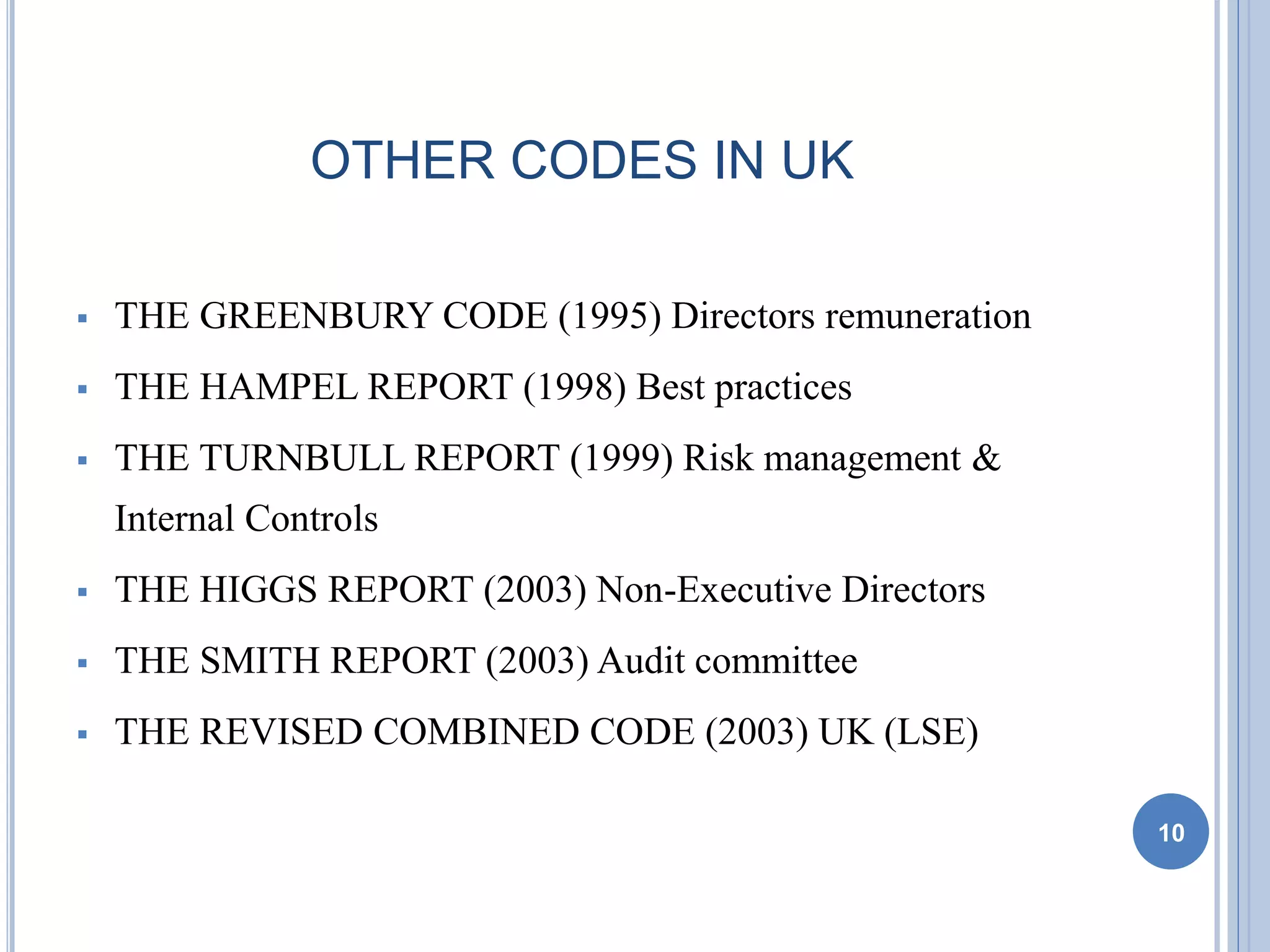

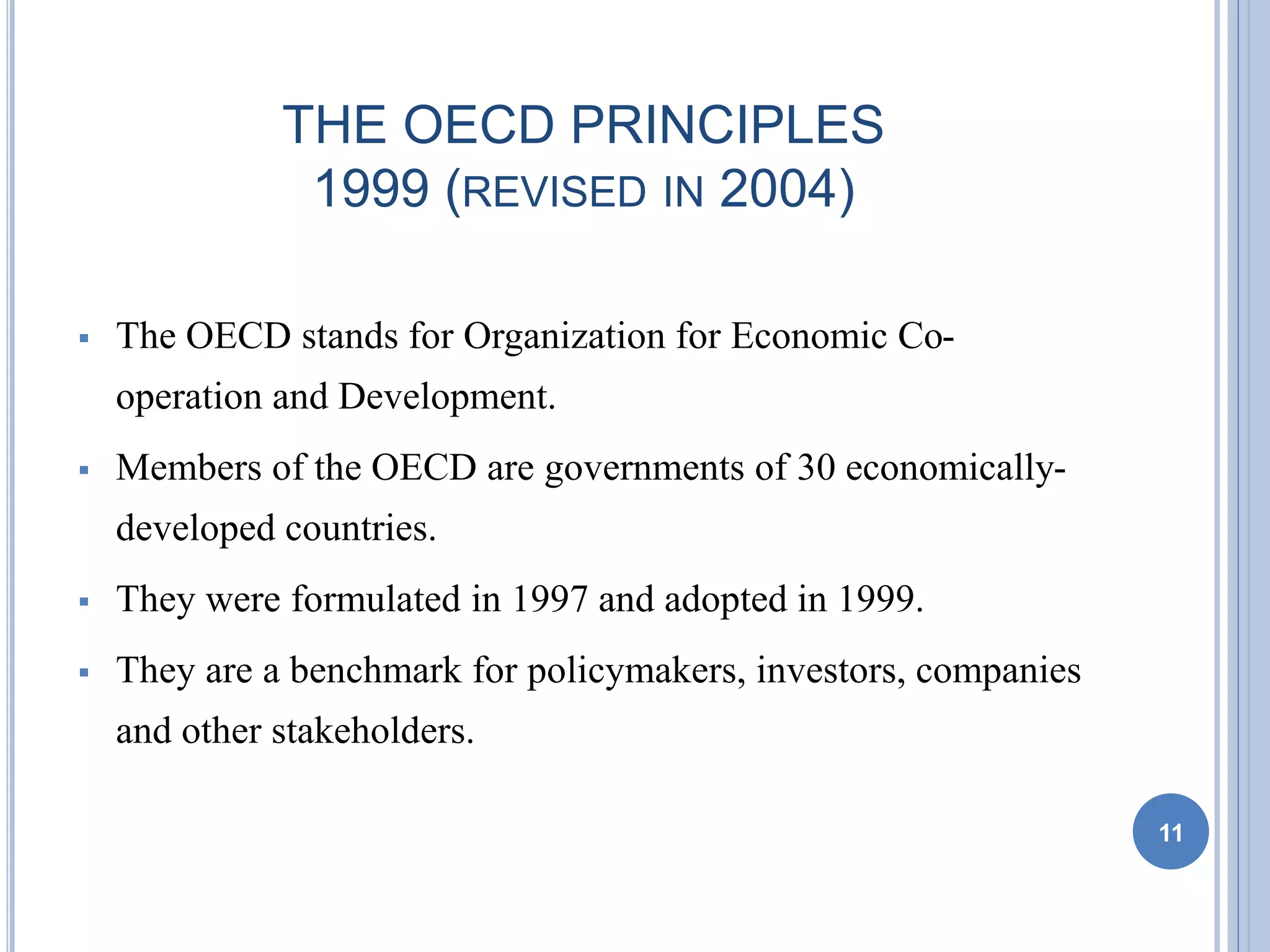

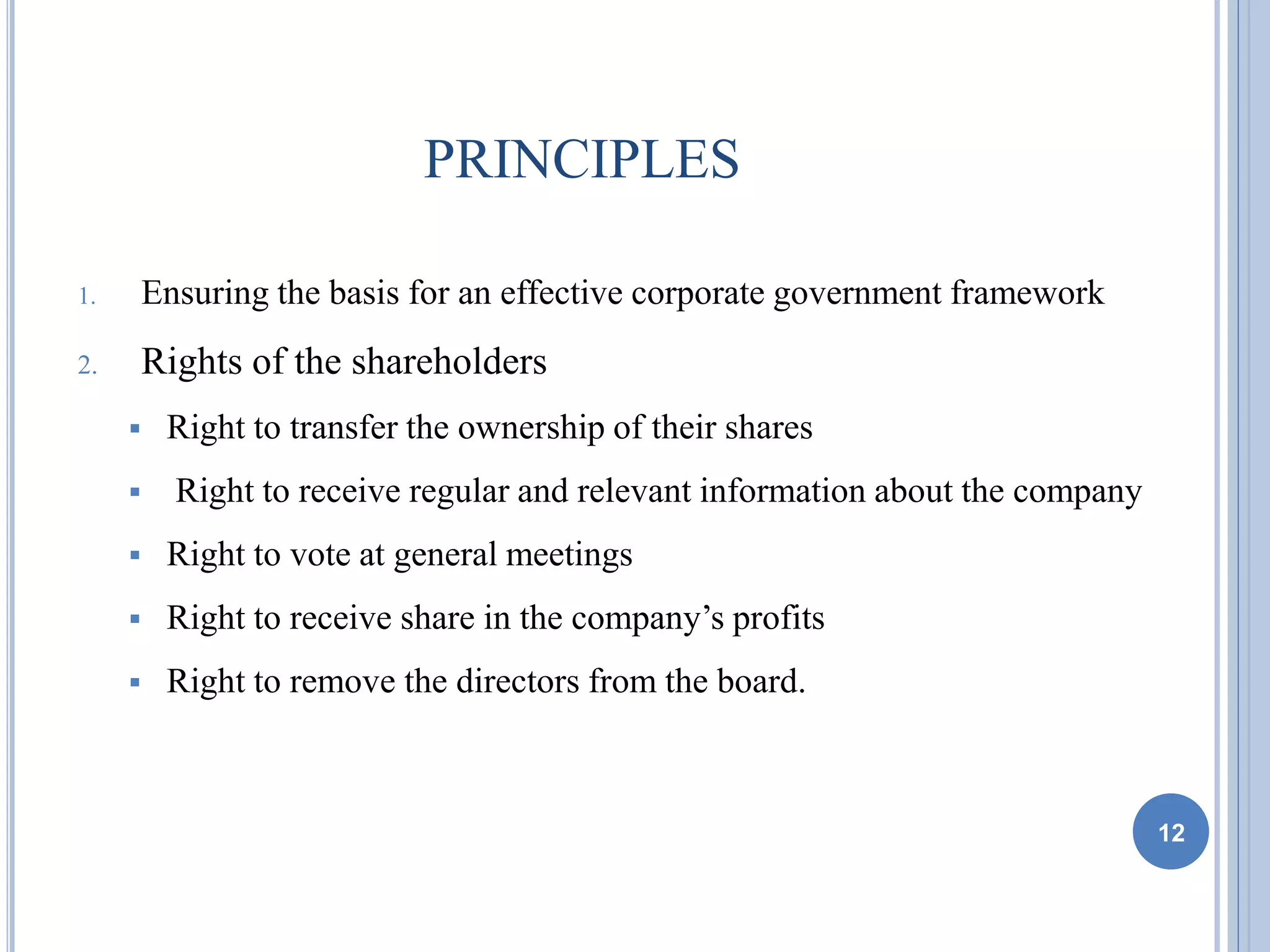

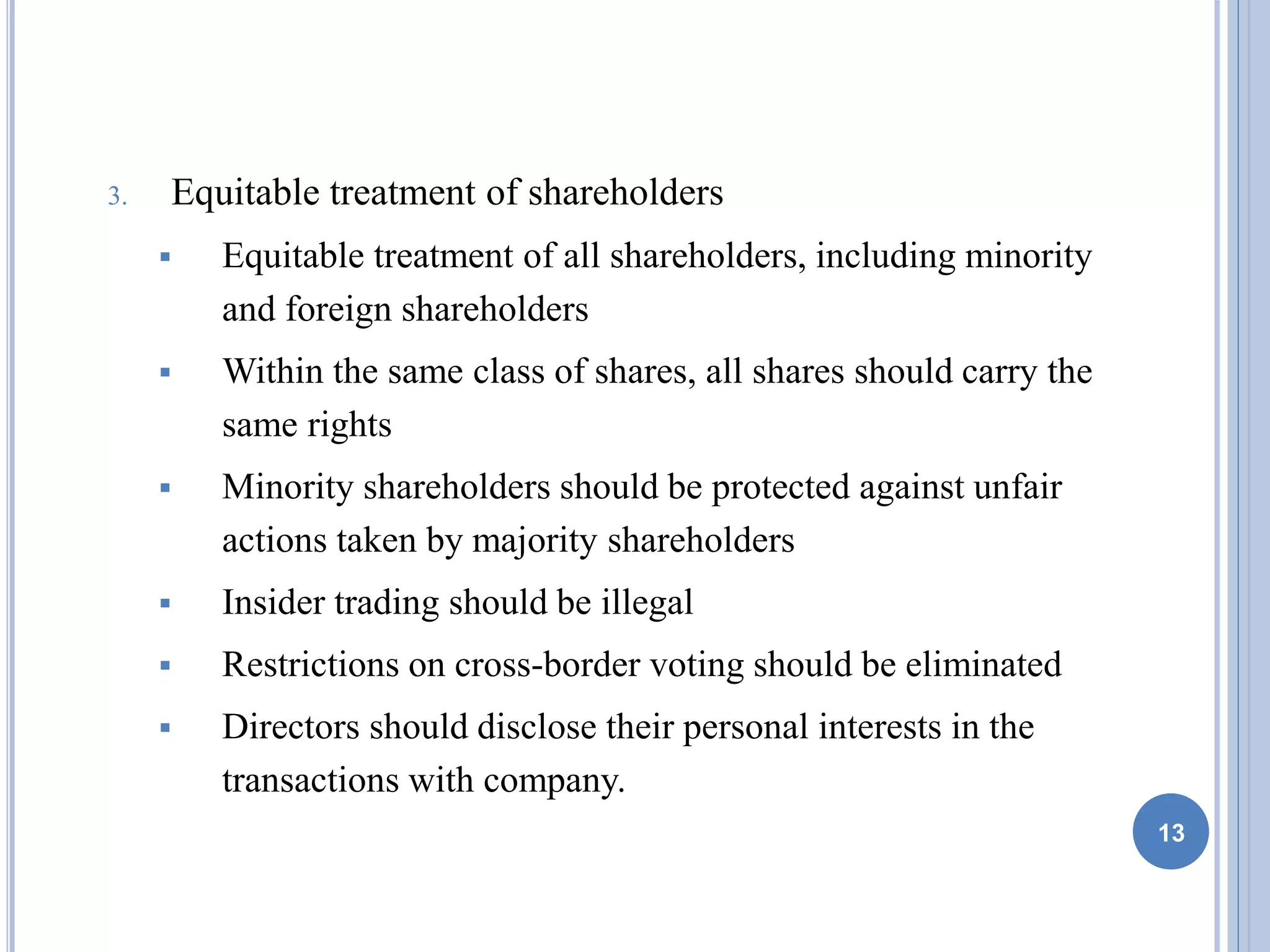

The document summarizes several major codes on corporate governance from the UK and internationally. It begins by discussing the 1992 Cadbury Committee report from the UK, which was commissioned after several business failures and established a Code of Best Practice for board structure and responsibilities. It also made recommendations regarding auditors and shareholder rights. The OECD later issued principles in 1999 focused on shareholder rights, equitable treatment, stakeholder rights, transparency and board responsibilities. Additionally, the US passed the Sarbanes-Oxley Act in 2002 to increase investor confidence through provisions regarding certification of financial statements, assessment of internal controls, restrictions on loans to executives, protection of whistleblowers and establishment of audit committees.