Class XII Economics Study Material

•Download as DOC, PDF•

2 likes•3,351 views

This document provides a syllabus and study material for the Economics class of Class XII in 2014-15. It outlines the course content, which is divided into two parts - Introductory Microeconomics and Introductory Macroeconomics. The Microeconomics section covers topics such as consumer behavior, producer behavior, market structures, and the introduction lesson. The introduction lesson defines key economic concepts such as scarcity, choice, opportunity cost and presents the production possibility curve. It also describes the three basic economic problems of what to produce, how to produce and for whom to produce. The document provides sample questions for students and a test paper with questions from the introduction lesson.

More Related Content

What's hot

What's hot (20)

Similar to Class XII Economics Study Material

Similar to Class XII Economics Study Material (11)

More from FellowBuddy.com

More from FellowBuddy.com (20)

Recently uploaded

Recently uploaded (20)

Class XII Economics Study Material

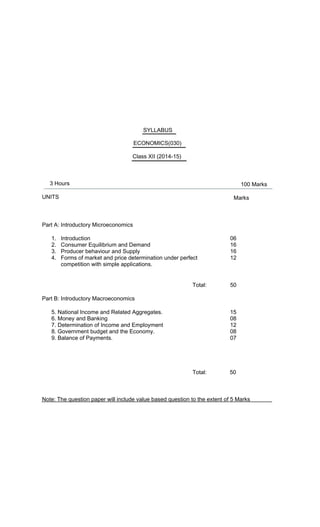

- 1. SYLLABUS ECONOMICS(030) Class XII (2014-15) 3 Hours UNITS 100 Marks Marks Part A: Introductory Microeconomics 1. Introduction 06 2. Consumer Equilibrium and Demand 16 3. Producer behaviour and Supply 16 4. Forms of market and price determination under perfect 12 competition with simple applications. Part B: Introductory Macroeconomics Total: 50 5. National Income and Related Aggregates. 15 6. Money and Banking 08 7. Determination of Income and Employment 12 8. Government budget and the Economy. 08 9. Balance of Payments. 07 Total: 50 Note: The question paper will include value based question to the extent of 5 Marks

- 2. STUDY MATERIAL (MICRO ECONOMICS) UNIT-1 (MARKS-6) INTRODUCTION GIST OF THE LESSON Meaning of economics: Economics is the science which studies human behavior as a relationship between ends and scarce means which have alternative uses. Meaning of an economy:-Economy is the system which provides people the means to work and earn a living. Or it is a frame work within which economic activities like production, consumption, and capital formation are undertaken. Meaning of scarcity:-It is defined as excess of demand over available supply, i.e, demand of resourses>supply of resources. Economic problem:-The problem of making a choice is called economic problem. Causes of economic problem:- It arises due to 1) Scarcity of resources 2) Unlimited human wants 3) Resources can be put to alternative uses Scarcity and Choice go together:-Scarcity and choice are not separable because resources are limited or scarce and the problem of choice arises due to it. Economising of resources:-Our wants are unlimited and resources are limited, so we have to use the resources fully and efficiently. It means that resources should be best utilized. This is called economizing of resources. Central Problems of an Economy:-Central problem of an economy is Allocation of resources.The three central problems relating to allocation of resources are:- 1) What to produce:-The problem of what to produce and in what quantity is the first basic or central problem. It is related to the selection of goods. Our resources are limited. So first problem that we have to face is which goods and services are to be produced e.g consumer goods or capital goods, war time or peace time goods. After the decision has been taken the quantities of these goods should also be decided. 2) How to produce:- The second important problem is the problem of choice of technique of production. That means we have to decide whether to use labour intensive technique(it uses more of labour than capital) or capital intensive technique(it uses more of capital than labour).How ever the choice of technique depends on the objective of the producer.The producer can use

- 3. labour intensive ,capital intensive or both technique of production.The main aim is to use the efficient technique of production. 3) For whom to produce:-This is also called the problem of distribution of National Income among the factor of production. For whom to produce is actually the problem of determining wage rate for the use of labour ,rent for the use of land, interest for the use of capital and profits for the producer to ensure equitable distribution of income and welfare in the society. Production possibility curve or frontier A production possibility curve/ frontier shows different combinations of two commodities that can be produced by an economy with the full use of given resources and technology. (i)Normally, the production possibility curve is concave to the origin. It is because of increasing marginal opportunity cost. (ii)A production possibility curve shifts out due to technological progress or increase in thesupply of resources available to an economy or both. Assumptions of PPC-1)Resources are constant. 2)Technology is given. 3)Resources are fully and efficiently used. 4)Production of only two goods can be shown in a PPC. Features of PPC-1) It is downward sloping. 2) It is concave to the origin. PPC can be explained with the help of a schedule

- 5. .

- 6. Shifting/Rotation of PPC a) Change of Resources

- 7. (ii) Change in technology • Efficient technology for the production of Commodity – X: Efficient technology for the production of Commodity – X would mean more production of commodity – X with the same resources. Accordingly, PPC would rotate (NOT SHIFT) as shown in Fig Efficient technology for the production of Commodity – Y : Efficient technology for the production of commodity – Y would mean more production of Y with the same resources. Accordingly, PPC would rotate (NOT SHIFT) as shown in Fig

- 8. Efficient technology for the production of both X and Y: Efficient technology for the production of both X and Y would mean much greater production of both X and Y with the same resources. Accordingly, PPC would shift to the right as shown in Fig.

- 9. Opportunity Cost (Transformation cost)- The opportunity cost of a factor is equal to the value of a factor in its next best alternative use. Eg-A plot of land can be used for wheat and rice production.Production of wheat provides earning of Rs. 1 lakh and Production of rice provides earning of Rs. 90000.If we produce wheat then its opportunity cost is Rs. 90000,which is the value of rice sacrificed. Marginal opportunity cost(or Marginal Rate of Transformation)- The marginal opportunity cost of good X is the rate of sacrifice of the other good, say, Y, per unit increase in the production of good X. Or

- 10. The marginal opportunity cost of good X is defined as the amount / quantity sacrificed of good Y per unit increase in production of good X. Marginal opportunity cost along a PPC. Production of Good X Production of Good Y Marginal Opportunity Cost of Good X in terms of Good Y or amount sacrificed of good Y per unit increase in good X 0 18 - 1 17 1 2 15 2 3 12 3 4 8 4 5 3 5 Note: The above table shows the case of increasing marginal opportunity cost. To produce one more unit of Good X, increasing units of Good Y have to be sacrificed. For example, to produce the first, second, third, fourth and fifth unit of Good X, 1, 2,3,4 and 5 units of Good Y have been sacrificed respectively. The shape of PPC depends on MOC : 1. If MOC is increasing PPC is concave. 2. If MOC is decreasing, PPC is convex. 3.If MOC is constant, PPC is a straight line.

- 11. The Fig Illustrates the concept of marginal opportunity cost. It is assumed that initially resources are employed such that, output in Use-1 = OK and output in Use- 2=OL M.O.C = Loss of Output of Good Y/Gain of Output of Good X = KK1 / LL1 = ab / bc= Slope of production possibility curve

- 12. Micro and Macro Economics: Micro economics studies the behaviour of individual economic units of an economy like a consumer, a producer for different goods and services. Macroeconomics studies aggregates at the level of the economy as a whole like aggregate demand, aggregate supply, problem of full employment, total saving, total investment, aggregate price level, etc. DIFFERENCE MICROECONOMICS MACROECO0NOMICS 1. It studies individual economic units. 1. It studies aggregate economic units. 2. It deals with determination of price and 2. It deals with determination of general output in individual markets. price level and national output in the country. 3. It aims at optimal allocation of 3. It aims at determination of aggregate resources. output, national income, price level and employment level in the economy. 4. Example-Theory of demand, theory of 4. Example- Aggregate demand, supply, theory of price determination,etc. aggregate supply, national income,etc. QUESTIONS FOR BRIGHT LEARNERS VERY SHORT ANSWER TYPE QUESTIONS: - (1 Mark Each) Q.1. Why is there a need for economizing of resources? Ans. Because resources are limited. Q.2. Why does economic problem arise? Ans. It arises mainly because of scarcity of resources. Q.3. Why is PPC downward sloping from left to right? Ans. Because in situation of full employment of resources, production of one good can be increased only with less of other good. Q.4. What does a rightward shift of PPC indicate? Ans. The rightward shift of PPC indicates growth of resources or technological progress. Q.5. Why does the problem of choice arise? Ans. Relative scarcity of resources having alternative uses in relation to unlimited wants, gives rise to an economic problem. Q.6. Why does PPC look concave to the origin?

- 13. Ans. PPC is concave to the origin because of increasing marginal rate of transformation (or increasing marginal opportunity cost). Q.7. Which factor lead to a shift of PPC towards right hand side? Ans. Growth of resources or technological progress leads to a shift of PPC towards right-hand side. Q.8. What does a point below PPC indicate? Ans. It shows inefficient/underutilization of resources. Q.9. What is the slope of PPC? What does it show? Ans. Slope of PPC refers to MRT (marginal rate of transformation).It shows that in order to produce more units of one good, say X, some units of the other good, say Y must be sacrificed. So slope of PPC= ∆Y/∆X Q.10. When allocation of resources is considered as inefficient? Ans. Allocation of resources is considered as inefficient when economy performs below the PPC curve. Q.11.When can PPC be a straight line? Ans. When MOC is constant. Q.12 What is the opportunity cost of opting for higher studies rather than a job? Ans.It is the amount of wage/salary the person would have earned in a job. SHORT ANSWER TYPE QUESTIONS: (3/4 Marks Each) Q.1. (a) (b) (c) Draw PPC and show the following:- Full employment of resources, Underutilisation of resources, and Growth of resources.

