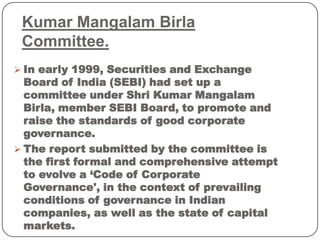

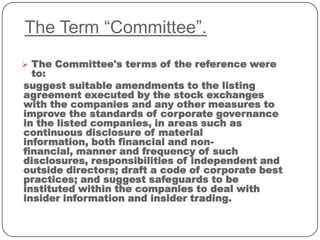

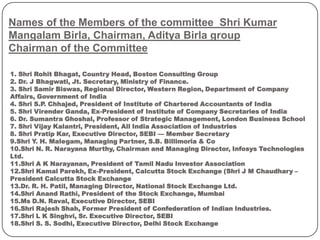

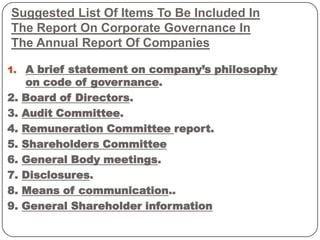

The Kumar Mangalam Birla Committee was formed by SEBI in 1999 to develop a code of corporate governance for Indian companies. The committee submitted recommendations for both mandatory and non-mandatory guidelines. Key mandatory recommendations included composition of boards, establishment of audit committees, and disclosure requirements. The recommendations were implemented through Clause 49 of the listing agreement, which came into effect in 2005 and aimed to improve governance standards for listed companies.