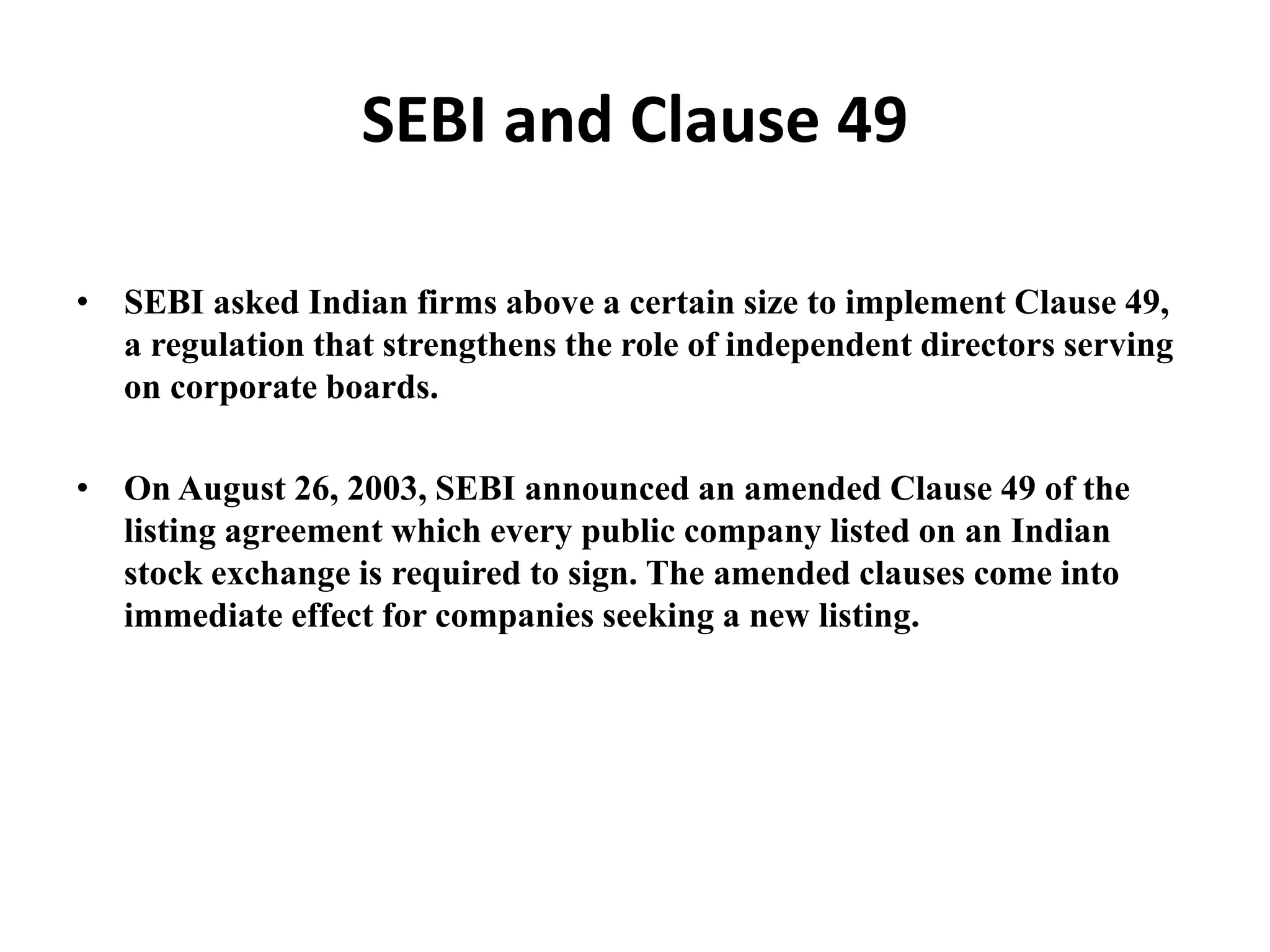

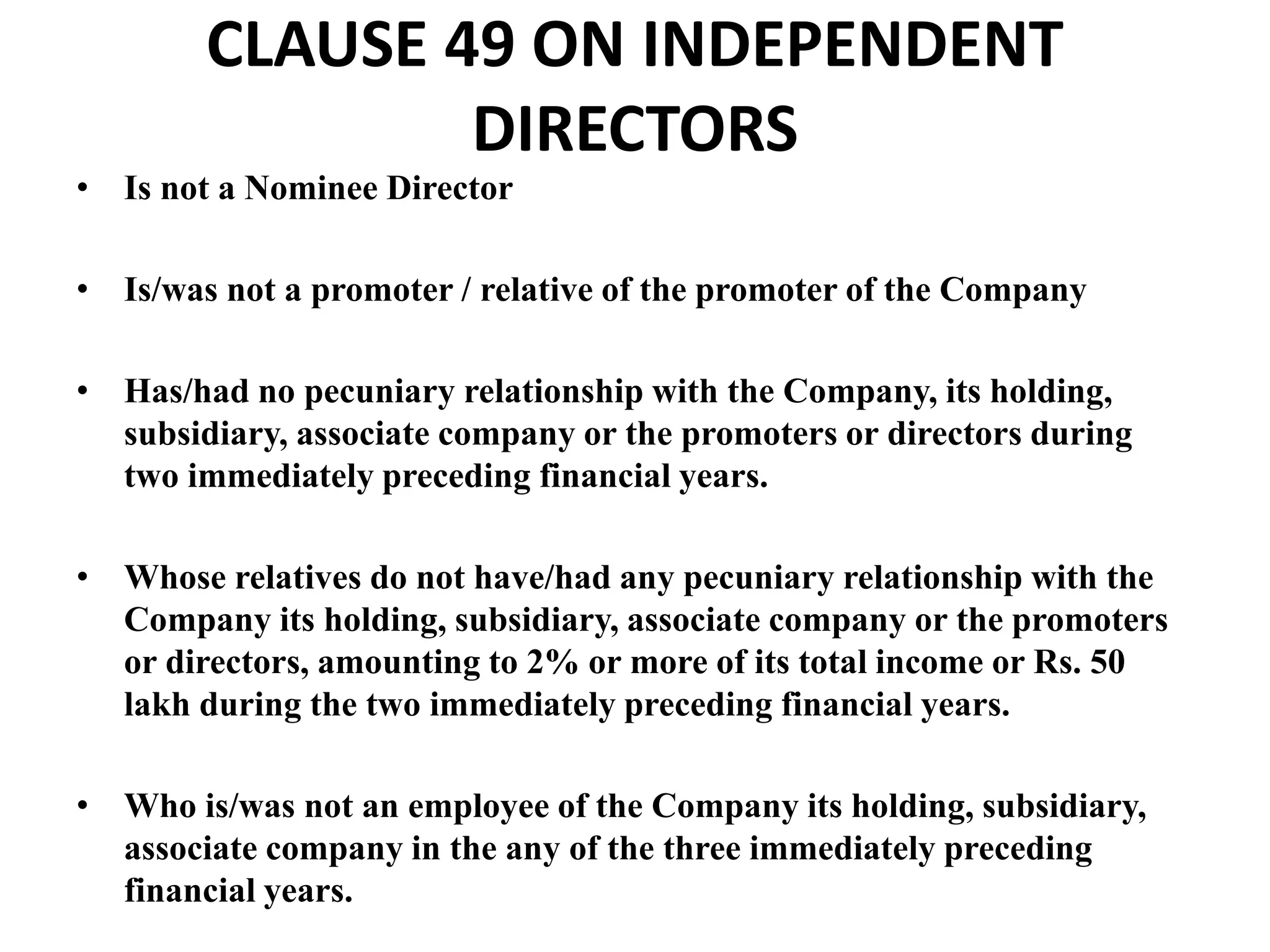

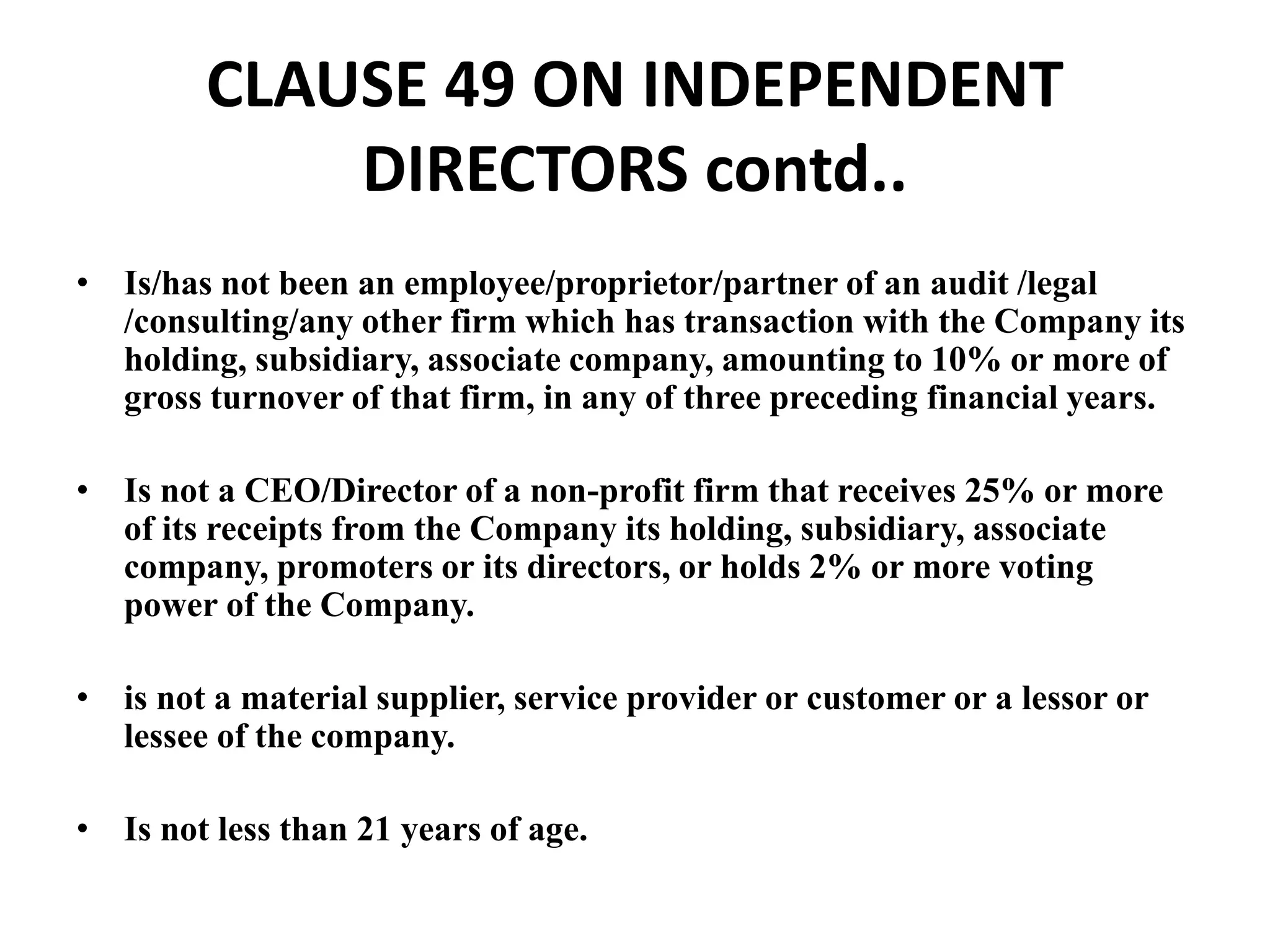

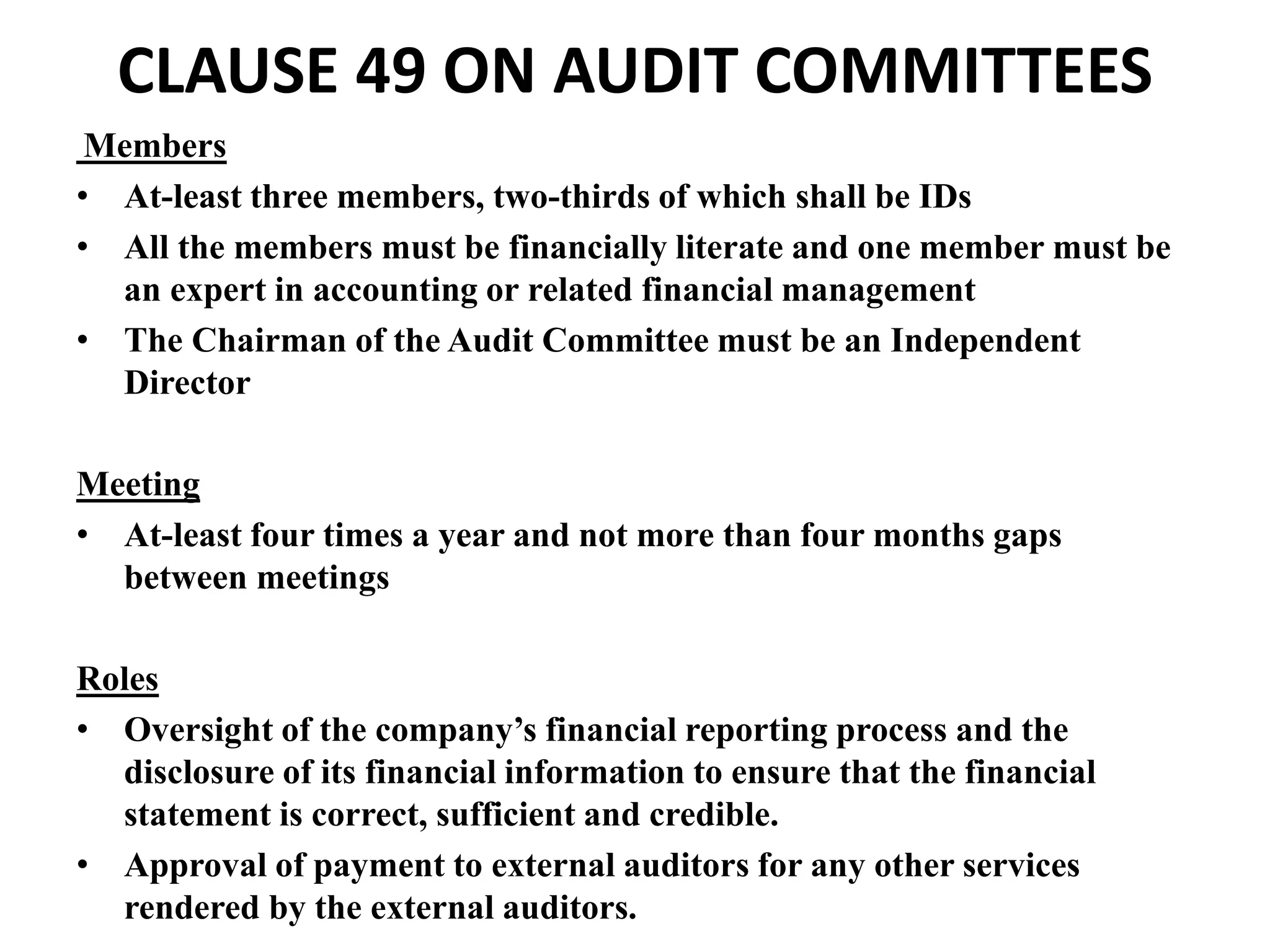

Corporate governance aims to balance the interests of various stakeholders. SEBI was established in 1988 to protect small investors and regulate stock markets in India. In 2003, SEBI announced an amended Clause 49 which prescribes corporate governance norms that listed companies must follow. Key aspects of Clause 49 include requirements regarding board composition and director independence, related party transactions, audit committees, and disclosure of financial/other information.