- 14. Y (a) Full employment of P’ (c) Growth of Resources Commod ity Y . (b) Underutilisation of Resources X O Commodity X P P’ Ans. (a) Full employment of resources - A point anywhere on the PPC, shows the efficient use or full employment of resources. (b) Underutilisation of resources - A point anywhere inside of the curve, shows inefficient/under utilisation of resources. (c) Growth of resources – It refers to the shift in PPC. If more resources are generated, the level of production will increase. In the figure it is represented by a shift in PPC from PP to P’P’. Q.2. Why does PPC look concave to the origin? Explain. Ans. PPC looks concave to the origin because of increasing marginal rate of transformation/ substitution (or increasing marginal opportunity cost). It means that more and more units of commodity ‘y’ are to be sacrificed, to get each additional unit of commodity ‘x’. Q.3. What does a PPC show? When will it shift to the right? Ans. Production Possibility Curve shows the different combinations of two goods which an economy can produce with available technology and resources. It would shift towards right-hand side in case of growth of resources or technological progress.

- 15. Q.4. Does production take place only on the PP curve? Ans. Yes and no, both. Yes, if the given resources are fully and efficiently utilized. No, if the resources are underutilized or inefficiently utilized or both. Y A B PPC Cloth C .U D X O Wheat Refer to the above figure; on a point anywhere on the PPC the resources are fully and efficiently employed. On point U, below the PPC or any other point but below the PPC, the resources are either underutilized or inefficiently utilised or both. Any point below the PP curve thus highlights the problem of unemployment and inefficiency in the economy. Q.5. Why does an economic problem arise? Explain. Ans. Reasons- 1. Unlimited wants - Human wants go on multiplying with the expansion of education, knowledge, scientific advancement and economic growth. A man can not satisfy all of his wants and therefore he has to make a choice in order of urgency. 2. Limited resources - The resources are limited in relation to need for them. It is the main cause of economic problem. 3. Alternative use of resources - A resource can be utilized in a different way and for different purposes. Therefore choice has to be made among different uses of resources. Q.6. Calculate MRTXY at different production possibilities from the following hypothetical data. Draw a PPC on the basis of the schedule

- 16. Production Possibilities A B C D E F Commodity X 0 1 2 3 4 5 Commodity Y 15 14 12 9 5 0 Ans. Production Possibility Schedule: Production Possibilities Commodity X Commodity Y Marginal Rate of Transformation (MRT) =ΔY/ΔX A 0 15 B 1 14 C 2 12 D 3 9 E 4 5 F 5 0 --------- 1 Y : 1X 2 Y : 1X 3 Y : 1X 4 Y : 1X 5 Y : 1X

- 17. Y 15 PPC 14 Comm1 o2 d ity Y X 0 1 2 3 4 5 Commodity X Value based question:- Q1 A basic economic problem is that there is oil shortage in INDIA. What measures do you suggest to mee t the growing demand of oil? Ans:-Measures taken are : 1) oil is limited so it should be efficiently and fully(optimum use)used. 2)Massive awareness on shortage of oil and people should be encouraged to use public transport system. Q2. The state govt. has sanctioned acertain amount to increase production in rural areas. Which technique of production will you suggest to the state govt. for this project? Ans.:-Labour intensive technique of production. Q3. Why is it that on one hand coal is found in plenty, yet it is scarce , while a rotten fruit is rare but not scarce? Ans:- Coal is scarce because its demand is greater than its supply.A rotten fruit is not scarce because there is no demand for rotten fruits. Q4. For a devolepmental project, logs of wood another building material have to be carried to the upper floor of building under renovation by the labour .Alternatively elevators and lifts can do the job ,which one will you choose and buy? Ans:- I will choose the second alternative as it is efficient and time and money saving method.

- 18. Q5. If more and more resources are constantly explored and new and new technique of production are constantly discovered,don’t you think a day will come when our central problems will be solved once for all? Ans:-When new resources are explored and new technology is discovered,PPC wouldexpand,indicating larger and larger flow of goods &services in the economy.But our wants are limlted, so scarcity of resources in relation to human wants will always exist.And,so long as limited resources are to colliding with unlimited wants,central problems can never be solved once for all. QUESTION FOR LATE BLOOMERS FOR THE SESSION 2013 Q1.What is microeconomics? Ans:Microecomics is the study of an individual economic unit like a firm, a consumer. Q2.What is PPC? Ans:Production possibility curve shows different combinations of two goods which can be produced with given resources and technology. Q3.What is Opportunity Cost? Ans:It is the value of a factor in its next best alternative use. Q4.What is marginal opportunity cost? Ans:It is the rate at which output of good Y is to be sacrificed for every additional unit of good X. Q5.Write two properties of PPC. Ans:PPC slopes downward from left to right. And PPC is concave to the origin. Q6.Why does an economic problem arise? Ans:An economic problem arises because resources are limited,our wants are unlimited and resources have alternative uses. Q7.What are the 3 basic economic problems of an economy? Ans.The 3 basic economic problems are: 1.What to produce and in what quantity? 2.How to produce? 3.For whom to produce?

- 19. Q8.Explain the meaning of what to produce? Ans: For answer see gist of the chapter. Q9.Explain the meaning of how to produce? Ans.For answer see gist of the chapter. Q10.Explain the meaning of For whom to produce? Ans:see gist of the chapter for this answer. Q11.Draw PPC and show the following: 1.Overutilisation of resources. 2.Fullutilisation of resources. 3.Underutilisation of resources. Q12.Write differences between microeconomics and macroeconomics. Ans.See gist of the lesson. TEST PAPER:-CLASS XII CHAPTER :- 1 ( INTRODUCTION) Q.1 What is an economy?( 1) Q.2 What is scarcity .{1} Q.3 Name the central problems of an economy.{1} Q.4 Why do economic problems arise?.{1} Q.5 What is the problem of what to produce? {1} OR Q.6 What is the problem of How to produce? {1} Q.7 What is the problem of ‘for whom to produce’? {1} Q.8 Define a PPC? {1} Q.9 Define opportunity cost.{1} OR Q.10 What is marginal opportunity cost or marginal rate of transformation? {1} Q.11 Define:) Micro economics.{1}

- 20. OR Q.12 Define M acro economics.{1} Q.13 What does a point on PPC indicate?{1} Q.14 FILL IN THE BLANKS. 1. The PPC would shift to right when there is _------------- of resources. 2) The basic economic problem is the problem of _-----------------------. 3)Cotton textile industry is the subject matter of _----------economics. 3x1 Q.15 What is Rotation of PPC? Explain with diagram. {3} OR Q 16 What is shift in PPC? Explain with diagram {3} Q.17 Why is PPC concave? Explain.{3} Q18. Does production take place only on thePPC? Explain with diagram. {3} Q.19A lot people died and many factories were destroyed in an earthquake{ natural calamity}. How will it affect the PPC? {3} Q20 Draw a ppc to represent the following on it . a)Underemployment of resources. b)Growth of resources c)Fuller utilization of resources. {4} Q21. Draw the shape of PPC when MOC is (a)Decreasing (b)Constant (c) Increasing. {4} Q22. Plot the PPC by taking Rice consumption on the X axis. Comment on the shape of the curve. {4} RICE CONSUMPTION FUEL CONSUMPTION 100 0 90 1 70 2 40 3 0 4

- 21. UNIT – 2 (16 Marks) CONSUMER BEHAVIOUR AND THE THEORY OF DEMAND STUDY MATERIAL FOR BRIGHT STUDENTS Sr. No 1 Chapters Utility Analysis Concepts Cardinal and Ordinal Utility Consumer’s Equilibrium - One Commodity - Two Commodity - Indifference Curve and Budget line Demand-Individual and Market Demand 2 Demand and Law of Demand 3 Elasticity of Demand Law of Demand Change in Demand and Change in quantity demanded Concept of elasticity of demand Factors affecting elasticity of demand Methods of measuring price elasticity of demand -Point Method -Total Expenditure Method - Geometric Method Utility Analysis Utility - Want satisfying Power of a good. Cardinal Utility – It says that utility can be measured in number. (Quantitative Concept) Ordinal Utility – It says that utility being a mental concept can’t be measured in number. (Qualitative Concept) Total Utility – It is the sum total of Utility derived from the consumption all units of consumption.TU= Sum of MU Marginal Utility – It refers to the additional utility on account of consumption of an additional unit of commodity. MU=TUn-TUn-1 Consumption of x TU MU 1 20 20 2 36 16 3 46 10 4 50 4 5 50 0 6 44 -6 7 42 -2 8 38 -4 Law of Marginal Utility – The law says that when a consumer consumes more and more amount of one commodity, the utility derived from successive units of commodity will go on declining.

