Downloaded 49 times

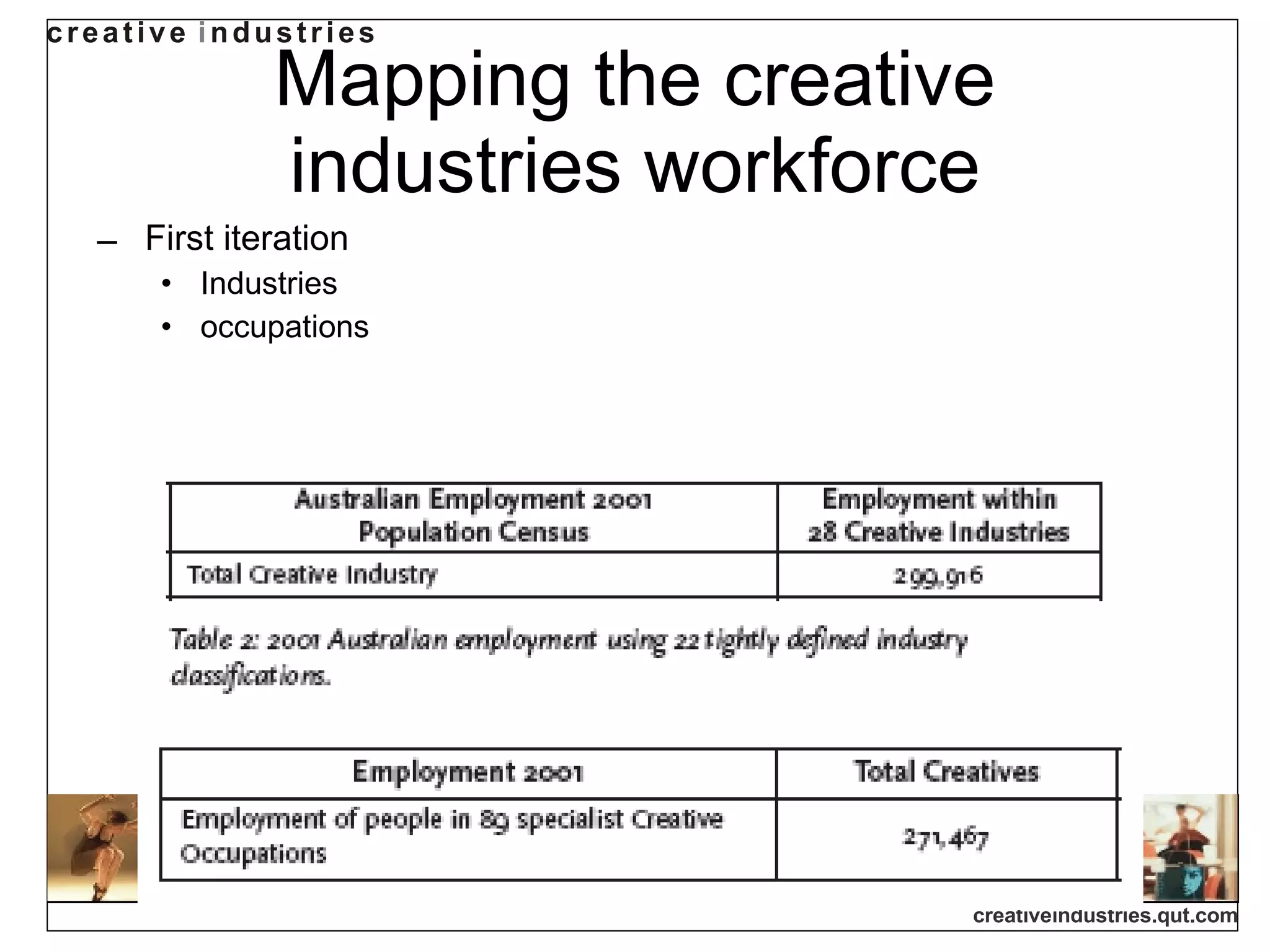

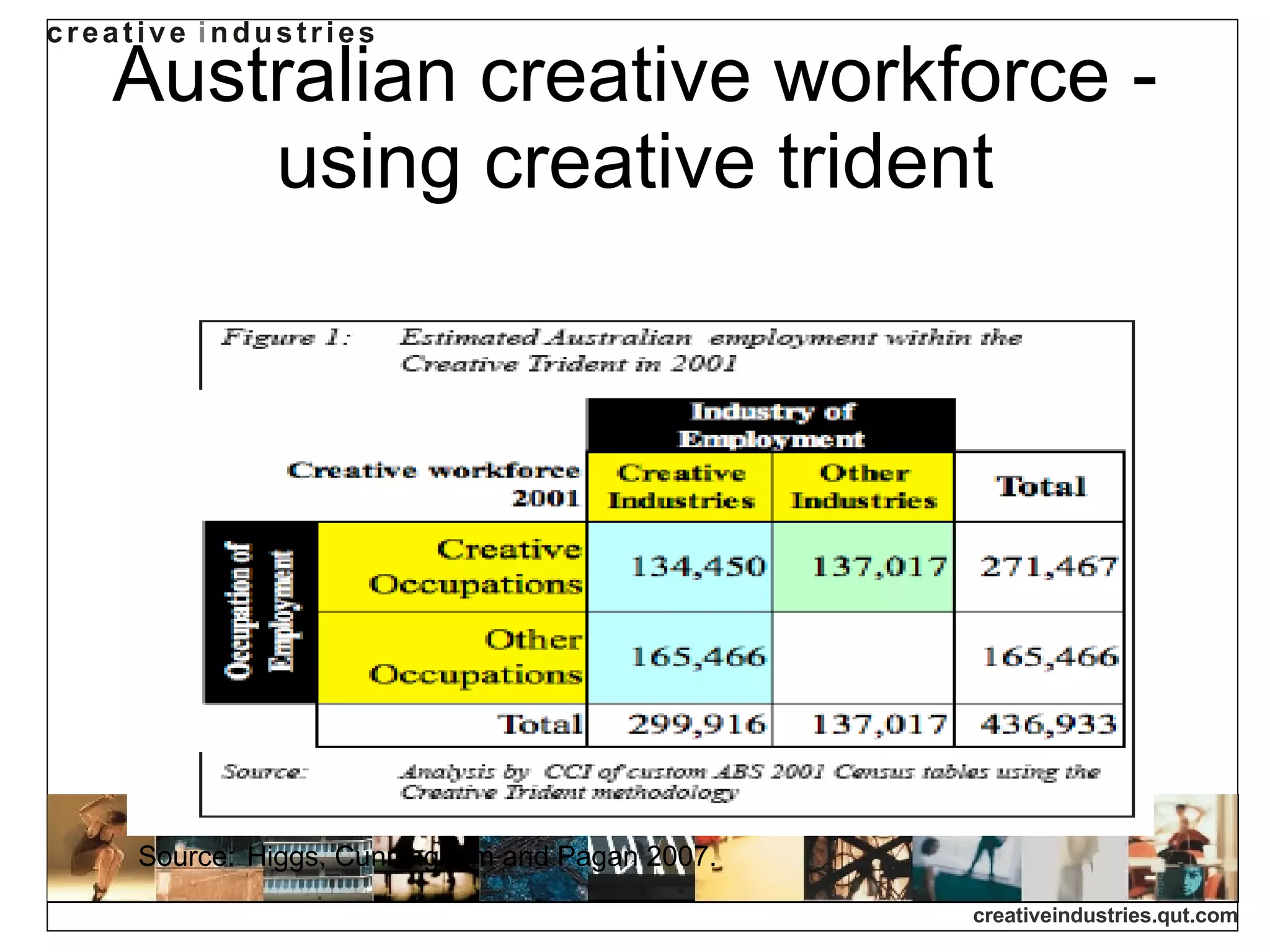

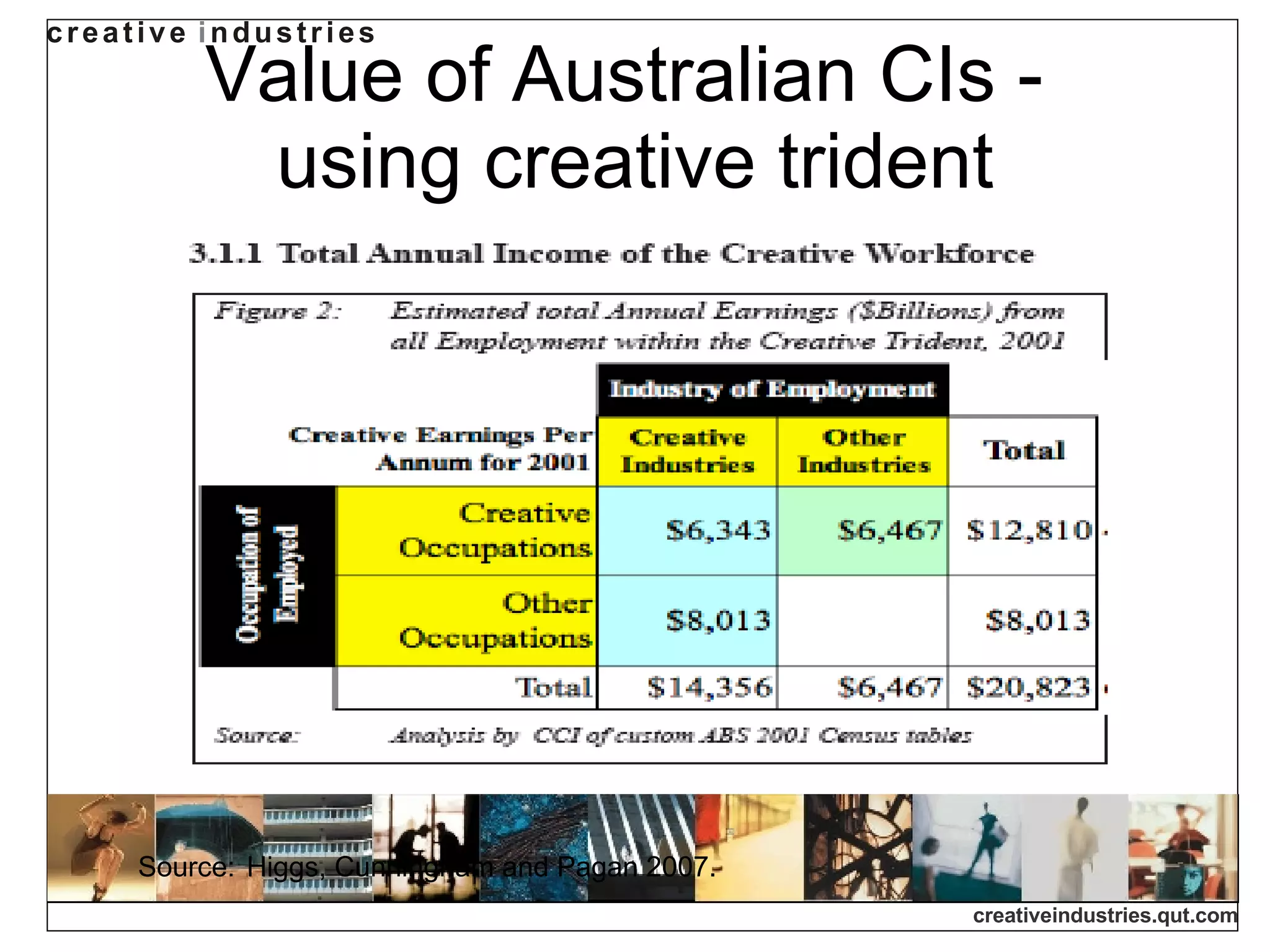

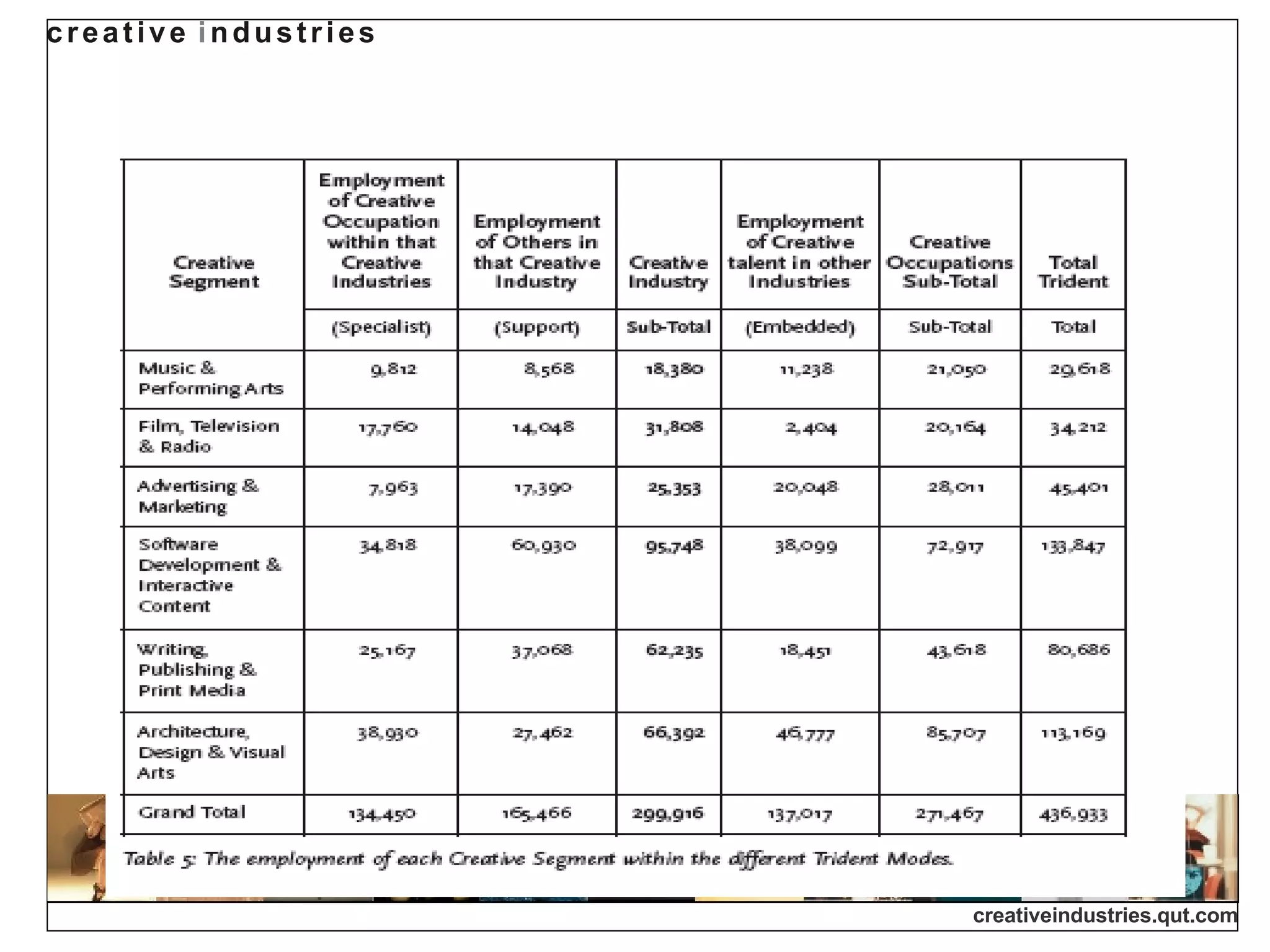

