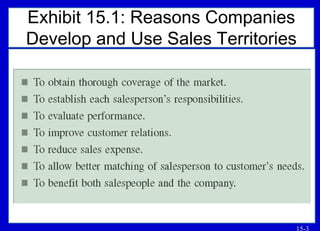

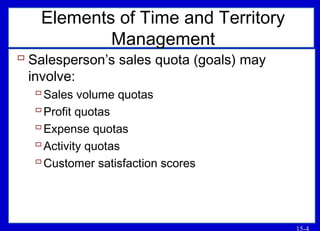

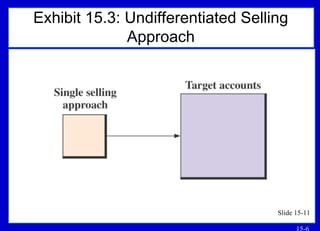

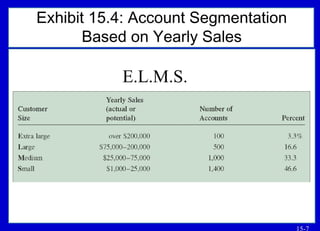

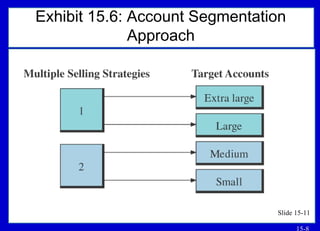

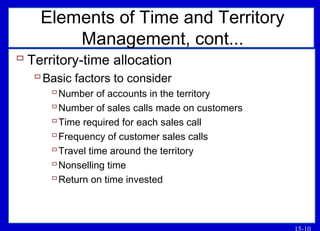

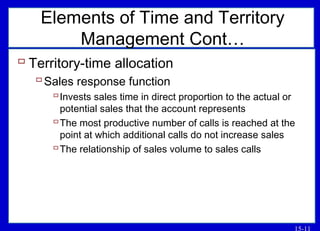

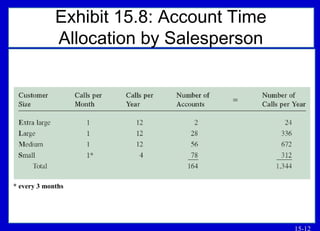

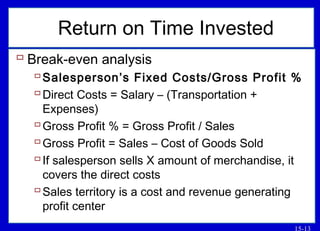

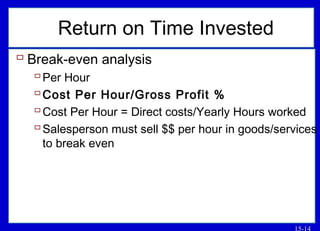

This document discusses keys to successful sales territory management including defining territories, setting sales quotas, analyzing accounts, allocating time to territories, and calculating return on time invested. Territories group customers or geographical areas and are assigned to salespeople. Quotas may involve sales volume, profit, expenses, activities, and customer satisfaction. Account analysis includes differentiation by annual sales, priority levels, or multiple variables. Time allocation considers accounts, calls, travel, and non-selling activities. Return on time is calculated using break-even analysis of fixed costs, gross profit percentage, and sales required to cover costs.