- 22. Consumer Equilibrium- Consumer’s equilibrium is a situation where the consumer maximises his satisfaction out of his limited income. Indifference Curve - It refers to the locus of all possible combinations of two commodity which gives equal level of satisfaction to the consumer. Budget line – It is the locus of all possible combinations of two commodities which can be purchased at a given level of income. Question and Answer 1. What do you mean by monotonic preference? Ans . it mean that a rational consumer always prefer more of a commodity as it offers him a higher level of satisfaction. 2. What price the consumer is ready to pay for a commodity in a state of his equilibrium? Ans:- in a state of equilibrium the price that the consumer is ready to pay is exactly equal to the price prevailing in the market . Because, in a state of equilibrium , money worth of marginal utility that the consumer gets is exactly equal to market price he has to pay. 3. What happen when Mux/Px is greater than MUy/Py ? Ans. This situation implies that by spending a rupee on Good –X the consumer gets grater marginal utility that in case of Good-Y. Accordingly, he will spend more on X than Y .As consumption of X rises, Mux will fall .On other hand ,as consumption of Y falls ,MUy will rise. The consumer will stop buying more of X in place of Y only when Mux/Px=MUy/Py. It is here only that the equilibrium is struck. 4. How is equilibrium of the consumer affected when Mum happens to rise ,and Px is constant. Ans . Equilibrium is struck when Mux/Px=Mum. If MUm rises and price is constant ,the consumer will be off the point of equilibrium .Because Mux/Px would then be less than Mum . the consumer will reach back his equilibrium only if Mux rises ,as Px is given to be constant . This will happen only when consumption of commodity –X is decreased. 5. How will the consumer move along his IC in a situation when MRSxy> Px/Py Ans. The consumer should move downward to the right along the IC . Convexity of the IC ensure that as the consumer moves downward to the right along his IC, MRSxy tends to fall. Implying that the consumer should start consuming more of X in place of Y. 6. How will a consumer adjust his consumption of Good-X and Y in asitution when MRSxy=Px/Py Ans. The consumer should start consuming more of Y in place of X . That is, he should move upward to the left along the IC . Convexity of the Ic ensure that as the consumer moves upward to the left along his IC , MRSxy tends to rise . He should stop at a point when MRSxy=Px/Py

- 23. 7. Why should a consumer buy more of a commodity even when MU of every successive units tends to decrease Ans. Even when MU is decreasing ,its money worthy still be greater than the price he has to pay. We know ,the consumer stops buying a good only when its money worth of MU is equal to its price. 8. State the condition of consumer’s equilibrium. Ans. Hint: A consumer strikes his equilibrium when rupee worth of marginal utility actually received by the consumer is equal to marginal utility on money Mux/Px=Mum Demand and Law of Demand Demand – Demand for a commodity is defined as the amount of commodity which a consumer purchase at a given price and at a given time. Individual Demand – It shows the amount of commodity purchased by an individual consumer at a given price and at given time. Market Demand – It shows the amount of commodity purchased by all consumers present in the market at a given price and at a given time. Demand function – It is the functional relationship between the quantity demanded and the factors affecting it. Symbolically it is written as Q = f( P R I N T), where P-Price of the commodity, R- Price of the related commodity, I – Income of the consumer N – Number of consumer, T – Taste and Habits and Preference of the consumer Law of Demand- Law of demand says that other thing remaining same more is demanded at a less price and less is demanded at a high price. Hence there exist an inverse relationship between the price and quantity demanded. Change in demand – When quantity demanded of a commodity changes due to change in the other factors, price of the commodity remaining constant, it is called change in demand. It is also called movement of the demand curve. It is of two types such as a) Increase in Demand b) Decrease in demand and Increase in Demand – When quantity demanded of a commodity increases due to positive changes in the other factors, price remaining constant, it is called increase in demand. Decrease in Demand – When quantity demanded of a commodity decreases due to negative changes in the other factors, price remaining constant, it is called decrease in demand. Change in quantity demanded – When quantity demanded of a commodity changes due to change in its price, other factors remaining constant, it is called change in quantity demanded. It is also called movement along the demand curve. It is of two types such as:- a) Expansion in demand b) Contraction in demand. Expansion in demand – when quantity demanded of a commodity increases due to fall in the price of the commodity, it is called expansion in demand.

- 24. Contraction in demand – When quantity demanded of a commodity decreases due to rise in the price of the commodity, it is called contraction in demand. Elasticity of demand Price elasticity of demand- It is defined as the degree of responsiveness in the quantity demanded of a commodity due to change in its price, other factors remaining constant. Factors affecting price elasticity of demand: 1. Nature of commodity 2. Availability of Substitutes 3. Diversity of uses 4. Income level of the buyer 5. Habit of the consumer 6. Proportion of income spent on a commodity 7. Time Period 8. Postponement of use Methods of measuring price elasticity of demand - There are three methods of measuring price elasticity of demand. These are 1. Percentage Method 2. Total expenditure method 3. Geometric Method Percentage Method: By percentage method the price elasticity of demand is measured by taking the ratio between the percentage change in quantity demand and the percentage change in price. Ed= (-) % Change in quantity Demanded/ % Change in price. Ed = q1-q/q*100 P1-p/p*100 = Δq/q Δp/p = Δq/q *p/Δp Ed = p/q * Δq/ Δp Question and Answer 1. If the quantity demanded of a commodity ‘X’ decreases as the household income increases, what type of good is ‘X’? Ans. Inferior good. 2. Write down one factor responsible for increase in demand. Ans. Rise of income or favourable taste for a good. 3. At the given price when will be the demand of a commodity be less? Ans. Fall in the income. or Ans. Fall in the price of a substitute good.

- 25. 4. When two demand curves intersect with each other which will be more elastic. Ans. The demand curve which is more flattered will be more elastic. 5. If the demands for good ‘Y’ increases as price of another good ‘X’ rises how the two goods are related? Ans. These are substitute goods. 6. Answer in one sentence the assumption on which a demand curve is constructed Ans. That all the determinates are constant. 7. What is cross price effect? Ans. Cross price effect refers to the effect of change in the price of commodity-X on the demand for commodity Y when X and Y are related goods. 8. What types of goods find a rise in their demand even income of the buyer reduces? Ans. Inferior goods 9. Why is demand for water inelastic ? Ans. Demand for water is inelastic ,as water is an essential of life. 3/4 Mark Questions : 1.Give difference between change in demand and change in quantity demanded. Change in quantity demanded 1. More or less quantity is demanded due to change of price 2. Movement on same demand curve downwards or upwards 3. Extension & contraction are two stages. Change in demand 1. More or less quantity is demanded due to factors other then price. 2. Shifting of demand curve towards left and right 3. Increase and decrease are two stages 2. Why more is purchased when price falls? Or Why does demand curve slope downwards? Ans. (a)Income effect: - change in real income due to change in price is income effect. When price falls real income increases that why a person purchases more. (b)Size of consumer groups: - when price falls the demand extends because the persons who were not purchasing earlier. They also start purchasing. (c)Substitution effect: - when the price of a substitute good increases the demand of the given god increases as it is relatively cheaper.

- 26. (d)Law of diminishing marginal utility:- by using more and more units of a commodity the marginal utility from each successive unit goes on decreasing. This is why the consumer buys more commodities at low price. 3.Explain with the help of diagram, the effect of the following changes on the demand of a commodity. 10. Fall in the price of a substitute good . 11. Fall in the income of its buyers. Ans. (a) Fall in the price of a substitute good will cause fall in the demand of the given commodity from 0q to 0q1. the demand curve will shift towards left to d1d1 (b) Fall in the income of its buyer will cause fall in the demand of normal goods from 0q to 0q1. the demand curve will shift towards left from dd to d1d1 4.Price of a commodity falls from Rs. 4 to Rs. 3 per unit. As a result total expenditure on it rises from Rs. 200 to Rs. 300. Find out price elasticity of demand by percentage method. Ans. PriceTotal Exp.Quantity Rs. 4Rs. 200200/4=50 Rs. 3Rs. 300300/3=100 Ed:- P / q x ∆q / ∆p Ed:- (-) 4 / 50 x 100 – 50 / 3-4 Ed:- (-) 4 / 50 x 50 / -1Ed:- 4

- 27. 5. Given the fact that the slope of a straight line demand curve =∆P/∆Q, how do you relate it to own price elasticity of demand ? Ans. We know ,Ed = P/Q x ∆Q/∆P . Given the fact that slope of demand curve = =∆P/∆Q , We can write that Ed = 1/slope of demand curve X P/Q Diagrams + 1. Law of demand with demand curve 2. Market Demand Curve A B Market 3. Change in quantity demanded and change in demand

- 28. Due to change in price No shifting of demand curve Price constant Shifting of demand curve 4 Degrees of price elasticity of demand Ed >1 Ed <1 Ed =0 Ed=infinity STUDY MATERIAL FOR SLOW LEARNERS (UNIT II) CONSUMER’S BEHAVIOUR AND DEMAND SOME BASIC CONCEPTS OF THE RELATED UNIT Utility:-Wants satisfying quality of a commodity. Total utility:-Total psychological satisfaction obtained from the consumption of all the commodities. Marginal utility:-The rate of change in total utility is known as marginal utility. Normal good:-whose demand increases with increase in income & vice-versa. Inferior good:- Whose demand decreases with increase in income & vice-versa.

