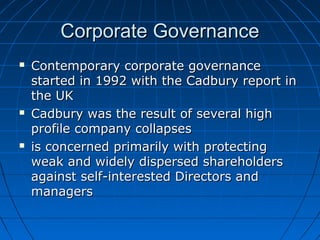

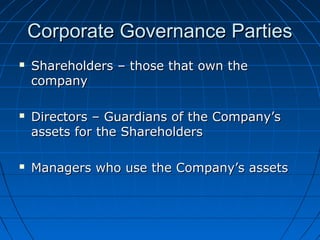

Corporate governance concerns protecting shareholders from self-interested directors and managers, primarily through establishing accountability, fairness, transparency and independence. It originated from the 1992 Cadbury Report in response to high-profile company collapses in the UK and is now a global practice, though its application varies between countries and types of organizations. Effective corporate governance can provide companies benefits like lower costs of capital despite weak legal environments through establishing strong internal governance practices.