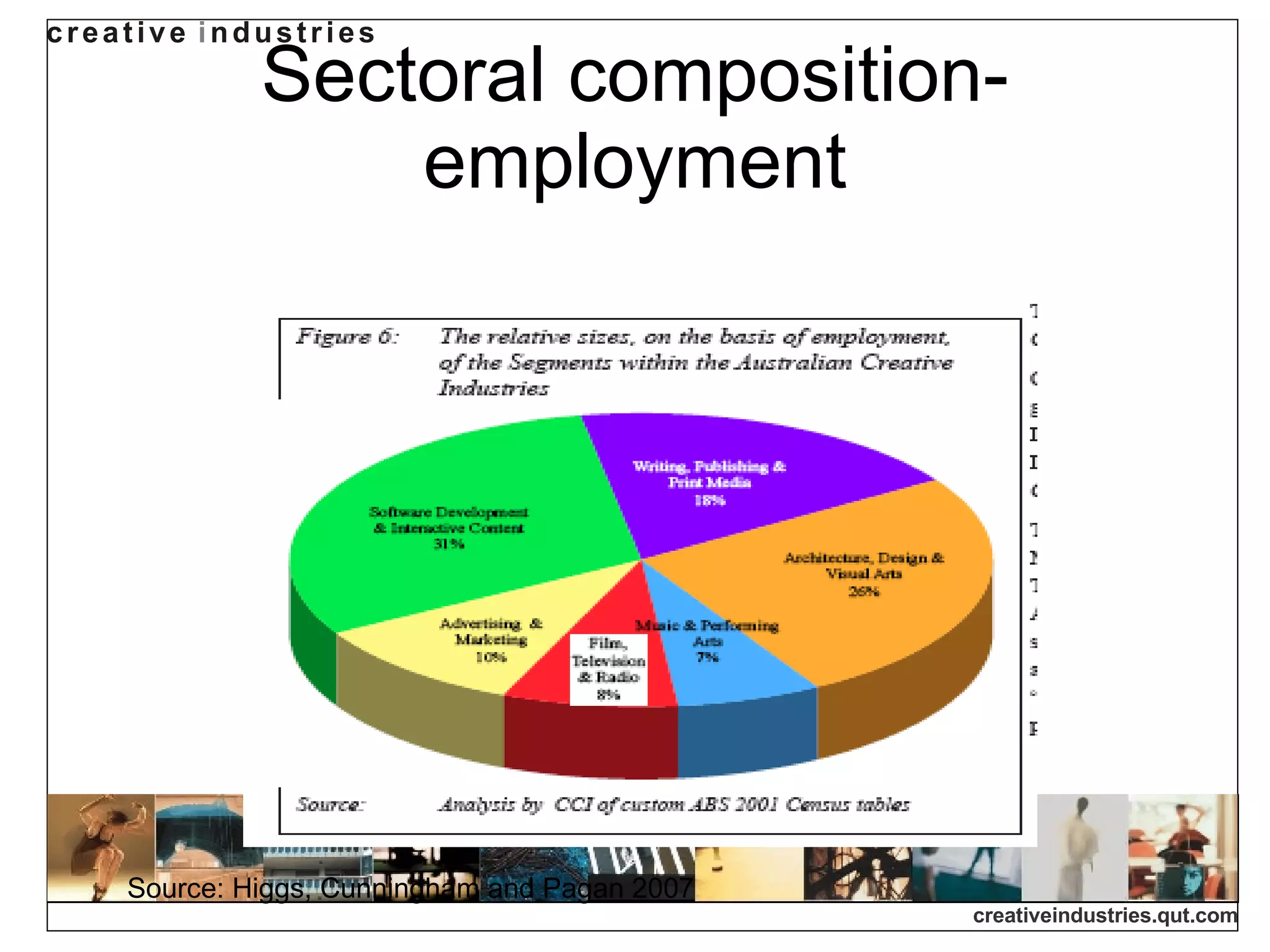

This document provides an overview of the creative industries in Australia and other countries over the past decade based on a guest lecture by Professor Terry Flew. It discusses definitions of the creative industries, economic contributions, workforce analysis, growth trends, and implications for policy and education. Key findings include that the creative industries accounted for 5.4% of the Australian workforce in 2001 and experienced 3% annual growth between 1996-2006. The sector is more significant than previously acknowledged but remains difficult to define and measure precisely.

![[BROCHURE] Italy Tour Project | @SlideON](https://cdn.slidesharecdn.com/ss_thumbnails/brochure8-251215152319-2805af68-thumbnail.jpg?width=640&height=640&fit=bounds)