- 29. Giffen good:-whose demand increases with increase in price & vice-versa. Substitute good:-Goods which can be demanded in place of other good. Complementary good:- Goods which are jointly demanded. Demand:-It is an effective desire which can be demanded at a certain price, place & time. Law of demand:- other things remaining the same, higher the price lower the demand & vice-versa. Indifference curve:-Locus of various points where a consumer attains equal level of satisfaction at all points. Indifference map:- Set of indifference curve which shows different level of satisfaction. Budget set:-The bundle of goods a consumer can buy from his/her entire income. Budget line :-It shows the budgetary constraints or the money income of the consumer. Consumer’s equilibrium:- when a consumer attains maximum level of satisfaction from the given income. Law of diminishing marginal utility:- It declines with the consumption of successive units of the commodity. Change in demand:- Affected by the factor other than price. Change in quantity demand:- Affected by price only. Elasticity of demand:-Responsive change in quantity demand which is due to responsive change in price. Factors affecting demand:- price of the goods,income of consumer, change in future price, taste0 and preference of consumer etc. (Very Short answer Questions Carrying 1 marks each) Q1.Define marginal utility? Ans:- The rate of change in total utility during consumption process is known as marginal utility. Q2. What is demand? Ans:- It is an effective desire which can be demanded at a certain price, place and time.

- 30. Q3. What is law of demand? Ans:- other things remaining the same higher the price lower the demand and vice- versa. Q4. What is normal good? Ans:-Goods whose demand increases with the increase in income and vice-versa. Q5. What is inferior good? Ans:- Goods whose demand decreases with the decrease in income is known as inferior good. Q6. Give two examples of giffen good. Ans:- Diamond, Precious stone, Merchandise car etc. Q7. Define the term elasticity of demand. Ans:- Percentage change in quantity demand which is due to percentage change in price is known as elasticity of demand. Q8. Write the situation when a consumer’s attain equilibrium in case of one good. Ans:- Mux/Px=Mum Q9. What do you mean by increase in demand? Ans:-It is a situation when demand increases irrespective of without change in price. Q10. What is inelastic demand? Ans:- When demand does not change irrespective of change in price. (Short Answer Questions carrying 3 Marks each ) Q1. List three factors which affects demand. Ans:- a)Price of the commodity b) Income of the consumer c) Change in taste, behaviour and preference of the consumer Q2. Distinguish between Normal good and Inferior good. Ans:-

- 31. Normal good Inferior good # Goods whose demand increase with # Goods whose demand decreases with increase in income .increase in income. # It has positive slope .# It has negatively slope. Q3. Differentiate between increase in demand and extension in demand. Ans:- Increase in demand Extension in demand # Demand increases without change in # Demand extends due to change in Price price # Rightward shifting of demand curve .# Movement along demand curve. Q4. Write the properties of indifference curve.(any three) Ans:-1)Higher indifference curve gives higher level of satisfaction. 2) Two indifference curve never intersect each other at any point. 3) Indifference curves are convex to origin. Q5.Mention any three factors which effects elasticity of demand. Ans:- a)Nature of the commodity-necessary and luxurious good b)Time period-short and long c) Proportion of expenditure-larger and smaller part(students will explain the points in brief) Q6.Calculate price elasticity of demand by total expenditure method:- Price(Rs) 8 10 Ans:- Quantity demand(units) 100 90 Price 8 10 Quantity demand 100 90 Total expenditure 800 900 Type of elasticity Ed=<1

- 32. Q7.Explain the concept of law of demand with suitable schedule. Ans:-Law of demand states that other things remaining the same higher the price lower the demand and vice-versa. Price (Rs) 10 5 (pupil will explain the schedule in brief) Quantity Demand 20 40 Q8. Show the relationship between total and marginal utility with the help of curve. Ans:- y TU utility o units of commodity MU x i)When TU increases MU falls. ii) When TU is maximum MU becomes Zero. iii) When TU declines MU becomes negative. (Short Answers Questions having 4 marks ) Q1. Distinguish between substitute and complementary good. Give example in each case. Ans:- Substitute good:- Goods which are demanded in place of one another is known as substitute goods. For example-tea and coffee, wheat and rice, bike and scooter etc. Complementary good:- Goods which are jointly demanded is known as complementary good. For example-car and petrol, bread and butter, pen and ink etc. Q2. Explain the effect of change in income of the buyers of a good on its demand. Ans:- As we know that the income of the consumer either increase or decrease and a rational Consumer behaves accordingly. Incase if consumer income raises then ultimately the demand will also increase and if consumer’s income decline then consequently he will demand less due to fall in income.(student may take an example to explain the concept by taking the case of normal and inferior good).

- 33. Q3. Distinguish between individual demand and market demand. Ans:- Individual demand:-Demand of a particular commodity by an individual consumer in the market is known as individual demand. For ex- Ram’s demand for milk. Market demand:- Demand of a commodity by all the consumers in the market is termed as market demand. For ex- Ram,Sohan and mohan’s demand for milk will be combined known as market demand. (Long Answer type questions carrying 6 Marks only) Q1. Explain briefly any three factors which lead to increase in demand. Ans:- (1)Increase in income of the consumer (2) Expected increase in future price (3) Increase in size of population (Pupil will explain the mentioned points along with suitable schedule and diagram) Q2. Define consumer’s equilibrium. Write its condition in case of two commodities with the help of suitable diagram. Ans:-It is a situation when a consumer spends his entire income on two goods in such a manner which gives him maximum satisfaction. Condition of consumer’s equilibrium:- i)Slope of IC =Slope of budget line i.e MRSxy=Px/Py ii) At equilibrium point IC is tangent to budget line. iii) IC is convex to the point of origin & we obtain decreasing MRS. Y IC o good x(Need diagram and its suitable explanation)

- 34. Test Paper for Bright Students Unit -2 (Consumer’s Behaviour) 1. What does ‘the law of diminishing marginal utility’ say? 1 2. Mention the conditions of consumer’s equilibrium in single commodity case.1 3. Given the market price of a good, how does a consumer decide as to how many units of that good to buy? Explain.3 4. Why does the demand curve downward slope? OR Give the reasons due to which the law of demand holds.4 5. State the ‘law of demand’. What is meant by the assumption “other things” remaining the same, on which the law is based.4 6. Price elasticity of demand for a good is (-) 1. At a given price the consumer buys 60 units of the good. How many units will the consumer buy if the price falls by 10%?4 7. Suppose there are 30 consumers for a good, having identical demand function: d(p) =10-3P for any price less than or equal to 10/3 and d(p)=0 for any price greater than 10/3. Write the market demand function. 6 8. Determine how the following changes (or shifts) will affect market demand curve of a product. 2×3=6 a) A new steel plant comes up in Jharkhand people who were previously unemployed in the area are now employed. How will this affect the demand for colour T.V. and Black and White T.V. in the region? b) In order to encourage tourism in Goa. The Government of India suggests Indian Airlines to reduce air fare to Goa from the four major cities of Chennai, Kolkata, Mumbai and New Delhi. If the Indian Airlines reduces the fare to Goa, How will this affect the market demand curve for air travel to Goa? c) There are train and bus services between New Delhi and Jaipur. Suppose that the train fare between the two cities comes down. How will this affect demand curve for bus travel between the two cities? Test Paper for Bright Students Unit -2 (Consumer’s Behaviour) 1. What is MRSxy.1 2. What happens to the demand curve of an inferior good when the income of the buyer rises? 1 3. What happens to demand of a commodity if there is an increase in price of the complementary good?1

- 35. 4. Define consumer equilibrium. Why does a consumer maximize her satisfaction only when the slope of both Indifference curve and Budget line are equal to each other?3 OR How much quantity of a good will be purchased by a consumer at a given market price to maximize her satisfaction? Explain with the help of a utility schedule. 5. Explain the difference between:- 4 A: Utility analysis and Indifference curve analysis. B: Normal goods and Giffen’s goods 6 : Given Ed = - 0.02, and percentage increase in price = 20%, find change in expenditure onthe commodity. 4 7 :Price of a commodity falls from Rs. 4 to Rs. 3 per unit. As a result total expenditure on it rises from Rs. 200 to Rs. 300. find out price elasticity of demand by percentage method. 4 8 Identify the effect on demand of the following–6 (a)Govt enhanced the pay of the government employees. How will this affect the demand curve of government employees? (b)A new car factory comes up in Assam; many people who previously unemployed, in the area are now employed .How will this affect demand curve of television. (c) There are train and bus service between Lucknow and Agra. Suppose the train fare between two cities comes down, how will this affect the demand curve for bus travel between two cities? 9 : “If a product price increases, a family’s spending on the product has to increase.” Defend or refute.6 TEST PAPER-2 (CONSUMER BEHAVIOUR AND DEMAND) (FOR UNDER ACHIEVERS) Q.1.State whether the following statements are true or false: 1x4=4 i. If other things remaining constant, there is positive relationship between quantity demanded and own price of a commodity. ii. The demand for inferior goods increases with decrease in income of consumer. iii.When elasticity of demand is equal to zero ,the demand curve will be vertical straight line parallel to Y-axis. iv. Income of consumer affect the demand for an individual. Q.2.Fill in the blanks: 1x4=4

