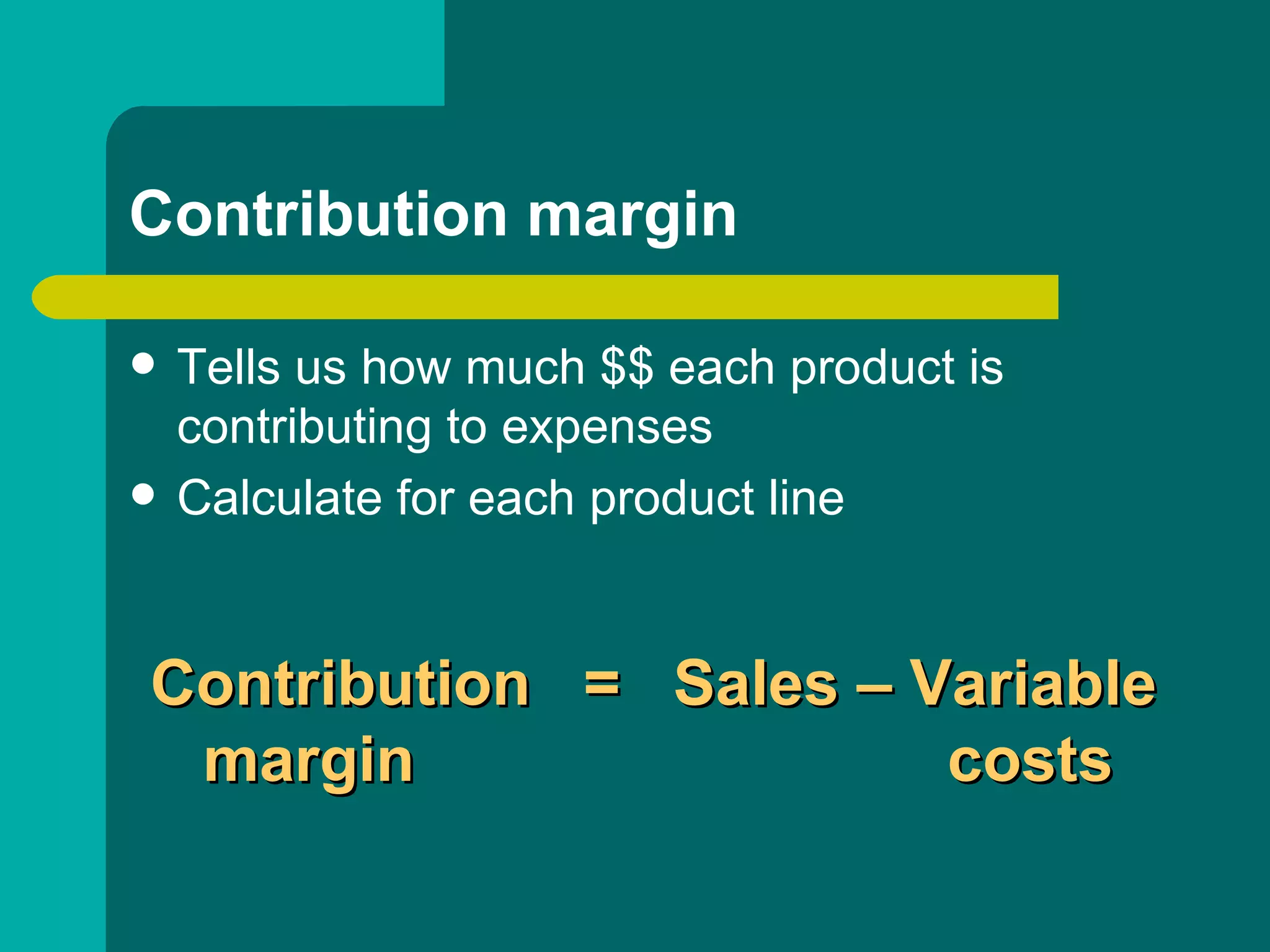

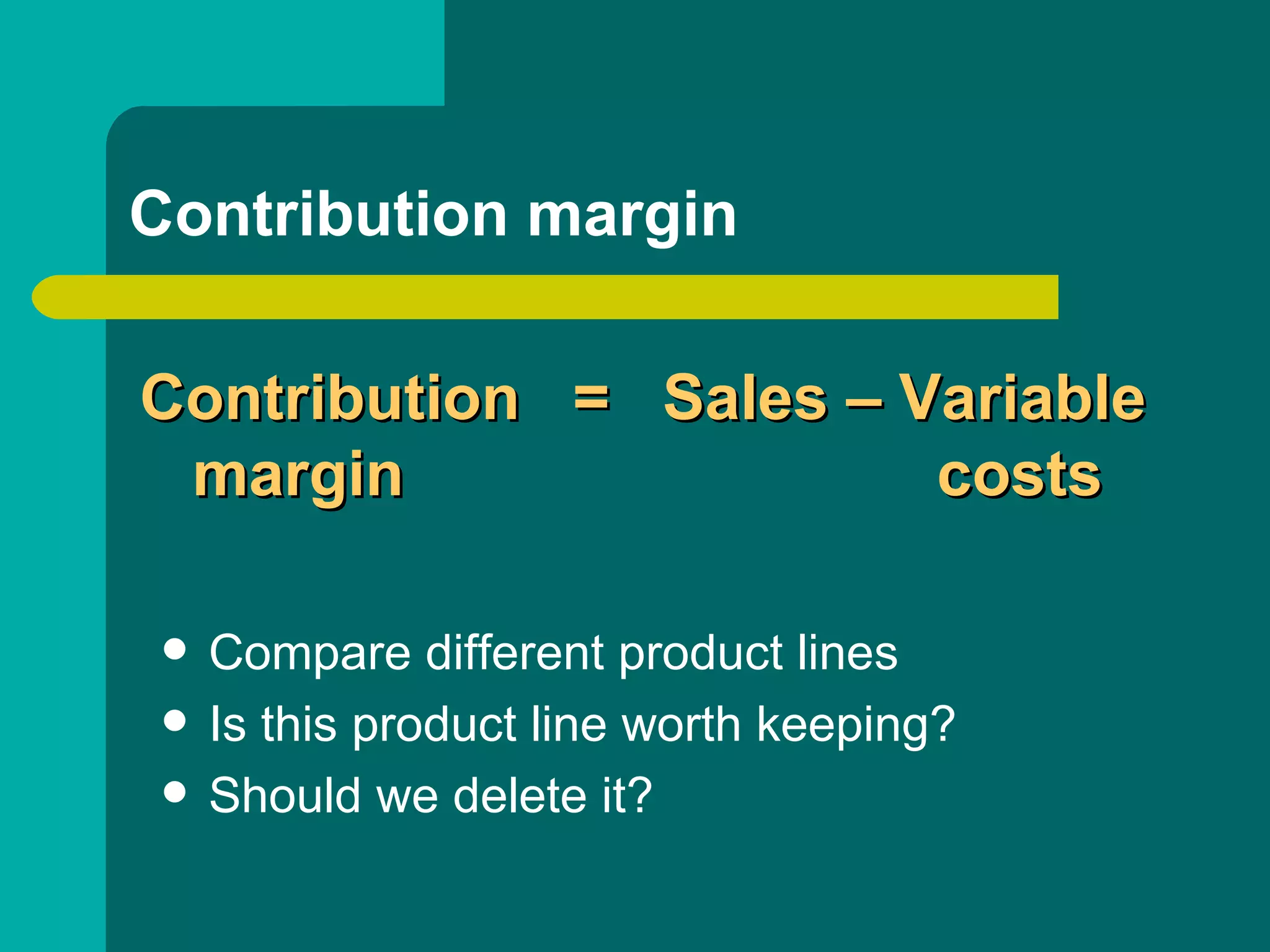

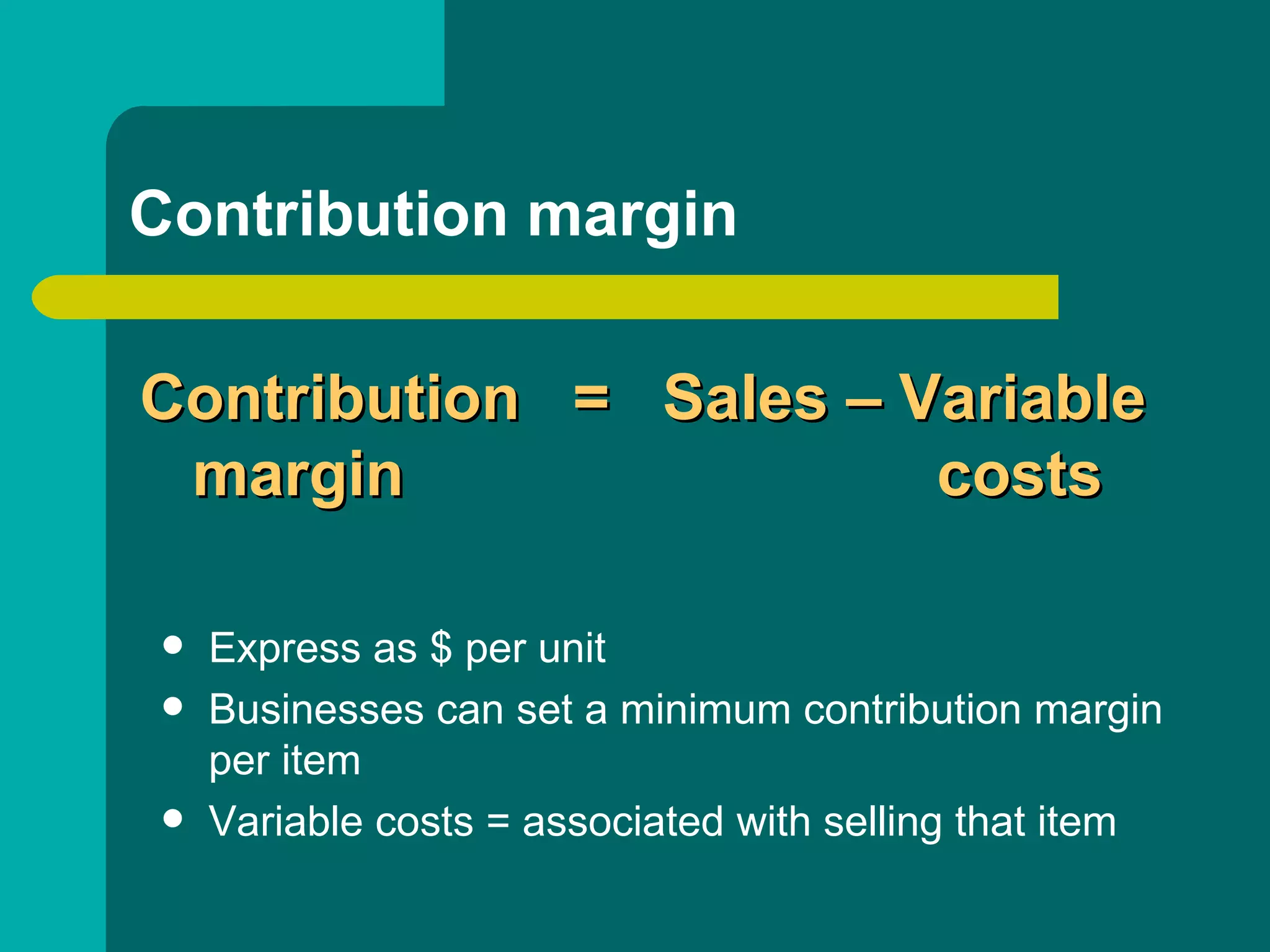