- 36. a.Indifference curve is ----------------------- to the origin. b.In case of --------------------goods demand rises with increase in income. c.When a change in price causes no change in total expenditure then elasticity of demand is--------------. d.If good X and good Y are used together to fulfill a want then good X and good Y are ------------------------goods. Q.3.Categorise the following changes as expansion, contraction, increase or decrease in demand (assuming given commodity is a normal good) 1x6=6 i. When price of substitute rises. ii. When price of given commodity increases. iii. When income of consumer decreases. iv. When price of given commodity falls. v. When the given commodity becomes a fashion good. vi. When price of complimentary good increases. Q.4.Draw demand curves having following elasticity: 1x4=4 i.Ed=0 ii.Ed=1 iii.Ed<1 iv.Ed=∞ Work-Sheet Q1 What is the another name of indifference curve approach? (a) Ordinal approach Q2 What is the formula of TU ? (b) Cardinal Approach (c) Both a and b (a) ∑ MP (b) ∑ MC (c) ∑ MU Q3 What is the normal shape of IC ? (a) Concave (b) Straight Line (c) Convex Q4 What is meant by change in demand ? (a) Increase or decrease in demand demand (c ) Both a and b Q5 What is meant by change in quantity demanded? (b) Extension or contraction in (a) Increase or decrease in demand(b) Extension or contraction in demand (c) Both a and b

- 37. Q6 The % change in quantity demanded will be equal to % change in price if – (a) Ed = 2 (b) Ed = 3 (c) Ed = 1 Q7 What is the slope of demand curve in case of normal goods? (a) Negative (b) Positive (c) Parallel to X axis Q8 What is the shape of demand curve in case of giffen goods? (a) Negative (b) Positive (c) Parallel to Y axis Q9 What is the another name of total expenditure method of measuring price elasticity of demand? (a) Total outlay method Method (b) Total cost method (c) MC and MR Q10 What is the formula to measure the price elasticity of demand through point method? (a) Upper portion / lower portion ( c) None of the two. Ans. 1.a 2.c 3.c 4.a 5.b (b) Lower portion / Upper portion 6.c 7.a 8.b 9.a 10.b UNIT – III PRODUCER BEHAVIOUR AND SUPPLY (16 Marks) A. PRODUCTION FUNCTION: TOTAL PRODUCT, AVERAGE PRODUCT, MARGINAL PRODUCT, RETURNS TO A FACTOR & PRODUCER’S EQUILIBRIUM BASIC CONCEPTS: 1. Production function: refers to the technological relation between physical inputs and physical output. It is the technological knowledge that determines the maximum level of output that can be produced by employing different levels of inputs. It is expressed in terms of a function as follows: q = f (x1, x2), where x1 is the amount of factor1, x2 is the amount of factor2, and ‘q’ is quantity of output to be produced. 2. Total Product: refers to total quantity of goods produced by a firm during a given period of time by varying the units of a variable input like factor 1. 3. Average product is defined the output per unit of a variable input, say, factor1. That is, AP1 = TP/x1.

- 38. 4. Marginal product refers to addition to total product, when one more unit of variable factor is employed, that is, MP1 = = TPn –TPn-1 5. Short Run and Long Run: Short run is a period in which some factors are variable (variable input) and other factors remain fixed (fixed input). On the other hand, in the long run, all factors of production are variable, nil is the fixed factor. 6. Returns to a factor refers to change in total product due change in only the variable input in the short run, while fixed inputs remain constant. 7. Law of Variable Proportion: states that if we go on increasing more and more units of a variable factor with fixed factor remain constant, total product increases at an increasing rate, but beyond a certain level of employment total product increases at a decreasing rate and finally TP falls. 8. Law of Diminishing Marginal Product states that if we keep on increasing the employment of a variable input with other inputs fixed, finally a point will be reached after which the marginal product will start falling. 9. Relation between: (i) TP and MP, and (ii) MP and AP in terms of a schedule: Factor1 TP1 MP1 AP1 O 0 - - 1 10 10 10 2 24 14 12 3 40 16 13.3 4 50 10 12.5 5 56 6 11.2 6 57 1 9.5 7 57 0 8.1 8 56 -1 7 (i) From the above schedule, the relation between TP and MP is derived as follows: Stages I:IncreasingReturnto factor1(uptofactor employment level 3 units ) II: Diminishing Return to factor 1 (from 4units to 0 unit) III: Negative Return to factor1 (after 7 units) TP1 Increases at increasing rate Increasesat diminishing rate Starts falling MP1 an Increasing a Diminishing Negative

- 39. * When TP is maximum, MP is zero. (ii) From the above schedule, the relation between MP and AP is derived as follows: (a) When AP rises, MP is higher than AP, (b)When AP falls, MP is less than AP, and (c) When AP is maximum, MP =AP, (d) MP may be positive, zero or negative but AP is always positive. 10. Reasons for the operation of increasing returns to a factor: (i) better utilization of the fixed input with increase in variable input, (ii) benefits of division and specialization of the variable input used, say, labour, (iii) indivisibility of fixed input. 11. Reasons for the operation of diminishing return to a variable input, say, labour: (i) optimum combination between fixed and variable inputs is disturbed with increasing use of the variable input, (ii) After a certain level of employment of the variable input, the benefits from the division of labour will diminish leading to diminishing return. (iii) imperfect substitutes between fixed input and variable input. QUESTIONS: A. Very short answer questions: 1. Define production function. 2. Define average product. 3. Define marginal product. 4. Define law of variable proportions. 5. What is the law diminishing marginal product? 6. How is TP derived from MP? 7. Define Producer’s equilibrium. 8. What are the conditions of producer’s equilibrium? 9. Give the meaning returns to a factor?

- 40. 10. What is the general shape of MP curve? 11. What happens to MP when TP increases at an increasing rate? B. Short Answer Questions: 1. Explain the relation between TP and MP in terms of TP and MP curves. 2. Explain the relation between MP and AP in terms of MP and AP curve. 3. What are the conditions of producer’s equilibrium under MC-MR approach? 4. What are the reasons of the operation of increasing returns to a variable input? C. Long Answer questions: 1. Explain the law of variable proportions in terms of (i) TP and MP curves, and (ii) a schedule of TP and MP. 2. What is producer’s equilibrium? Explain the producer’s equilibrium under MC-MR approach. Use diagram. 3. To increase the production of a good only one input is increasing while other inputs are held constant. Explain its effect on total physical product. Give reasons. D. NUMERICAL QUESTIONS WITH SOLUTIONS: Q.1. Find out APP and MPP. (i) Labour 1 2 3 4 5 6 7 TPP 40 80 110 130 140 140 130 Ans. APP 40 40 36.67 32.5 28 23.33 18.57 MPP 40 40 30 20 10 0 -10 (ii) Find out the TPP and APP. Labour 1 2 3 4 5 6 7 MPP 24 20 16 12 8 0 -8 Ans. TPP 24 44 60 72 80 80 72 APP 24 22 20 18 16 13.33 10.28

- 41. (iii) Calculate the APP and MPP. Labour 0 1 2 3 4 5 6 7 TPP 0 5 12 20 30 35 40 42 Ans. APP 0 5 6 6.66 7.5 7 6.66 6 MPP - 5 7 8 10 5 5 2 (iv) The following table gives APP of a factor. It is also known that (TPP) total product at O level of employment is O. Determine its total product and marginal product. Labour 1 2 3 4 5 6 APP 50 48 45 42 39 35 Ans. TPP 0 50 96 135 168 195 210 MPP - 50 46 39 33 27 15 7. Complete the following table: Units of Labour TP AP MP 1 --- 3 -- 5 20 -- 66 --- -- -- -- 21 22 -- --- 22 22 21 --- 9. Find out the maximum profit position of a producer by comparing MC & MR on the basis of the following data:

- 42. Output (in units) 1 2 3 4 5 MR (Rs) 10 9 8 7 6 MC (Rs) 4 5 6 7 8 E. HOT Questions: 1. What happens to TP when MP is zero? 2. What happens to MPP when TPP increases at decreasing rate? 3. As the variable input is increased by one unit, total output falls. What would you say about of marginal productivity labour? 4.What happens to MPP when TPP falls? 5.Why MP curve lies above AP curve in the phase of increasing returns to a factor? 6.Why AP keeps raising even when MP declines? 7.When will the producer will be in equilibrium. Explain with the help of a schedule. 8. Explain the conditions of producer’s equilibrium in case of MR & MC approach (with the help of diagram). 9.When does a producer earn maximum profit? 10.Prove that for profit maximization:- 1)The market price (P) = MC. 2)MC curve is non-decreasing F: True or False Questions: 1. State whether the following statements are true or false. Give reasons for your answer. (i) When there are diminishing returns to a factor TP first increases then start falling. (ii) Average product will increase only when marginal product increases. (iii) Under diminishing returns to a factor, total product continues to increase till marginal product reaches zero. G. MCQ Questions: 1. Some factors variable and some factors fixed are referred to the period as: (a) medium run, (b) long run, (c) short run, (d) None of the above. 2. Output per unit of a variable input is called: (a) MP (b) TP (c) AP (d) AC 3. The technological relation between inputs and output is referred to as: (i) cost function, (ii) supply function (iii) utility function (iv) production function.

- 43. 4. If we keep on increasing units a variable input, fixed inputs remain constant, the marginal product is initially increasing. But after a certain level of employment marginal product starts falling. What is the law? (i) law of diminishing marginal product, (ii) law of variable proportions, (iii) law of diminishing marginal utility, (iii) law of demand 5. What happens to MP when TP continues to increase at a diminishing rate? (a) increasing, (b) diminishing (c) remain constant (d) negative 6. What is the value of TP if the AP is 12 at 4 unit of variable input? (i) 6 (ii) 16 (iii) 48 (iv) 8 7. A producer is in equilibrium when: (i) MC>MR, (ii) MC= MR, (iii) MC is increasing, (iv) both (ii) and (iii) STUDY MATERIALS FOR UNDER-ACHIEVERS (QUESTIONS WITH SOLUTIONS): 1. Define marginal product. Ans: Marginal product is an addition to the total production by using an extra unit of a variable factor. 2. Define average product. Ans: Average product is the product per unit of a variable factor used. 3. Define production function. Ans: Production function is defined as technological relation between inputs and output. 4. What is the relation between TP and MP? Ans: (i) When TP rises at an increasing rate, MP is increasing. (ii) When TP rises at a diminishing rate MP is diminishing. (iii) When TP starts falling, MP is negative. (iv) When TP is maximum, MP is zero. 5. What is producer’s equilibrium? Ans: Producer’s equilibrium refers to a position at which the producer gets maximum profit with minimum cost. 6. State the conditions of producer’s equilibrium. Ans: (i) MC = MR and (ii) MC should be rising at the point of equilibrium. 7. From the following table, find out the level of output at which the producer will be in equilibrium. Give reasons for your answer.

- 44. Ans: Output (in units) 1 2 3 4 5 Output (in units) 1 2 3 4 5 Marginal Revenue (Rs.) 8 8 8 8 8 Marginal Revenue (Rs.) 8 8 8 8 8 Marginal Cost (Rs.) 10 8 7 8 9 Marginal Cost (Rs.) 10 8 7 8 9 From the above schedule it is concluded that the producer attains equilibrium when he produces 04 unit of the output because at this level of output both conditions of producer’s equilibrium are satisfied, i.e., (i) MC = MR, and (ii) MC is increasing at point of equilibrium. STUDY MATERIALS FOR BRIGHT LEARNERS (QUESTIONS WITH SOLUTIONS): 1. What type of changes take place in TP and MP when there are: (a) increasing return to a factor (b) diminishing return to a factor Why do these changes take place? Ans: (a) TP increases an increasing rate and MP is increasing. Causes: (i) better utilization of the fixed input with increase in variable input, (ii) benefits of division and specialization of the variable input used, say, labour, (iii) indivisibility of fixed input. (b) TP increases at a diminishing rate and MP is diminishing. Causes:(i) optimum combination between fixed and variable inputs is disturbed with increasing use of the variable input,

- 45. (ii) After a certain level of employment of the variable input, the benefits from the division of labour will diminish leading to diminishing return. (iii) imperfect substitutes between fixed input and variable input 2. Identify the different phases of the law of variable proportions from the following schedule. Give reasons for your answer. Ans: Variable input (units) 1 2 3 4 5 TP (Units) 4 9 13 15 12 Variable Input 1 2 3 4 5 TP MP 4 4 9 5 13 4 15 2 12 -3 Phases I: Increasing return to a factor II: Diminishing return to a factor Negative return to a factor Reasons: (i) In the 1st phase, TP increases at an increasing rate and MP is increasing. (ii) In the 2nd stage, TP increases at a diminishing rate and MP is diminishing. (iii) In the 3rd stage, TP starts falling, and MP is negative. B.COST & REVENUE: Meaning-Cost means the total expenditure incurred in the Production of a commodity. Broadly Costs are of two types:- Short-run costs & Long-run costs. Short run costs-Short-run is a period of time when some factors are fixed and some factors are Variable. Expenditure incurred in the Production of a commodity in the short-run is known as short-run cost. Long-run costs-Long-run is a time period when all the factors are variable. Expenditure incurred in the production of a commodity in the long-run is known as Long-run cost. Types of Short-run costs: 1. Total Fixed Cost (TFC)-Expenditure incurred on the fixed factors of production are known as Total fixed costs. Fixed costs do not vary with change in output.

- 46. TFC 40 TVC -- TC 40 AFC -- AVC -- AC -- MC -- 40 20 60 40.00 20.00 60.00 20 40 38 78 20.00 19.00 39.00 18 40 53 93 13.33 17.67 31.00 15 40 63 103 10.00 15.75 25.75 10 40 69 109 8.00 13.80 21.80 6 40 77 117 6.67 12.83 19.50 8 40 89 129 5.71 12.71 18.43 12 40 107 147 5.00 13.38 18.38 18 40 132 172 4.44 14.67 19.11 25 40 162 202 4.00 16.20 20.20 30 TFC=TC-TVC 2. Total Variable cost (TVC)- Expenditure incurred on the variable factors of production are known as Total Variable Cost. Variable costs vary with change in output. TVC=TC-TFC Total Cost (TC)-Total Cost is the total expenditure incurred on the production 3. of a commodity. It is the sum total of Total Fixed Cost and Total Variable Cost. TC=TVC+TFC Average Fixed Cost (AFC)-AFC is obtained by dividing the Total Fixed Cost By the total number of units produced. 4. AFC=TFC/Q Average Variable Cost (AVC)-AVC is obtained by dividing the Total Variable Cost by the number of units produced. AVC=TVC/Q 5. Average Total Cost (ATC)-ATC is obtained by dividing the Total Cost by the number of units produced. ATC=TC/Q Marginal Cost (MC)-Marginal cost is the addition made to the total cost by 6. producing an additional unit of Output. MC = ∆TC/∆Q, MCn = TCn-TCn-1 7. Cost Schedule: Out Put 0 1 2 3 4 5 6 7 8 9 10

- 47. Diagrams: MARGINAL AND AVERAGE COSTS: Marginal cost curve is U-Shaped because: MC falls in the beginning because of increasing return to a factor(decreasing cost ) and then increases due to diminishing return to a factor(increasing costs). Relationship: 1. Between Total Cost and Marginal cost. MCn =TCn-TCn-1 When Total Cost increases at a diminishing rate Marginal Cost decreases. When Total Cost increases at an increasing rate Marginal Cost increases. 2. Between Total Variable Cost and Marginal Cost. MCn =TCn-TCn-1 When Total Variable Cost increases at a diminishing rate Marginal Cost decreases. When Total Variable Cost increases at an increasing rate Marginal Cost increases. 3. Between Average Variable Cost and Marginal Cost. When MC ‹ AVC, then AVC falls. When MC =AVC, then AC is Minimum. When MC› AVC, then AVC rises. MC curve always intersect AVC at its minimum point. 4. Between Average Total Cost and Marginal Cost.

- 48. When MC ‹AC, then AC falls. When MC =AC, then AC is Minimum. When MC ›AC, then AC rises. MC curve always intersect AC curve at its minimum point. REVENUE Revenue is the total money receipt of the firm from sale of its product.Three main concepts of revenue are total revenue, marginal revenue, and average revenue. Total Revenue refers to the total money receipt of the firm from the sale of its total output TR = Number of units sold (Q) x price per unit (p) TR = P X Q Average Revenue: AR is revenue per unit of output sold. MARGINAL REVENUE: It is the addition to total revenue when an extra unit of output is sold. MR = TRn – TR n - 1 Relationship between AR & MR i) If AR is constant MR is equal to AR ii) If MR is above AR, AR increases. iii) If MR is below AR, AR decreases. AR and MR in Perfectly competitive market: AR, MR Output AR = MR In this market price or AR is constant. So MR isequal to AR. Both are represented by the same horizontal line parallel to OX-axis. AR & MR in non-competitive markets 1) The average revenue curve and marginal revenue curve slope downward from left to right. 2) Since AR falls MR curve lies below the AR curve. 3) MR falls twice the rate of fall in MR. Relationship between TR & MR: 1) As long as MR is positive TR increases. 2) When MR increases TR increases at increasing rate.

- 49. 3) When MR decreases, but positive TR increases at decreasing rate. 4) When MR is zero TR is maximum. 5) When MR is negative TR diminishes. QUESTIONS: Very Short Answer Questions: 1. What is meant by Variable Cost? Ans- Expenditure incurred on the variable factors of production are known as Total Variable Cost 2. What is meant by Fixed Cost? Ans- Expenditure incurred on the fixed factors of production are known as Total fixed costs 3. Define marginal cost. Ans- Marginal cost is the addition made to the total cost by producing an additional unit of Output. 4. Define Average Variable Cost. Ans- AVC is obtained by dividing the Total Variable Cost by the number of units produced. 5. Express Total Variable Cost in terms of Total Fixed Cost and Total Cost. Ans- TVC=TC-TFC 6. Explain marginal cost in terms of total cost. Ans. MCn = TCn-TCn-1 7. Why is Average Total Cost greater than Average Variable Cost? Ans- ATC=AVC+AFC 8. Give two examples of variable cost. Ans- Expenditure on raw materials and expenditure on labor. 9. How does Average Fixed cost behave as out-put decreases? Ans-AFC decreases. 10. How is MC derived from TVC? Ans. MCn = TVCn-TVCn-1