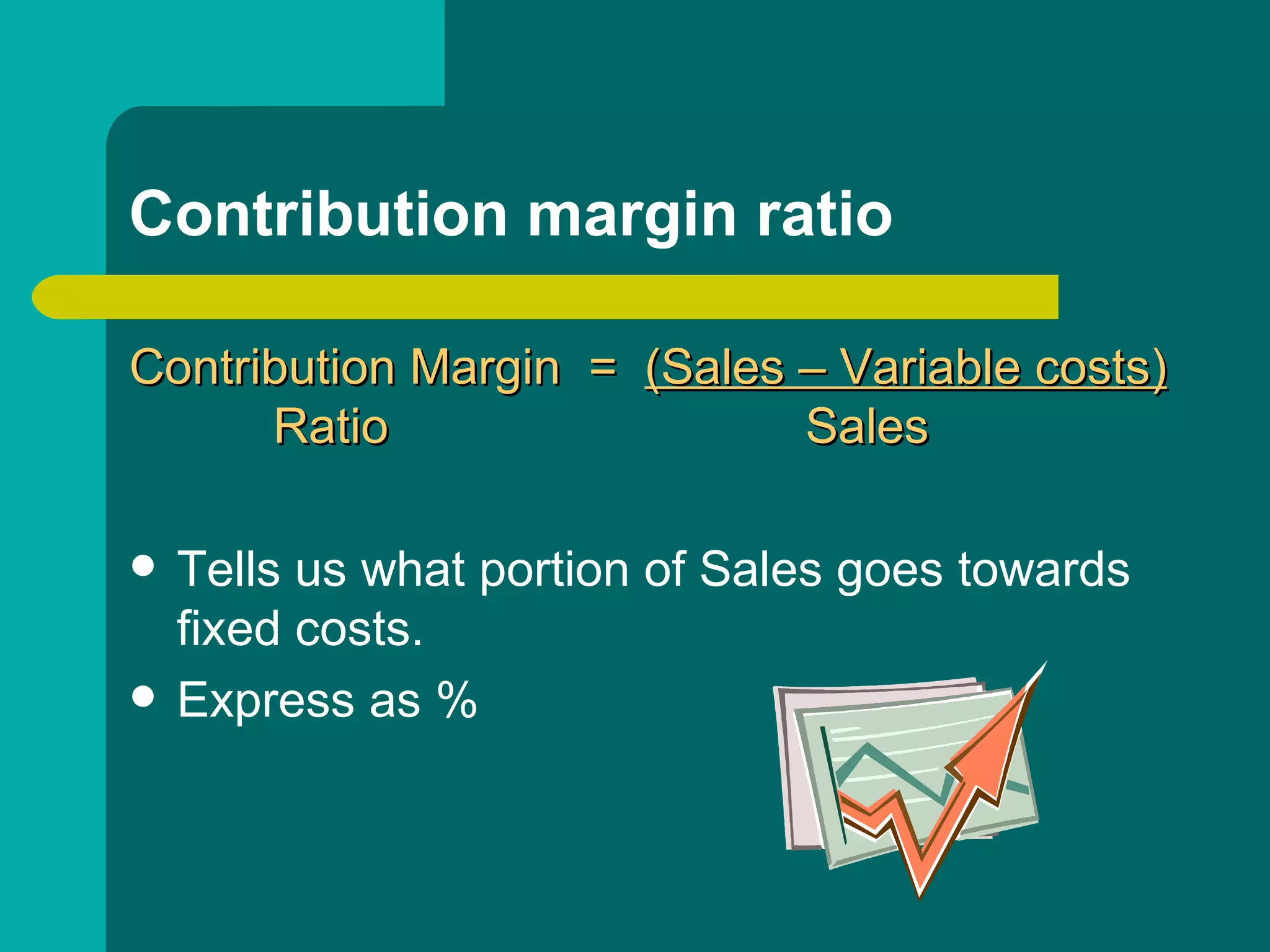

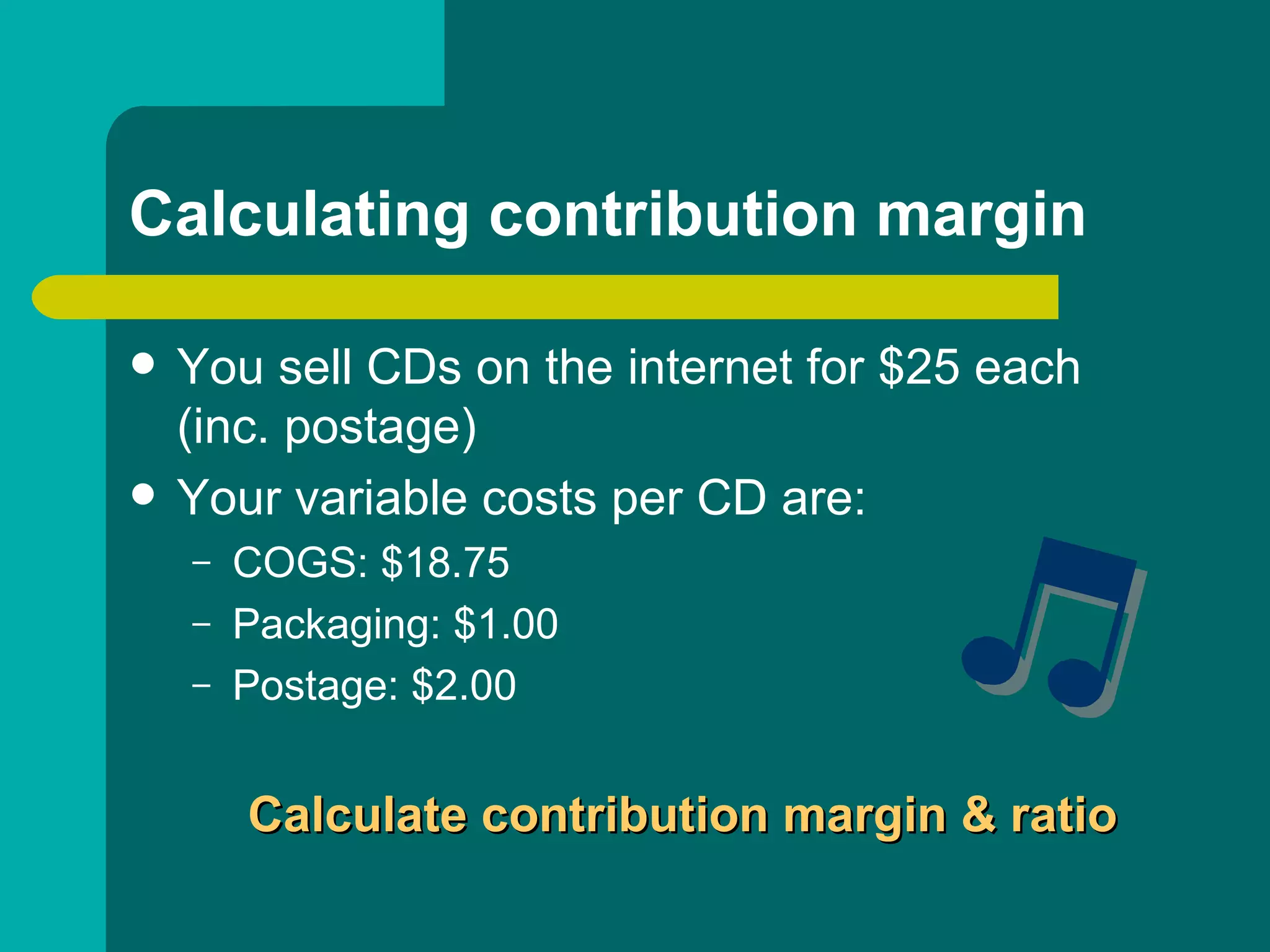

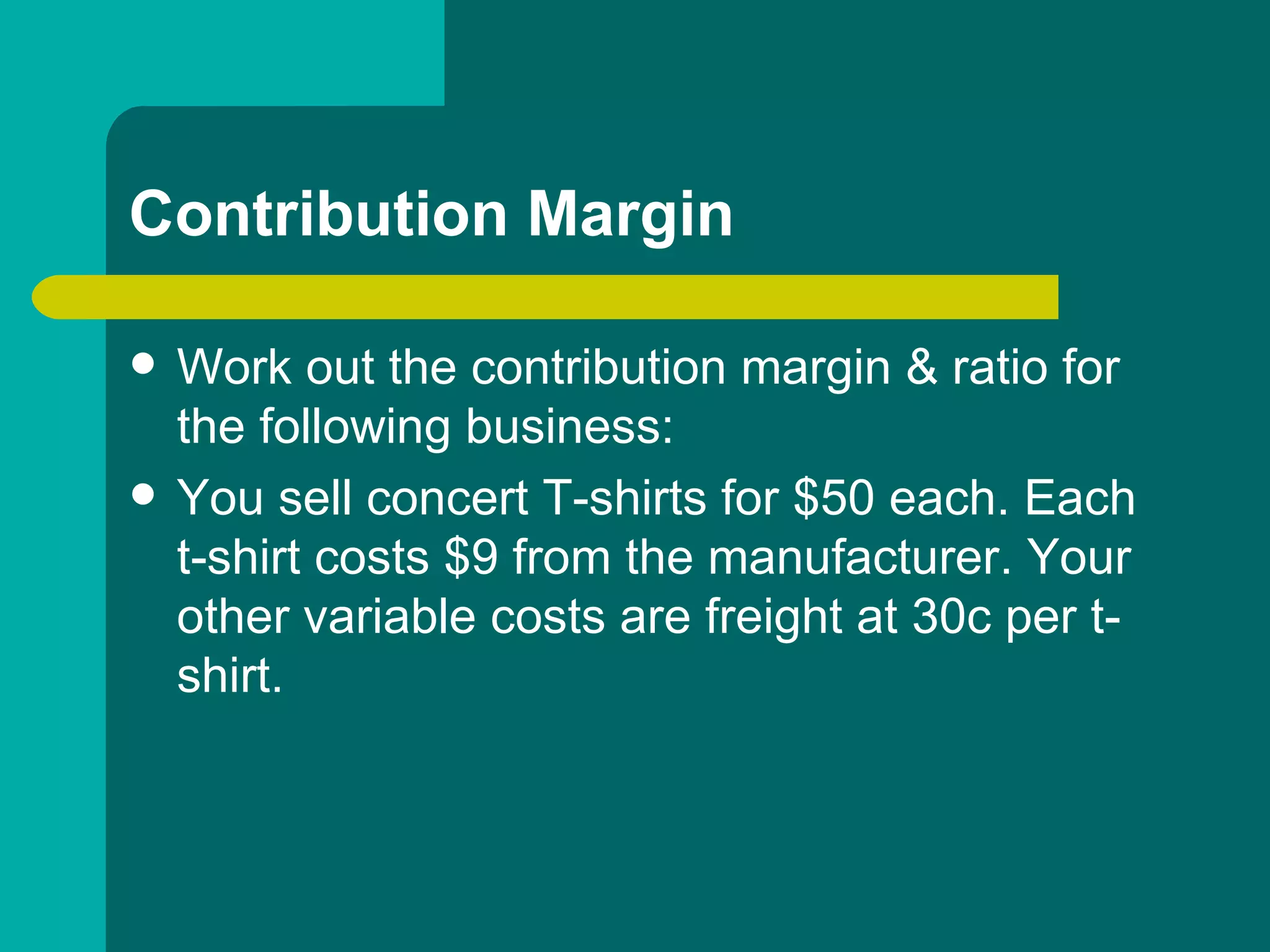

This document discusses the key differences between managerial accounting and financial accounting. Managerial accounting provides internal information for managers to use for planning, directing, monitoring and controlling operations, while financial accounting provides external information to stakeholders. It also discusses decision-making tools in managerial accounting like contribution margin and break-even analysis which are used to evaluate product lines and determine the sales volume needed to cover total costs.