- 50. Short Answer Questions (3/4 Marks) 1. Draw TFC, TVC and TC curves in a single diagram. 2. Distinguish between Fixed Costs and Variable Costs. Give two examples of each. 3. Why is the MC curve in the short-run U-shaped? 4. Explain the relationship between the Marginal Cost and Average Cost with the help of a cost schedule and diagram. Ans- When MC ‹AC, then AC falls. When MC =AC, then AC is Minimum. When MC ›AC, then AC rises. MC curve always intersect AC curve at its minimum point. 5. What changes will take place in Total Cost if Marginal Cost is rising? Show with the help of a diagram. 6. Complete the following table. Out Put 1 -- 3 -- TVC 10 -- 27 -- AVC MC -- -- 8 6 -- -- 10 13 7. Complete the following table. Out Put 1 -- 3 -- 5 AFC MC TC -- -- -- -- 10 82 20 8 -- -- -- 99 12 10 -- REVENUE: 8. Find AR and MR. (i) Output 1 2 3 4 5 6 7 TR 10 24 33 40 40 36 28 Ans. AR 10 12 11 10 8 6 4 MR 10 14 9 7 0 -4 -8

- 51. 9. (i) Ans. Find out TR and MR. Output 10 AR 6 TR 60 MR - 9 8 7 8 63 64 3 1 10. (i) Complete the following table: Output1 2 3 4 Price- 9 - - MR10 - - 4 TR- - 24 - Ans. Output 1 2 3 4 Price 10 9 8 7 MR 10 8 6 4 TR 10 18 24 28 Q11. (i) Output123 MR1080 Calculate TR and AR 4 -2 Ans.TR101818 16 AR1096 4 12.How do changes in MR affect TR? Ans. i)If MR increases, TR increases at increasing rate. ii)If MR is constant, TR increases at constant rate. ii)IF MR falls, TR increases at diminishing rate. 13.What is MR? How is it related to AR? Ans. MR refers to the change in TR due to sale of an additional unit. Relation – (i)If AR (Price) is constant, MR = AR (ii)If AR (Price) falls, MR < AR. (iii)If AR (Price) rises, MR > AR. HOTs: 1.At what point does the MC curve cut the AVC curve? Ans- Minimum point of AVC. 2.What happens to ATC when MC is less than ATC? Ans-ATC falls 3.When AC is rising What is the relation between AC and MC? Ans-MC is greater than AC.

- 52. 4.The Average Cost of producing 5 units of a good is Rs 6 /- and that of producing 6 units is Rs 5/- What is the MC of producing 6 units? Ans-MC of producing 6 units is 0. Study Material For Under Achievers: 1. Define cost. Ans- Cost means the total expenditure incurred in the Production of a commodity 2. What is Marginal cost? Ans- 1.Marginal cost is the addition made to the total cost by producing an additional unit of Output. 3. What do you mean by variable cost? Ans-Expenditure incurred on the variable factors of production are known as Total Variable Cost 4. Write the formulas for calculating AFC, AVC and MC. Ans-AFC=TFC/Q AVC=TVC/Q MCn=TCn-TCn-1 5. State the relationship between AC and MC. Ans- When MC ‹AC, then AC falls. When MC =AC, then AC is Minimum. When MC ›AC, then AC rises. MC curve always intersect AC curve at its minimum point. 6. What is the relationship between TC and TVC? Ans-TC=TVC+TFC 7. Calculate TVC,AVC,AFC,AC and MC from the following data. TFC 60 60 60 60 60 60 60 60 TC 90 105 115 120 135 160 200 260 Ans-TVC=TC-TFC AVC=TVC/Q, AFC=TFC/Q, AC=TC/Q, MCn=TCn-TCn-1

- 53. Study Material for Bright Students: 1. What is MR? How is it related to AR? Ans. MR refers to the change in TR due to sale of an additional unit. Relation : (i) (ii) (iii) If AR (Price) is constant, MR = AR If AR (Price) falls, MR < AR. If AR (Price) rises, MR > AR. 2. What happens to ATC when MC is less than ATC? Ans-ATC falls 3.When AC is rising What is the relation between AC and MC? Ans-MC is greater than AC. 4. Explain the relationship between the Marginal Cost and Average Cost with the help of a cost schedule and diagram. Ans- When MC ‹AC ,then AC falls. When MC =AC ,then AC is Minimum. When MC ›AC ,then AC rises. MC curve always intersect AC curve at its minimum point. TEST PAPER -1 1. Fill in the blanks: 1x5=5 a. _cost increases and decreases with the volume of out-put. b. ------------------ cannot be changed in the short period. c. Wages is cost of the production. d. ATC= +AVC. e. =AFC x Q 2. Choose the correct answer. 1x5=5 a. Expenditure incurred on the fixed factors of production is known as- i)Total Cost. ii)Total fixed cost. iii)Total Variable Cost. iv)Marginal Cost. b. Average Variable Cost is obtained using which of the following formulas? i) TC/Q ii)TVC/Q iii)TFC/Q iv) AFC/Q

- 54. c.When Total Cost rises at a diminishing rate the Marginal Cost _. i)Rises. ii) declines iii)Constant. iv) increases d. Marginal Cost is calculated from . i)AVC ii)TC iii)TFC iv)AFC e. Cost of raw materials is an example of . i)fixed cost ii)variable cost iii)opportunity cost iv)marginal cost 3.Say whether true or false. a) MC is calculated from TVC. b) When MC is greater than AC, then AC falls. c) Average cost is always positive. 1x10=10 d) Average cost is always equal to the price of the commodity. e) Total cost is equal to the total fixed cost less total variable cost. f) AFC is equal to TFC divided by total out-put. g) Average cost is equal to AFC plus AVC. h) MC=TCn+1-TCn-1 i) TFC=AFC/Q J) TC=AFC+AVC. C. THEORY OF SUPPLY: 1. Supply: It is that quantity of a commodity which a seller or producer is ready to sell in the market at a certain price within a given time period. Factors Affecting Supply of the commodity: 1) Own price of commodity 2) State of technology 3) Prices of factors of production 4) Taxation policy 5) Price of related goods 6) Other factors like natural calamities.

- 55. Law of Supply: Other things being constant, there is a direct relation between price of a commodity and its quantity supplied i.e. higher the price more the supply and vice-versa. Supply Schedule: It is a schedule / table showing different quantities supplied of a commodity by a seller at different prices. Price Quantity Supplied 5 20 4 15 3 12 2 10 Supply Curve -If supply schedule is shown on a graph, we get a curve which is called supply curve. Market Supply: It is the horizontal summation of the supply of a product by all the producers in the market at a given price and at a point of time. Tabular presentation: Price per Unit (in Quantity Rs) supplied (Units) Quantity by A supplied (Units) Market by B (Units) Supply 5 4 6 10 4 3 5 8 3 2 4 6 2 1 3 4

- 56. Diagrammatic Presentation: Change in Quantity Supplied: When there is change in supply of a commodity due to change in price (This is movement along the supply curve) This Change is of two types. 1) Expansion in supply -Supply increases due to increase in price (Figure 3.10) 2) Contraction in supply -Supply decreases due to decrease in price. Change in Supply -(Shift in supply curve) When supply of a commodity changes due to factors other than price, like technique, taxation policy, prices of factors of production etc. This is called change in supply. This change is of two types: a) Increase in supply -when supply of a commodity rises due to factor other than price it is increase in supply. In this case the supply curve shifts rightward. b) Decrease in supply -when supply of a commodity falls due to factors other than price it is decrease in supply. In this case the entire supply curve shifts to the left (upward).

- 57. (Figure 3.11) Price Elasticity of Supply: It is the measurement of degree of change in supply of a commodity to change in its price. Es = % change in quantity supplied / % change in price Es = ∋Σ x P ∋Π S Factors Affecting Elasticity of Supply: 1. Nature of commodity Durable goods -Elastic Non-durable -Inelastic 2. Change in cost of production - 3. Technique of production 4. Time period. Methods of Measuring Elasticity: 1. Percentage method or Proportionate method. Es = % Change in QS or % change in price 2. Geometric method a) Es > 1 Proportionate change in Supply = ∋S x P Proportionate change in PriceS x ∋Π (Figure 3.12) b) Es = 1 Supply curve passes through origin.

- 58. c) Es < 1 (Figure 3.13) VERY SHORT ANSWER QUESTIONS: 1. What causes a downward movement along a supply curve of a commodity? Ans : Increase in cost of production 2. What causes an upward movement along the supply curve of a commodity? Ans: Decrease in excise duties. 3. What causes a movement along the supply curve of a commodity? An : change in price of goods. 3. State the law of supply. Ans : The law states that as price of a good rises, quantity rises, while other things remain constant. 5. Define supply. 6. When is the supply of a commodity called ‘elastic’?

- 59. 7. Price elasticity of supply of a good is 0.8. Is the supply ‘elastic’ or ‘inelastic’ and why? 8. Price elasticity of supply is 1.2. Is its supply elastic or inelastic and why? 9. Define market supply. 10. What is the price elasticity of a straight line supply curve touching the OY-axis? 11. What is the price elasticity of straight line supply curve touching the OX-axis? SHORT ANSWER QUESTION: 1. At a price of Rs. 8 per unit, the quantity supplied of a commodity is 200 units. Its price elasticity of supply is 1.5. If its price rises to Rs. 10 per unit, calculate its quantity supplied at new price 3. 2. The price elasticity of supply of a commodity is 2.5. At a price of Rs. 5 per unit, its quantity supplied is 300 units. Calculate its quantity supplied at a price of Rs. 4 unit. 3. The price of a commodity is Rs. 12 per unit and its quantity supplied is 500 units. When its price rises to Rs 15 per unit, its quantity supplied rises to 650 units. Calculate its price elasticity of supply. Is supply elastic? 4. List any three determiners of supply of a commodity. 5. Give three reasons for a rightward shift of supply curve of a commodity? 6. Give three reasons for ‘increase ‘in supply of a commodity? 7. State any three causes of leftwards shift of supply curve? 8. Explain the effect of ‘technological changes ‘on the supply of a product? 9. Define market supply of good. Give three causes of a rightward shift of supply curve? 10. What is meant by ‘change in supply’? State three factors that can cause’ ‘change in supply’? 11. When the price of a commodity falls from Rs. 10 per unit to Rs. 9 per unit, its quantity supplied falls by 20 percent. Calculate its price elasticity of supply? 12. The price of a commodity is rs.5 per unit and its quantity supplied is 600 units. If its price rises to Rs. 6 per unit, its quantity supplied rises by 25 per cent. Calculate its price elasticity of supply. 13. Due to a 10 per cent rise in the price of a commodity, its quantity supplied rises from 400 units to 450 units. Calculate its price elasticity of supply. Is its supply elastic? 14. A 5 per cent fall in the price of a commodity results in a fall in its quantity supplied from 400 units to 370 units. Calculate its price elasticity of supply. Is its supply elastic? 15. The price elasticity of supply of a commodity is 2. When its price falls from Rs. 10 to Rs. 8 per unit, its quality supplied falls by 500 units. Calculate the quantity supplied at the reduced price.

- 60. 16. When the price of a commodity rises from Rs. 10 to Rs. 11 per unit, its quantity supplied rises by 100 units. Its price elasticity of supply in 2. Calculate its quantity supplied at the increased price. 17.The elasticity of supply of a commodity is 3. An increase in its price from Rs. 20 to Rs. 21 per unitresults in a rise in its quantity supplied by 150 units. Calculate its quantity supplied at the increased price. LONG ANSWER QUESTION INCLUDING HOTS 1. Define price elasticity of supply. How is it measured by geometric method? (In case of a straight line supply curve). 2. Distinguish between ‘change in supply’ and ‘change in quantity supplied’ of a commodity. 3. Explain briefly the following determinants of supply: i. ii. iii. Increase in the prices of inputs. Decrease in tax on total product. Technological change. MCQ of Supply and Producer’s Equilibrium: Fill in the blanks: 1. A supply curve reflect the positive relationship between and quantity supplied. 2. An increase in the inputs prices shift the supply curve too the _. 3. Elasticity of supply = % change in quantity supplied ? 4. MR=MC and other condition is 5. Breakeven point is the point where is equal to TC. 6. A/An in supply will rise the supply curve, at the same price, . (Increase, Decrease, Constant) 7. Market supply is of individual supply. (Addition, Subtraction, Division) 8. Unitary elastic supply equal to . (2,>1, <1, 1) 9. If MC is more than MR at particular level of output, then Producer will the production to maximize the profits.

- 61. (Increase, reduce, constant) 10. Profit refers to . (Cost=Revenue, Cost>revenue, Revenue>cost) Find True and False and Give reasons: 1. Contraction of supply occurs due to change in factors other than price of the given commodity. 2. Supply is always Unitary elastic for all supply curves starting from the origin. 3. In case of zero elastic supply, supply curve is a horizontal straight line. 4. Law of supply does not indicate the magnitude of change in quantity supplied of a commodity due to change in its price. 5. At the state of Producer’s Equilibrium, marginal cost of the firm should rising. 6. To maximize the profits of a firm, the only condition needed is equality between marginal cost and marginal revenue. VALUE BASED QUESTIONS: Production Function: Returns to a Factor: 1. A producer produced 35 units by employing 4 laborers, but it produces 42 units by employing 5 laborers. What is the amount as marginal production? (1) Ans. MP = 42 - 35 = 7 units. 2. In Indian agriculture, we obtain 120 Million tons of food grains by employing 20mns of laborers if it employs 1 more millions of labor, production rises by 6 million tons which type of return it is?(1) Ans. Constant returns. 3. A firm employs form laborers and it had following value-additions. Comment on it. (2) Units of labor 1 2 3 4 Total product 4 10 18 28 Ans. We can calculate marginal product from it, to decide about the law of return applying upon this firm, shown through following table: Labor Total product Marginal products 1 4 4 2 10 6 3 18 8 4 28 10

- 62. Labor (millions) 1 2 3 4 Total production 25 54 55 5 (million tons) Since marginal product is increasing with additional laborer, therefore law of increasing returns is applicable on firm’s productions. 4. A country’s electronic industry is passing through diminishing returns to scale. It wants to raise product defeating the effect of diminishing stage. Suggest two ways. (2) Ans. In diminishing return to scale, firm’s cost of production rises which can lower firm’s profits. It can improve its profit ability through following measure: (i)By introducing new technology that helps in reducing its cost of production. (ii)By improving managerial skills so that labor cost as well as marketing costs are reduced. 5. Determine various stages of law of variable of proportions for a firm which has following total productivity table:(3) Labor 1 2 3 4 5 6 Total product 20 55 75 90 90 80 Ans. various stages of law of variable of proportion are determined on the basis of marginal product. Therefore, we rewrite the table in following manner: LaborTotal product 120 255 375 490 590 680 Ist Stage: till MP is highest at second laborer. IInd stage: Till MP was zero at 5th laborer. IIIrd stage: when MP becomes negative at 6th laborer. Marginal product 20 35 (Ist stage) 20 15 0 (2nd stage) -10 3rd stage 6. Production function of a firm is given as Y= 5L+2K A firm employs zero units of labor and to units of capital, what would be its total output? Ans. Y= 5L+2K(where L=0 & K=10) Y =5(0) + 2(10) =20units 7. Total production in an economy is given as such: Fixed factor10mn hectares of land (1) (2) Determine the stage of law of returns to a factor. Ans. Law of returns to a factor can be determined on the basis of marginal production which is given as such.

- 63. Fixed factors Labor Total product Marginal product (Millions) (Million tons) (million tons) 10 million hectares 10 25 --- of land 20 35 10 30 45 10 40 55 10 Law of diminishing constant returns to a factor is being applied. Supply and Elasticity of Supply: 8. A firm raises its supply without any incentive of rise in price, mention three reasons. Ans. (i)Improvement in technique in production. (ii)Fall in factor pricing. (iii)Subsidies provided by the state. (3) 9. An electronic company has enough period to raise the supply of A.C’s. what type of elasticity of supply it will have (1) Ans. Elastic 10. Demand for a good is elastic whereas its supply is inelastic. What impact it will have, when demand for good increases? Explain. Ans. When supply is inelastic, it means supply for such a product cannot be increased. Now when demand for it increases, it will raise price for such a good. 11. “Supply of agricultural goods is inelastic”. Explain. Ans. Yes, it is true that supply of agricultural goods is inelastic because it is not inspired by price-rise rather it depends upon natural, climatic and biological factors. Such goods take lot of time in its production, therefore no price-frame can guide there production. 12. Imports of production with less elastic supply can fetch higher revenue. Explain. Ans. True, those imported goods which are inelastic or less elastic like petrol and diesel and can fetch higher revenue. It is because of the reason that such goods will be sold at high price because of limited supply. Therefore, the yield from such import will be higher. 13. Which of the following is an example of increase in supply? Explain with reason. X- commodity Y- commodity Price Rs.Supply Price Rs .Supply 10100 50 1000 1212 50 1200 (1) (2) (2) (2)

- 64. Output (unit 0 1 2 3 4 5 6 Total cost 60 160 240 300 400 560 780 Ans. Supply of Y-commodity is an example of increase in supply because in this case supply increases even when price per unit remains to be Rs. 50. In case of X- commodity, there is extension in supply because here supply rises with every increase in price. In case of Y-Commodity, supply increases due to factors other than price rise. Concepts of Costs: 14. Rent paid for hiring a building and depreciation of machine is a fixed on variable cost?(1) Ans. Fixed costs 15. When cost of producing one commodity is expressed in terms of alternative commodity, it is known as which costs?(1) Ans. Opportunity Cost 16. Total cost for 6 units of a good is given through the following table. Determine total variable cost and marginal cost from it. (3) Ans. Rs. 60 is total fixed cost as it is cost of producing zero units. Here TVC=TC- TFC and MC=TVCn-TVCn-1. It is calculated as follows: Output (units) T.C.(Rs) TFC (Rs.) TVC (Rs.) M.C. (Rs.) 0 60 60 0 --- 1 160 60 100 100 2 240 60 180 80 3 300 60 240 60 4 400 60 340 100 5 560 60 500 160 6 780 60 720 220 17. Supply curve of a firm is represented through which type of costs? (2) Ans. Supply curve of a firm is represented through an average cost curve (AC) and Marginal cost cure (MC). Concepts of Revenue: 18. Total revenue earned from 20 units was Rs.800, what was average revenue? What is its alternative name?(1) Ans. AR=TR/Q = 800/20 =Rs.40. It is also known as price. 19. In case of perfect competition, what shape of AR curve? (1) Ans. It is parallel to x-axis.